March 6, 2026

Updated: May 24, 2026

Home › Financial Stability › Income Volatility Management

This cluster is part of the Financial Stability guide on PersonalOne — the complete framework for building financial stability through buffers, emergency funds, income protection, and shock absorption systems.

What You Need to Know

— Income volatility means your income changes significantly month to month — freelancers, commission workers, gig economy, seasonal workers, and business owners all face this. Bills stay constant. Income does not.

— The fix is structural, not behavioral. Build a one to two month income buffer so you are always spending last month's money, not this month's. Timing lag creates stability that willpower cannot.

— Budget on 80–90% of your six-month income average — not your best month, not your worst. This gives you margin for volatility without constant shortfalls.

— Variable income workers need a larger emergency fund: 6–9 months minimum, 12 months ideal. Standard three-month advice assumes income is stable. Yours is not.

— The two-account system — Income Holding Account plus Operating Account — keeps volatility contained and spending predictable month to month.

— Never increase fixed expenses during high-income months. The lifestyle you lock in at $10,000 becomes the trap you cannot escape during a $2,000 month.

Most financial advice is built for someone with a consistent paycheck. Budget 30% for housing. Save 20% of every paycheck. Build a three-month emergency fund. All of it assumes your income arrives on schedule in a predictable amount — and for freelancers, commission workers, gig economy workers, seasonal workers, and business owners, that assumption is never true.

Income volatility is not a budgeting problem. It is a structural problem. The income arrives irregularly, in variable amounts, often misaligned with when bills are due. Standard financial tools were not designed for that reality, and applying them without modification creates constant cash flow stress even when total annual income is more than sufficient.

This cluster covers the complete framework for managing variable income — the income buffer that creates timing stability, the averaging method that makes budgeting possible, the two-account system that separates volatility from spending, and the tax planning that keeps quarterly obligations from becoming year-end crises. For the complete financial stability system that this cluster sits within, the Financial Stability hub covers all six layers.

Why Variable Income Breaks Standard Financial Advice

The core problem with variable income is not the amount — it is the timing mismatch. Your expenses arrive on a predictable schedule: rent on the 1st, utilities mid-month, insurance quarterly. Your income arrives unpredictably. That timing gap creates cash flow crises regardless of how much you earn in total.

The people most affected are not those with low incomes. A freelancer earning $80,000 per year but collecting it in uneven lumps can face the same overdraft anxiety as someone earning half that on a steady paycheck — because the problem is structural, not financial. Solving it requires structural tools, not more discipline or more income.

Variable income also makes standard emergency fund advice dangerously inadequate. A three-month emergency fund assumes that your only income risk is job loss. For a variable income worker, income disruption is already baked into every month. A slow period, a lost client, a delayed invoice, or a bad commission month can each create a cash flow crisis without any of them technically being a job loss. The emergency fund has to account for that ongoing volatility, not just catastrophic events.

The sections below cover each structural solution in sequence: the income buffer first, then averaging, then the two-account system, then emergency fund sizing, then seasonal planning, then tax management. Each one addresses a specific failure mode of applying stable-income tools to variable-income life.

The Income Buffer: Spending Last Month's Money

Standard budgeting runs on this assumption: this month's income pays this month's bills. When income is stable and predictable, that works. When income is variable, it creates constant pressure — a low-income month means bills cannot be paid, and a high-income month creates false confidence that leads to overspending.

The income buffer breaks that dependency. The structural shift is simple: this month's income goes into a buffer account. Next month's spending comes out of that buffer. You are always spending last month's money, not counting on this month's to arrive in time.

How the Income Buffer Works

Month 1 — Building Phase: All income goes into the buffer account. You live on whatever savings or previous income you have. This is the hard month — it only happens once.

Month 2 — Transition: Income continues going into the buffer. You spend Month 1's deposit. Your budget for the month is set by what came in last month, not what arrives this month.

Month 3 onwards — Stabilized: The pattern locks in. High-income months build the buffer. Low-income months draw from it. Your spending is always based on a known, already-arrived number.

Result: Income volatility stops producing spending volatility. A bad month does not immediately become a bills crisis. A good month does not immediately become a spending surge. The buffer absorbs both.

Building the buffer from zero requires one month of aggressive saving — banking windfalls, cutting non-essentials temporarily, using high-income months fully. It is the hardest month in the system. After that, it runs automatically.

Income Averaging: How to Budget When Income Fluctuates

Budgeting based on your best month creates lifestyle inflation that a slow month cannot support. Budgeting based on your worst month creates artificial scarcity during periods when you have more than enough. Neither approach fits variable income reality.

The correct approach is averaging. Calculate your total income over the past six months. Divide by six. Budget at 80–90% of that average. The remaining 10–20% provides margin — high months build reserves, low months draw from them, and you are never budgeting at the edge.

Example: Six-Month Income Average

Jan: $4,200 — Feb: $2,800 — Mar: $6,500 — Apr: $3,900 — May: $7,100 — Jun: $4,500

Six-month total: $29,000 — Average: $4,833/month

Budget at 85% of average: $4,108/month — This gives $725/month of margin. High months build reserves. Low months draw on them. You are never spending at the ceiling of what arrived.

Recalculate your average every three months. Income patterns shift as client rosters change, markets evolve, and skills develop. A six-month average that was accurate in January may not reflect reality in July. Quarterly recalculation keeps the budget anchored to actual conditions.

The Two-Account System: Separating Volatility From Spending

Keeping all income and spending in a single checking account makes volatility visible in the worst possible way — the balance swings wildly, you never know how much is actually safe to spend, and the anxiety is constant. The two-account system eliminates that entirely.

Account 1 — Income Holding Account

— All income deposits here first. Invoices, paychecks, tips, transfers — everything lands here.

— The balance fluctuates wildly. That is its job.

— You never spend directly from this account.

— At the start of each month, transfer your averaged budget amount to the Operating Account.

Account 2 — Operating Account

— Receives a fixed monthly transfer from the Income Holding Account.

— All bills autopay from here. All spending comes from here.

— The balance is always predictable — you put in a known amount at the start of the month.

— When it reaches zero, spending stops. The limit is structural, not willpower-dependent.

This system keeps income volatility in the Income Holding Account where it belongs — the Operating Account sees a consistent monthly deposit regardless of what the market, clients, or commissions did that month. Spending behavior normalizes. The anxiety of not knowing what is safe to spend disappears.

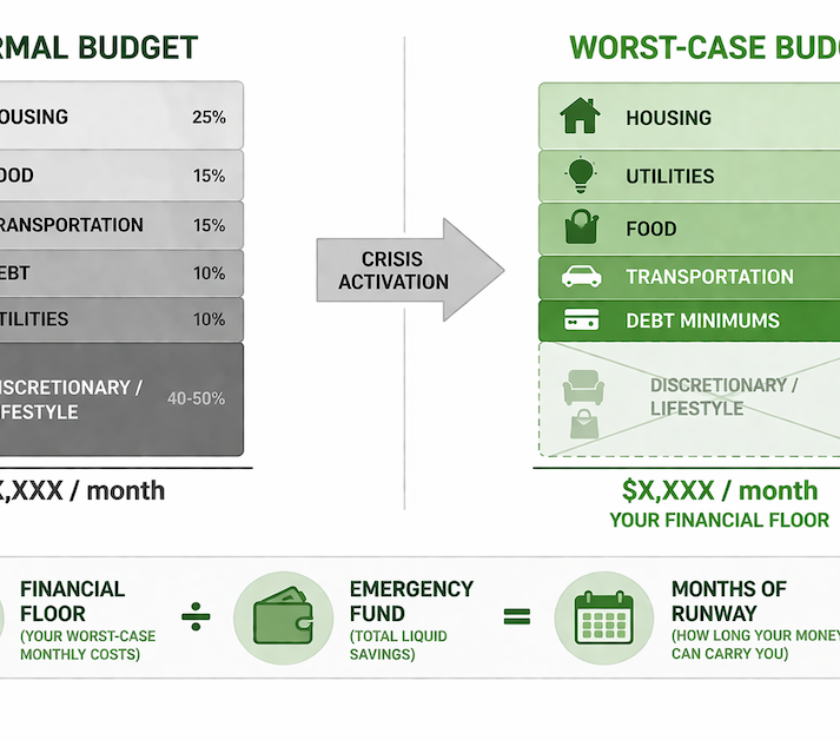

Emergency Fund Sizing for Variable Income

Standard emergency fund advice — three to six months of expenses — assumes that job loss is the primary risk and that income is otherwise stable. For variable income workers, income disruption is not a risk to prepare for. It is already built into every month. A lost client, a slow quarter, a delayed invoice, or a bad commission stretch can create the same cash pressure as job loss without technically being job loss.

Emergency Fund Targets by Income Type

Stable W-2: 3–6 months — income predictable, job loss is the primary risk, standard timeframe covers job search.

Commission-based W-2: 6 months — base salary provides floor but commission swings require additional buffer.

Established freelancer/contractor: 6–9 months — client loss, slow periods, and invoice delays compound. Larger buffer required.

New freelancer, seasonal, or gig worker: 9–12 months — highest volatility, least predictable income, longest rebuilding timeline. Maximum protection needed.

Calculate your target using average monthly survival expenses — not average income, not normal spending. Survival expenses are the essentials that cannot be cut: rent, utilities, minimum debt payments, basic groceries, essential transportation, insurance. Multiply that number by your target months based on income type. That is your fund target.

Preparing for Predictably Low Months

Most variable income is not randomly volatile — it follows seasonal and cyclical patterns. January and August are slow for many freelancers. November and December are high-volume for retail and e-commerce. Real estate peaks in spring and summer. B2B services often slow in Q4 as clients finalize budgets. The pattern repeats year over year.

Identifying your low months turns a recurring crisis into a manageable predictable event. Pull 12–24 months of income data. Mark your three or four lowest-income months. They are almost certainly consistent. Once identified, the response is straightforward: build extra buffer in the two to three months before the slow period begins, compress discretionary spending during it, and schedule large annual expenses — insurance renewals, registration fees, professional memberships — to hit during high-income months, not low ones.

The key principle is that a predictable problem is not an emergency — it is a planning problem. The expense compression strategies and survival budgeting tools that apply when a shock hits also apply to slow season preparation. They just get deployed in advance rather than in response.

Tax Planning for Variable Income

W-2 employees have taxes withheld automatically. Variable income workers — 1099 contractors, freelancers, self-employed, and business owners — handle their own. No withholding happens automatically. Quarterly estimated payments are required. The failure to plan for this is one of the most common and most damaging financial mistakes variable income workers make.

The correct approach is automatic: set aside 25–30% of every payment the day it arrives into a dedicated tax savings account. That account does not get touched except for quarterly estimated payments on April 15, June 15, September 15, and January 15, and the annual April filing. Treat it as already spent the moment it goes in.

Recalculate the liability quarterly based on actual year-to-date income. Income changes mean tax liability changes. Adjusting in real time prevents the end-of-year surprise of owing a large amount you do not have. If you are uncertain about your exact rate, overpay slightly — a small refund is a minor inconvenience, an unexpected large tax bill is a financial crisis.

Build Complete Financial Stability

Income volatility management is one cluster in the complete financial stability framework. Emergency funds, buffer accounts, shock absorption, and long-term resilience all connect. See the full system at the Financial Stability hub.

Go Deeper: Income Volatility Management Guides

This hub covered the complete framework. The articles below go deep on the specific situations, scenarios, and execution details that the framework surfaces.

Irregular Income Survival Guide: How to Stay Stable When Pay Fluctuates

The complete playbook for living on unpredictable income — how to build the structural systems that create stability regardless of what arrives each month and how to respond when a low-income stretch hits without a plan.

How to Plan Your Budget Around a Variable Paycheck

The step-by-step budgeting method for income that changes month to month — how to calculate your working budget, when to adjust it, and how to protect fixed obligations when variable income dips below average.

How to Build Stability on a Minimum Wage Income

The structural approach to financial stability when income is both low and variable — which buffers to build first, how to sequence savings when every dollar is already spoken for, and what stability actually looks like at the income floor.

How to Build an Income Buffer From Zero — Coming Soon

The month-by-month plan for creating a one-month income lag when starting from nothing — how to fund the buffer using high-income months, windfalls, and temporary expense compression without going into debt to do it.

Tax Planning for Freelancers and Self-Employed Workers — Coming Soon

The complete quarterly tax system for variable income earners — how to calculate your reserve percentage, when and how to pay estimated taxes, and how to prevent the year-end tax bill from becoming an annual financial shock.

How to Prepare for a Slow Season Before It Hits — Coming Soon

Seasonal income patterns, how to identify your low months, and the advance preparation system that turns a recurring crisis into a manageable planned event.

The Two-Account System for Variable Income: Step-by-Step Setup — Coming Soon

How to open, fund, and operate the Income Holding and Operating Account setup — which institutions to use, how to automate the monthly transfer, and how to handle edge cases like an unusually low-income month.

Emergency Fund Size for Freelancers and Variable Income Workers — Coming Soon

Why the standard three-month emergency fund target fails variable income workers, how to calculate the right target for your specific income pattern, and how to build toward it while managing current volatility simultaneously.

Resources

Official Sources

IRS — Self-Employed Individuals Tax Center

IRS Form 1040-ES — Estimated Tax for Individuals

CFPB — Bank Account Tools and Consumer Rights

Related PersonalOne Guides

Financial Stability Hub — The complete stability framework across all six clusters

Emergency Fund Strategy — How to size and build the cash reserves that variable income workers need larger than most

Financial Shock Absorption — The layered protection system that handles income disruption at every severity level

Frequently Asked Questions

How long does it take to build an income buffer from zero?

For most people, three to six months of aggressive saving. Calculate your average monthly income, bank every dollar above survival minimum, and use any windfalls or tax refunds to accelerate. If you average $4,000 per month and can save $1,000 per month above survival expenses, you will hit a one-month buffer in four months. The first month is the hardest — after that the system runs without ongoing effort.

Should I average income over three months or six months?

Six months for most variable income workers — it smooths out peaks and valleys better and produces a more stable budget baseline. If your income is moderately stable with occasional variation, three months responds faster to real trend changes. After six to twelve months of tracking your own pattern you will know which timeframe fits your specific income cycle.

What if I have multiple income sources with different timing?

Treat all income as one pool in the Income Holding Account. It does not matter whether $3,000 arrives from one client on the 5th and $2,000 from another on the 23rd — everything lands in the same holding account. The transfer to the Operating Account happens at the start of each month on a fixed schedule, regardless of which sources paid when. Multiple income sources actually help because they are rarely correlated — a slow month with one client is often offset by a stronger month with another.

How do I handle large irregular expenses like annual insurance or quarterly subscriptions?

Two approaches work: divide the annual cost by twelve and move that amount monthly into a sinking fund, so the money is already set aside when the bill arrives; or deliberately schedule renewals during your predictable high-income months so the bill hits when you have the most cash available. Most providers allow renewal date adjustments. Use that flexibility.

Should I try to reduce income volatility or just manage it better?

Both, but in sequence. Short-term: build the structural systems that manage existing volatility — the buffer, averaging, two-account system. These create stability now without waiting for income to stabilize. Long-term: work toward reducing volatility through retainer clients, passive income streams, or more specialized skills that command higher and more consistent rates. Do not wait for perfect income stability before implementing stability systems. Build the structure now and reduce the underlying volatility over time.

PersonalOne Money System

This content is researched, written, and owned by PersonalOne — a free financial education platform built to help Millennials and Gen Z build real financial systems.

Disclaimer: This content is for educational purposes only and does not constitute financial, tax, or accounting advice. PersonalOne is not a licensed financial advisor, CPA, or tax professional. Income volatility management strategies, tax planning, and emergency fund recommendations should be tailored to your individual circumstances. Self-employment and freelance income have specific tax requirements that vary by jurisdiction — consult a qualified tax professional for personalized guidance.