April 11, 2026

April 5, 2026

Home › Financial Stability › Income Volatility Management › Irregular Income Survival Guide: How to Stay Stable When Pay Fluctuates

This article is part of the Income Volatility Management cluster on PersonalOne — how to build financial stability when your income changes month to month.

Here's Your Irregular Income Survival Guide

Don Briscoe is a Financial Systems Strategist with 12+ years of experience helping Millennials and Gen Z build financial stability and income systems. He founded PersonalOne to provide the financial education he wished existed — structured, honest, and free.

What You Need to Know

— Stability on irregular income is a systems problem, not a discipline problem — standard budgeting breaks when income changes month to month

— Budget to your income floor (your lowest month), not your average — every fixed expense must fit within that number

— An income buffer account absorbs timing volatility before it reaches your bills — this is the most important structural piece

— A pre-defined high-month protocol and low-month playbook eliminate reactive decision-making under financial stress

— Tax reserves for self-employment income must be separated from operating money at the point of deposit, not at filing

Every irregular income survival guide starts in the same place: the month everything fell apart. Income came in late, a bill hit early, and what looked like a reasonable financial situation became a crisis inside of ten days. If you have freelance, commission, gig, or seasonal income, you already know this cycle.

The fix is not earning more, budgeting harder, or having better willpower. Those approaches assume the problem is behavioral. It is not. The problem is structural. Standard financial advice was designed for people who receive the same deposit every two weeks. That architecture breaks entirely when your income swings from $2,000 to $9,000 to $4,500 with no predictable pattern.

This guide builds you a system that handles volatility at the structural level — before it creates stress, before it disrupts your bills, and before it forces decisions that cost you more in the long run. The income volatility management framework here is built specifically for variable earners who need stability without a predictable paycheck.

What Counts as Irregular Income

Irregular income means your pay amount changes significantly month to month, week to week, or project to project. This includes freelancers and contractors whose income is project-based, where one month might bring $11,000 and the next $1,200. It includes commission-based workers in real estate, sales, or financial services whose income is tied directly to what closes. It includes gig and platform workers whose hours-based income fluctuates with demand and personal availability. Seasonal workers in retail, landscaping, or tourism face income peaks and valleys that follow a calendar rather than a paycheck schedule. Business owners see revenue shift with sales cycles and client retention. Tipped workers — servers, bartenders, delivery drivers — face income that varies by shift, day, and economic conditions entirely outside their control.

The core problem in every case is the same: your expenses arrive on a fixed schedule. Your income does not. That timing mismatch — not a lack of income — is what creates constant financial instability even when total annual earnings are adequate.

Why Standard Budgeting Fails Variable Earners

Standard budgeting operates on a fundamental assumption: income is consistent enough to assign fixed percentages to spending categories. Spend 30% on housing. Save 20%. Allocate 15% to food. These percentages only work if the denominator — your income — stays relatively constant. When it swings 60% between months, percentage budgets collapse.

Three specific failure points appear in nearly every variable earner's financial breakdown. The first is lifestyle inflation in high months — a big income month feels like permission to spend, and new expenses become fixed costs that persist into lower-income periods. The second is panic spending in low months — without a system, credit cards absorb the gap reactively and the financial drag takes months to recover from. The third is the absence of any buffer between income and bills — when income flows directly into the same account that pays fixed expenses, every timing mismatch becomes an immediate crisis. The goal is a financial stability system that decouples income arrival from bill payment entirely.

The Income Floor Method: Budget to Your Worst Month

The foundational rule of variable income budgeting: never budget to your average income. Budget to your floor.

Pull the last 6 to 12 months of income history. Identify your single lowest month. That number — not the average, not the median, not the good months — becomes your budget baseline. Every fixed expense in your life must fit within your income floor. If it does not fit, you have an expense reduction problem to solve before anything else.

This approach feels restrictive when you know your average is higher. But the floor method solves the most dangerous pattern in variable income: spending in anticipation of income that has not arrived yet. When your expense structure fits inside your worst month, no single bad income period derails your financial system. Everything above the floor becomes allocation territory for buffer building, savings, and future investment.

Build the Income Buffer Before Anything Else

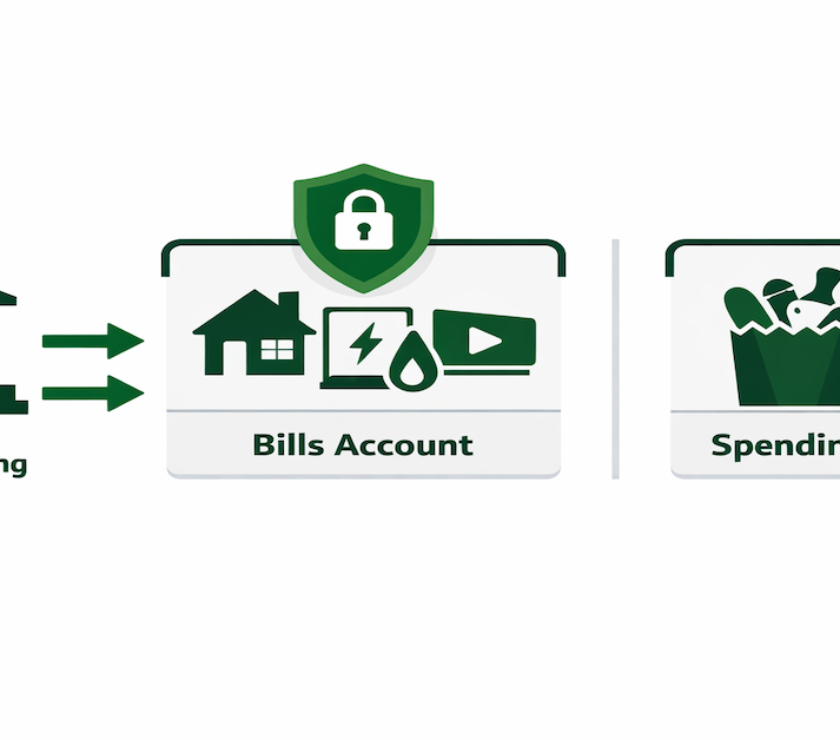

An income buffer is not an emergency fund. These serve different purposes. An emergency fund covers unexpected catastrophic expenses — job loss, medical crisis, major car repair. An income buffer absorbs paycheck timing volatility. It is the structural gap between when income arrives and when bills are due.

The target size for a functional income buffer is 4 to 8 weeks of your fixed expense total. For a variable earner with $2,800 per month in fixed expenses, that means $2,800 to $5,600 sitting in a dedicated buffer account — separate from operating money, separate from savings.

The buffer account changes how income flows through your financial system. Income arrives, enters the buffer, and bills pull from the buffer on their regular schedule. When a low-income month hits, the buffer absorbs the gap. When a high-income month arrives, the buffer refills and excess moves to savings. The buffer is what makes the system function for variable earners — without it, every income swing becomes a direct threat to fixed expenses. Pairing this with a solid account structure for variable earners gives the buffer a proper home in your overall banking architecture.

The High-Month Protocol: What to Do When Income Spikes

High income months are where most variable earners lose financial ground without realizing it. The income feels large, the bills are paid, and what remains looks like discretionary money. A structured high-month protocol eliminates the decision fatigue of figuring out what to do with a large deposit each time it arrives.

When income exceeds your floor, run it through this allocation order. First, refill the buffer to its target level if it was drawn down in a prior low month. Second, confirm all fixed expenses for the current period are funded. Third, move tax reserves to a dedicated holding account — 25 to 30 percent of net self-employment income for most freelancers and contractors. Fourth, allocate to savings targets: emergency fund, sinking funds, or investment contributions determined in advance. Fifth, and only after all of the above, discretionary spending from what remains.

The protocol works because it treats high-income months as system-building opportunities rather than spending events. When the next slow month arrives, the buffer is full, taxes are reserved, and savings are intact.

The Low-Month Playbook: Surviving Shortfalls Without Debt

Low income months are inevitable for variable earners. The system succeeds or fails based on whether you have a predetermined response rather than a reactive one. Three tiers apply as shortfall severity increases.

Tier 1 — Income is 80 to 100% of floor. The buffer absorbs the gap. No behavioral changes required. Fixed expenses are covered. This is exactly why the buffer exists.

Tier 2 — Income is 50 to 79% of floor. The buffer absorbs what it can. Discretionary spending suspends immediately. Subscriptions and non-essential recurring charges pause. Variable expenses compress across groceries, dining, and entertainment. No new discretionary spending this month. No debt.

Tier 3 — Income is below 50% of floor. Full survival mode. The buffer covers fixed expenses. Every non-essential expense eliminates. The emergency fund becomes eligible to supplement only after the buffer is exhausted. Simultaneously, income recovery becomes the active priority — additional hours, faster invoicing, pipeline acceleration. This is a temporary crisis response, not a budget strategy.

Pre-defining your tier responses removes the most damaging element of a low-income month: emotional decision-making under financial stress. The decision is already made. You execute.

Tax Planning for Variable Income Earners

Variable income — particularly freelance and self-employment income — creates a tax obligation that salaried workers never encounter in the same way. No employer withholds payroll taxes. Quarterly estimated tax payments are the responsibility of the earner. Missing them results in underpayment penalties at filing.

The safest approach is a dedicated tax reserve account that receives a fixed percentage of every income deposit before any other allocation. A general guideline for self-employed earners is 25 to 30 percent of gross self-employment income. This account does not get spent. It sits until quarterly estimated payments are due. Variable earners who spend their full deposit and pay taxes from savings at filing time face a predictable crisis every March and April. The budgeting strategies for growth framework connects the tax reserve system to a broader structure for directing surplus income efficiently.

Ready to build the full system?

This guide covers the core framework. For the complete income volatility management system — including account architecture, routing protocols, and integration with your full financial structure — return to the cluster hub.

Income Volatility Management →Building Income Stability Over Time

The survival guide framework is foundational, but sustainable stability for variable earners requires two additional layers built over time: income diversification and floor elevation.

Income diversification means adding a second income stream that operates on a different cycle than the primary one. A seasonal worker picks up a skill-based freelance service that generates off-season income. A commission-based salesperson builds a small recurring revenue product. The goal is reducing the depth and duration of low-income periods by ensuring not all income sources trough simultaneously.

Floor elevation means systematically raising your minimum reliable income over time — through rate increases, retained clients, and added income sources. A floor of $2,500 per month creates a tight system. A floor of $4,500 per month creates room for faster savings, larger buffers, and investment contributions. The account structure does not change as the floor rises — the amounts simply grow.

Resources

Official Sources

CFPB: Budgeting and Money Management Resources — Consumer Financial Protection Bureau guidance on budgeting, cash flow, and financial planning tools.

IRS: Self-Employed Individuals Tax Center — Official IRS guidance on estimated taxes, quarterly payments, and self-employment tax obligations.

BLS: Employed Persons by Class of Worker — Bureau of Labor Statistics data on employment types including self-employed and gig workers.

SBA: Managing Business Finances — Small Business Administration guidance on cash flow management for self-employed individuals and small business owners.

Continue Building Your Stability System

This article is one part of the complete income volatility framework. The full system — including buffer architecture, account structure, and allocation protocols — lives in the Income Volatility Management cluster hub inside the Financial Stability authority hub.

Frequently Asked Questions

How large should my income buffer be to start?

Start with a target of four weeks of fixed expenses. This covers most timing mismatches between income and bills without requiring a large upfront accumulation. Work toward six to eight weeks over the following few months as income allows. Four weeks is functional; eight weeks is resilient.

What if my income floor does not cover my fixed expenses?

This is a structural problem, not a budgeting problem. When the floor does not cover fixed costs, you either need to reduce fixed expenses or actively raise the floor through rate increases, additional clients, or secondary income. Budgeting tools cannot solve a math problem where minimum income is less than minimum expenses. Fix the structure first.

Can I use a high-yield savings account for the income buffer?

Yes, and it is recommended. The income buffer should be in a high-yield savings account separate from your main checking. This keeps the buffer visible, earns interest while it sits, and adds one friction step between you and impulsive use of the funds. Ensure the account allows fast transfers back to checking when needed — most HYSAs settle within one business day.

How do I know what percentage to set aside for taxes?

For most self-employed earners, 25 to 30 percent of gross self-employment income is a safe estimate for combined federal and state self-employment tax liability. The actual number depends on your total income, filing status, deductions, and state. If your income creates significant quarterly liability, working with a tax professional to calculate accurate estimated payments is worth the cost.

Is this system different for gig workers versus freelancers?

The core structure is the same. The main variable is income floor stability. Gig workers with platform-based income often have a more predictable floor because hours can be controlled. Freelancers and project-based contractors have higher variance because income depends on client decisions outside their control — which is why freelancers typically need a larger buffer of six to eight weeks to absorb longer payment gaps.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, tax, or legal advice. Tax treatment of compensation components changes and varies by individual circumstances — consult a qualified tax professional for guidance specific to your situation. PersonalOne is not a licensed financial advisor.