May 22, 2025

Updated: January 26, 2026 | 10 min read

By Don Briscoe, a personal finance educator with over 12 years of experience guiding everyday people through smarter banking, credit, and money decisions.

TL;DR — 0% APR Credit Cards

- 0% APR cards pause interest for 12-21 months on purchases, balance transfers, or both — giving you breathing room to pay down debt.

- Best for balance transfers: Cards offering 18-21 months can save thousands in interest if you're carrying high-rate debt ($5,000 at 22% APR = $5,500 in interest over 5 years).

- Critical requirement: You need a real payoff plan before applying — a 0% card without strategy just delays the problem and adds temptation to spend more.

- Watch for balance transfer fees: Typically 3-5% of transferred amount, though some promotional offers waive this temporarily.

- After the promo period: Standard APRs kick in (usually 18-29%), so any remaining balance starts accruing interest immediately.

If you're carrying credit card debt at the typical 20-24% APR, you're watching hundreds or thousands of dollars vanish into interest charges every year instead of making actual progress on your balance. It's frustrating, demoralizing, and financially draining — especially when it feels like your payments barely move the needle.

0% APR credit cards offer a rare opportunity: they pause interest charges for an introductory period (typically 12-21 months), allowing every dollar of your payment to go directly toward reducing your principal balance. For someone with $5,000 in debt at 22% APR making $200 monthly payments, switching to a 0% card could save over $1,000 in interest and help you become debt-free 8-10 months faster.

But here's the reality check: 0% APR cards are a tool, not a solution. They create space for you to execute a debt payoff strategy, but they won't fix the underlying spending habits or lack of planning that created the debt in the first place. Used correctly, they're powerful accelerators. Used carelessly, they just delay consequences while adding new temptations to spend.

This guide breaks down how 0% APR cards actually work, which types of offers exist, how to evaluate whether you're a good candidate, and most importantly — how to use them strategically to eliminate debt rather than just shuffling it around while accumulating more.

What 0% APR Actually Means (And What It Doesn't)

APR stands for Annual Percentage Rate — the cost of borrowing money on your credit card expressed as a yearly percentage. When a card offers 0% APR, it means you won't be charged interest during the promotional period, typically ranging from 12 to 21 months depending on the card and your creditworthiness.

Three Types of 0% APR Offers

1. 0% APR on Balance Transfers

You can transfer existing credit card debt from other cards to this new card and pay no interest on the transferred amount during the promotional period. This is the most valuable type for people carrying debt.

Typical terms: 18-21 months at 0%, then 18-29% APR. Balance transfer fee of 3-5% (so transferring $5,000 costs $150-250 upfront). New purchases usually accrue interest at the standard rate unless the card offers 0% on purchases too.

2. 0% APR on Purchases

New purchases made with the card during the promotional period don't accrue interest. This works well for planned large purchases you want to pay off over time without interest.

Typical terms: 12-15 months at 0%, then 18-27% APR. No transfer of existing debt allowed, or if allowed, it's at the standard APR. Useful for financing planned expenses like appliances, electronics, or home repairs.

3. 0% APR on Both Transfers and Purchases

The best of both worlds — you can transfer existing debt and make new purchases without interest during the promo period. These cards typically offer slightly shorter promotional periods (15-18 months) as a trade-off for the flexibility.

Typical terms: 15-18 months at 0%, then 19-29% APR. Balance transfer fee still applies (3-5%). Requires excellent discipline since you're tempted to both transfer debt AND spend more.

What 0% APR Doesn't Mean

- It's not free money: You still owe the full principal balance. You're just not being charged interest for a limited time.

- It doesn't erase your debt: If you don't pay off the balance before the promo ends, you'll start accruing interest at potentially very high rates.

- It won't automatically improve your credit score: Opening a new card creates a hard inquiry (temporary score dip), and if you max it out with transfers, your utilization spikes. The score benefit comes from paying down the balance strategically.

- It's not a permanent solution: If you don't address the spending habits that created the debt, you'll end up right back where you started — or worse.

The Tool Needs a Plan

A 0% APR card only works if you pair it with a real plan for paying off credit cards, not more spending. Without a structured payoff strategy, you're just moving debt around while potentially adding to it — which defeats the entire purpose of the interest-free period.

The Math: How Much You Can Actually Save

Let's look at real numbers to see why 0% APR cards matter for people carrying balances:

Scenario: $5,000 credit card balance at 22% APR

Without a balance transfer:

Making $200/month payments: You'll pay $1,862 in total interest and take 32 months to pay off the balance. Your payments break down to roughly $92 going to interest and $108 to principal in the early months.

With a 0% APR balance transfer for 18 months:

Transfer fee: $250 (5% of $5,000)

Making $300/month payments: You'll pay off the entire balance in 18 months (including the transfer fee) with zero interest charges. Total cost: $250 transfer fee.

Total savings: $1,612 compared to keeping the debt on your original card.

Even if you can only afford $200/month payments, you'd pay off $3,600 during the 18-month promo period, leaving a $1,650 balance that would then accrue interest. But you'd still save over $1,000 in interest compared to never transferring.

The key insight: Every dollar you pay during the 0% period goes entirely to principal reduction, which is why these cards are so powerful for aggressive debt payoff. But only if you actually execute the plan.

Are You Actually a Good Candidate for a 0% APR Card?

Not everyone should apply for these cards. Here's an honest assessment of who benefits and who should probably look at other debt relief strategies:

You're a Good Candidate If:

- Your credit score is 670+: Most 0% APR cards require good to excellent credit for approval and the best promotional terms. Below 670, you might get approved but with shorter promotional periods or higher post-promo rates.

- You have a realistic payoff plan: You've calculated exactly how much you need to pay monthly to eliminate the balance before the promo ends, and you're confident you can maintain those payments.

- You've addressed the spending problem: You understand why the debt accumulated and have implemented changes (budget, spending limits, automatic payments) to prevent it from happening again.

- You're carrying $2,000+ in high-interest debt: Below $2,000, the transfer fee might outweigh the interest savings unless your current APR is extremely high. Above $2,000, the math usually works strongly in your favor.

- You won't use it as an excuse to spend more: You're planning to put the new card away after the transfer and focus solely on payoff, not treating the available credit as spending money.

You're NOT a Good Candidate If:

- Your credit score is below 640: You'll likely be denied or offered terms that aren't much better than your current situation. Focus on credit building first.

- You haven't fixed the underlying spending issue: If you're still spending more than you earn or have no budget, a 0% card will just add more available credit to abuse. You'll end up with the original debt PLUS new debt on the 0% card.

- You can't afford to pay off the balance in the promo period: If your maximum possible payment won't eliminate the debt before the 0% expires, you might be better off with debt consolidation, settlement, or working with your current creditors.

- You're considering bankruptcy: Don't take on new credit if bankruptcy is a serious possibility within the next 12 months. Consult a bankruptcy attorney first.

- You need debt forgiveness, not just time: If your debt is genuinely unmanageable ($20,000+ in credit card debt with income under $40,000), a 0% card just delays the inevitable. You might need debt settlement or credit counseling instead.

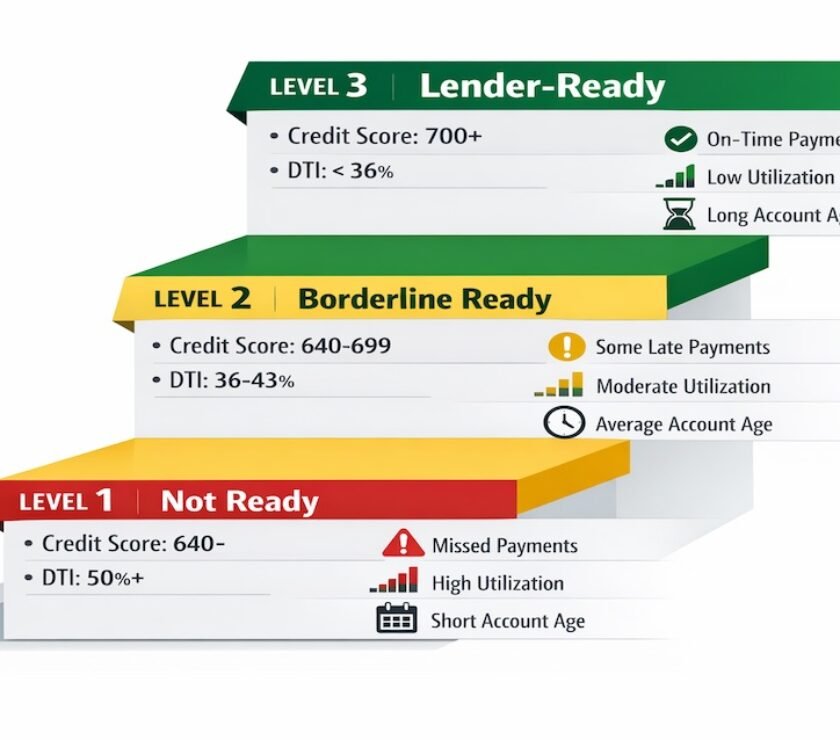

Check Your Readiness First

Before applying, check where you stand in the credit readiness framework so a balance transfer doesn't backfire. If you're not actually ready for new credit or lack the discipline to execute a payoff plan, this tool becomes a trap rather than a solution.

What to Look For in a 0% APR Card

Not all 0% APR offers are created equal. Here are the critical factors to evaluate:

1. Length of Promotional Period

Ideal: 18-21 months

The longer the better, as it gives you more time to pay down the balance. A 21-month promo period on a $6,000 balance requires $286/month to pay off completely. At 12 months, you'd need $500/month — a much tighter budget constraint.

Watch out: Some cards offer longer promotional periods only if you make on-time payments every single month. Miss one payment, and the promo can be revoked, retroactively charging interest from day one. Read the terms carefully.

2. Balance Transfer Fee

Standard: 3-5% of transferred amount

On a $5,000 transfer, that's $150-250 added to your balance immediately. Some promotional offers temporarily waive this fee, which can save you hundreds of dollars. These no-fee offers are rare but worth hunting for.

Break-even calculation: Even with a 5% transfer fee, you'll save money if your current APR is 15% or higher and you plan to carry the balance for at least 12 months. The higher your current APR, the faster you break even on the transfer fee.

3. Post-Promotional APR

Range: 16-29% variable

This is what you'll be charged on any remaining balance after the promo ends. While your goal should be to pay off everything during the 0% period, life happens. A lower post-promo APR (18-20%) provides a softer landing than a higher one (25-29%) if you can't eliminate the balance completely.

4. Transfer Window

Typical: 60-120 days from account opening

You must complete balance transfers within this window to qualify for the 0% rate. Transfers initiated after the window closes will be charged the standard APR. Don't wait — complete transfers immediately after approval.

5. Annual Fee

Best: $0 annual fee

Most balance transfer cards charge no annual fee, but some premium cards with longer promotional periods might charge $95-150 annually. Only consider cards with annual fees if the promotional period is significantly longer or the terms are substantially better than no-fee alternatives.

How to Use a 0% APR Card Strategically (Not Recklessly)

Getting approved for a 0% APR card is the easy part. Using it correctly to actually eliminate debt is where most people struggle. Here's your execution plan:

Step 1: Transfer Strategically

- Prioritize highest-interest debt first: Transfer balances from cards charging 22-29% APR before transferring anything at 15-18%.

- Don't max out the new card: Try to keep total utilization below 80% of the new card's limit to minimize credit score impact. If you have a $10,000 limit, transfer no more than $8,000.

- Complete all transfers within 7 days of approval: Don't wait. The sooner you transfer, the more of the promotional period you preserve for actual payoff.

- Keep old cards open: Don't close the cards you transferred from — this reduces your total available credit and spikes your utilization ratio, hurting your score.

Step 2: Calculate Your Required Monthly Payment

Take your total transferred balance (including transfer fee) and divide by the number of promotional months:

Example: $5,250 transferred balance ÷ 18 months = $292/month minimum to pay off completely

Your action: Set this as your minimum automatic payment. Anything extra you can pay accelerates your payoff and builds a safety buffer in case of unexpected expenses.

Step 3: Physically Hide or Freeze the Card

Don't carry the 0% APR card in your wallet. Put it in a drawer, freeze it in ice, or store it somewhere inconvenient. The available credit should not be treated as spending money. This card has one job: holding your transferred debt while you pay it off.

Exception: If the card offers 0% on both transfers and purchases, and you have a specific planned expense (replacing a broken appliance, necessary car repair), you can use it for that — but only if you've budgeted the payoff into your monthly payment calculation.

Step 4: Set Calendar Reminders

Create three critical reminders:

- 6 months before promo ends: Check your progress. Are you on track? Can you increase payments?

- 3 months before promo ends: Final push. Consider using tax refund, bonus, or side hustle income to pay down more aggressively.

- 1 month before promo ends: If you won't finish, decide whether to do another balance transfer, increase payments dramatically, or prepare for the interest rate jump.

Step 5: Never Miss a Payment

Some cards will revoke your 0% promotional rate if you're even one day late with a payment — and they can retroactively charge interest from the day you opened the account. Set up automatic payments for at least the required monthly amount, scheduled 2-3 days before the due date to account for processing time.

Understanding the Bigger Picture

Using a 0% APR card doesn't automatically improve your credit score — in fact, the initial application and high utilization from transfers can temporarily hurt it. But paying down the balance aggressively does improve your score over time by lowering utilization. Understanding what actually moves your credit score helps you set realistic expectations and avoid common misconceptions about how balance transfers affect your credit profile.

Common Mistakes That Turn 0% Cards Into Traps

Here's where good intentions go wrong:

Mistake #1: Treating Available Credit as Spending Money

You transfer $5,000 in debt to a card with a $10,000 limit, see $5,000 available, and think "I have room to spend." Within months, you've maxed out the new card while still carrying balances on your old cards. Now you have $15,000+ in debt instead of $5,000.

The fix: Available credit on a balance transfer card is not spending money. It's emergency-only capacity, and even then, only for genuine emergencies (medical bills, car breakdown), not lifestyle spending.

Mistake #2: Only Making Minimum Payments

Card issuers set minimum payments low (often $25-50 or 1-2% of balance) because they want you to carry a balance after the promo ends. If you only pay the minimum on a $5,000 balance for 18 months, you'll pay off less than $2,000 and owe $3,000+ when the 22% APR kicks in.

The fix: Calculate the payment needed to eliminate the balance by the promo end date and treat that as your actual minimum, not what the issuer suggests.

Mistake #3: Serial Balance Transfer Surfing

Some people get a 0% card, make minimal payments for 18 months, then transfer the remaining balance to a new 0% card, repeating this cycle indefinitely. While this technically avoids interest, you're:

- Paying 3-5% transfer fees repeatedly (adds up to thousands on large balances)

- Never actually eliminating the debt

- Accumulating hard inquiries that damage your credit

- Risking denial eventually (issuers catch on to this pattern)

The fix: Use a 0% card as an opportunity to aggressively eliminate debt, not as a permanent strategy to avoid paying it off.

Mistake #4: Closing Old Cards After Transferring

After transferring balances from your old cards, your instinct might be to close them. Don't. Closing cards reduces your total available credit, which spikes your utilization ratio and hurts your score. Keep them open with zero balances (proving you can have credit without using it), and use them occasionally for small purchases to keep them active.

Real-World Success: Taylor's 18-Month Payoff

Taylor, a 29-year-old graphic designer, accumulated $8,200 across three credit cards at APRs ranging from 19-24%. Her minimum payments totaled $285/month, with roughly $150 going to interest and only $135 to principal.

Her strategy:

- Applied for a 0% APR balance transfer card with an 18-month promotional period

- Transferred all $8,200 (plus 3% fee = $246) for a total of $8,446

- Calculated required payment: $8,446 ÷ 18 = $470/month

- Set up automatic payments of $500/month (giving herself a buffer)

- Physically cut up the new card after the transfer to remove temptation

- Used her tax refund ($1,400) to make an extra payment in month 4

Results: Paid off the entire balance in 16 months (2 months early). Total cost: $246 transfer fee. Money saved compared to keeping debt on original cards: approximately $2,800 in interest charges. Her credit score improved by 45 points as utilization dropped from 75% to 0%.

Key to success: Taylor treated the 0% card as a payoff tool, not as new spending capacity. She also addressed the underlying issue (overspending on dining out and entertainment) by implementing a strict budget and using cash envelopes for discretionary spending.

What Happens After the Promotional Period Ends

Let's be realistic: not everyone will pay off their balance completely before the 0% period expires. Here's what happens and your options:

Scenario 1: You Paid It Off Completely

Congratulations. Now decide: keep the card open with a zero balance (helps your credit history and utilization), or close it if there's an annual fee you don't want to pay. If keeping it open, use it for one small purchase every 6 months and pay it off immediately to prevent closure due to inactivity.

Scenario 2: You Have a Small Remaining Balance ($500-1,500)

The standard APR (usually 18-29%) kicks in, but you're close enough to payoff that you can finish within 3-6 months with aggressive payments. Continue paying as much as possible to minimize interest charges. You'll still have saved substantially compared to never doing the transfer.

Scenario 3: You Have a Significant Remaining Balance ($3,000+)

You have three options:

- Option 1 — Another balance transfer: Apply for a new 0% card and transfer the remaining balance. This works if your credit is still good and you're committed to actually paying it off this time. But you'll pay another transfer fee, and repeated balance transfer surfing isn't a sustainable strategy.

- Option 2 — Negotiate with the issuer: Call and explain your situation. Some issuers will offer hardship programs with lower APRs (maybe 8-12%) if you've been making consistent payments and can demonstrate financial difficulty.

- Option 3 — Accept the higher APR and aggressively pay down: Buckle down and throw every spare dollar at the balance. Even at 22% APR, you're still better off than if you'd never done the transfer in the first place.

Ready to Tackle Credit Card Debt Strategically?

A 0% APR card is a powerful tool, but it's only as effective as the payoff plan behind it. Learn proven strategies for eliminating debt permanently.

Get Your Payoff StrategyFrequently Asked Questions

Will applying for a 0% APR card hurt my credit score?

Yes, but the impact is typically minor and temporary. The application creates a hard inquiry on your credit report, which usually drops your score by 5-10 points. This impact fades within 6-12 months and disappears completely after 24 months. Additionally, opening a new account temporarily lowers your average account age, which can reduce your score by another 5-10 points depending on your existing credit history. However, if you use the card to pay down debt and lower your overall credit utilization, the positive impact on your score (20-50+ point increase from improved utilization) typically outweighs the temporary negatives within 3-6 months. The key is actually paying down the balance rather than maxing out the new card with transfers and then continuing to spend on your old cards, which would spike your total utilization and cause more damage than benefit.

What happens if I miss a payment during the promotional period?

This depends on the card issuer's specific terms, but many cards will immediately revoke your 0% promotional rate if you're 30+ days late on even a single payment. Some issuers go further and retroactively charge interest from the date you opened the account, meaning you'd owe interest on the entire balance from day one as if you never had the promotional rate. This can result in hundreds or thousands in unexpected interest charges. At minimum, a late payment will trigger late fees ($25-40) and be reported to the credit bureaus after 30 days, damaging your credit score by 60-110 points. This is why setting up automatic payments for at least the minimum amount is absolutely critical — you cannot afford to miss payments on a 0% APR card. If you're worried about cash flow, set the autopay for the minimum required amount (which ensures the promo rate stays intact) and then make additional manual payments when you have extra money available.

Is the balance transfer fee worth paying?

Almost always yes, as long as your current APR is 15% or higher and you're carrying the debt for at least 12 months. Here's the math: A 3% transfer fee on $5,000 costs you $150 upfront. If your current card charges 20% APR, you'd pay roughly $1,000 in interest over the next year if you kept the balance there. Even after paying the $150 transfer fee, you save $850 in interest during the promotional period. The higher your current APR and the larger your balance, the more you save despite the fee. The only scenario where a transfer fee doesn't make sense is if you have a very small balance (under $1,500) with a relatively low current APR (12-15%), or if you're absolutely certain you can pay off the debt within 2-3 months anyway. For most people carrying significant high-interest debt, the transfer fee is a small price to pay for 18-21 months of interest-free debt reduction. Some promotional offers occasionally waive the transfer fee entirely, which obviously makes the decision even easier, but don't wait indefinitely for a no-fee offer if you're bleeding interest on your current cards.

Can I transfer a balance from one card to another card from the same bank?

Generally no. Most card issuers explicitly prohibit balance transfers between cards they issue, even if one offers 0% APR. For example, you can't transfer a balance from a Chase Sapphire card to a Chase Freedom Flex card, or from one Citi card to another Citi card. The prohibition exists because banks don't want you moving debt around within their ecosystem at promotional rates — they make money on interest charges, and internal transfers just shuffle money between accounts without generating new customers or profit. If you have debt on multiple cards from different issuers, you can transfer some to a new 0% card while leaving balances on cards that can't be transferred (then focus on paying those down once transfers are complete). Always check the fine print in the balance transfer terms — the issuer will list which banks and types of accounts are excluded from transfers. Attempting a prohibited transfer will either be declined or processed at the standard APR rather than the promotional rate, defeating the purpose entirely.

Should I use the 0% card for new purchases or only for transferred balances?

This depends on the card's terms and your self-control. If the card offers 0% APR on both balance transfers and purchases, and you have a specific, planned expense that you've budgeted to pay off during the promotional period, it can make sense to use the card for that purchase. For example, if you need to replace a broken appliance and can pay it off in 12 months, using a 0% purchase card saves you interest compared to financing through the retailer at 15-25% APR. However, the safer approach is to treat a 0% balance transfer card as a dedicated debt-payoff tool, not a spending card. Here's why: credit card psychology shows that people with available credit tend to spend more, and the mental accounting gets complicated when you're both paying down transferred debt and adding new purchases. You might think "I'm paying $500/month" but not realize that $300 is going toward old debt while $200 is just covering new purchases, meaning you're not making real progress. Best practice: if you must use the card for a planned purchase, put it in your budget as a separate line item with its own payoff schedule, and don't use the card for anything beyond that one planned expense. Better yet, use a different rewards card for purchases and keep the 0% card locked away.

What should I do if I get denied for a 0% APR card?

First, find out why you were denied by requesting the adverse action letter the issuer is required to send you by federal law. Common reasons include: credit score too low (most 0% cards require 670+), too much existing debt relative to income (high debt-to-income ratio), too many recent credit applications (issuers see this as risk), or recent negative marks like late payments or collections. If your credit score is the issue (below 670), focus on improving your score for 3-6 months before reapplying: pay down high-balance cards to lower utilization, ensure all payments are on time, dispute any errors on your credit reports, and avoid new credit applications during this period. If existing debt is the problem, consider alternative strategies: contact your current card issuers to request lower APRs or hardship programs, explore debt consolidation loans (which may have lower rates even without 0% promos), or consult with a nonprofit credit counseling agency about debt management plans. Some people with lower scores find success with secured credit cards that offer brief 0% promotional periods on purchases, though these typically won't allow balance transfers. Don't apply for multiple 0% cards in rapid succession if you're denied — each application creates a hard inquiry, further damaging your approval odds for the next application.

Are there alternatives to 0% APR cards for paying down credit card debt?

Yes, several alternatives exist depending on your situation. Personal debt consolidation loans offer fixed interest rates (typically 8-18% depending on credit) and fixed payment schedules, which can provide more structure than 0% cards if you lack discipline. Home equity loans or HELOCs offer even lower rates (6-10% currently) if you own a home with significant equity, though you're putting your home at risk if you can't repay. Nonprofit credit counseling agencies can negotiate with your creditors to reduce interest rates to 8-12% and consolidate payments into a single monthly amount through a debt management plan, though this closes your accounts and appears on your credit report. Balance transfer checks from existing cards sometimes offer lower promotional rates (5-9% for 12-24 months) without requiring a new card application. Borrowing from retirement accounts like 401(k)s is generally discouraged but may offer lower rates than credit cards — though you're robbing your future and face taxes/penalties if you can't repay. For those with genuinely unmanageable debt ($20,000+ with income under $40,000), debt settlement programs or bankruptcy might be more realistic than trying to pay off everything. The right alternative depends on your total debt amount, credit score, income stability, and self-discipline. A 0% card works best for those with good credit, manageable debt ($3,000-$15,000), and strong commitment to aggressive payoff.

Resources

Related PersonalOne Articles

- Paying Off Credit Cards: Proven Strategies for Lasting Freedom — Comprehensive debt payoff strategies

- The Credit Readiness Framework: When You're Actually Lender-Ready — Assess your readiness before applying

- What Actually Moves Your Credit Score (And What Doesn't) — Understanding credit fundamentals

PersonalOne Calculators & Tools

- Credit Card Interest Calculator — See how much interest you're paying on current balances

- Credit Score Impact Calculator — Model how balance transfers affect your score

External Resources

- CFPB: What Is a Balance Transfer? — Official government explanation

- FTC: Credit and Loans — Consumer protection information

Important Disclaimer

This article is for informational and educational purposes only and does not constitute financial advice. Credit card terms, promotional offers, APRs, fees, and eligibility requirements vary by issuer and are subject to change without notice. The calculations and examples provided are illustrative and may not reflect your actual costs or savings based on your specific circumstances. Before applying for any credit card or making balance transfer decisions, carefully review the terms and conditions provided by the card issuer, and consider consulting with a qualified financial advisor or credit counselor. PersonalOne.org does not endorse specific credit card products and receives no compensation for mentioning card features or issuers in this educational content.