February 24, 2026

Last updated: February 24, 2026

Home >

Money Through Life Stages >

Careers and Financial Impact

About the Author: Don Briscoe is a financial systems coach with 12+ years helping Millennials and Gen Z escape paycheck-to-paycheck cycles. He's worked with hundreds of people to build emergency funds, eliminate debt, and start investing using framework-first strategies that require less willpower and more infrastructure. He founded PersonalOne to provide the financial education he wished existed—structured, honest, and free.

TL;DR

- Your career choice affects every stage of the PersonalOne Money System.

- Income stability determines how fast you build emergency funds.

- Education costs directly impact debt, credit, and long-term wealth.

- Salary growth affects investing power and timeline to financial independence.

- The right career decision isn’t just about passion — it’s about financial architecture.

- Before pursuing any career path, evaluate income potential, debt risk, and system impact.

Choosing a career is often framed as a passion decision. “Do what you love.” “Follow your dreams.” But from a financial systems perspective, a career is not just an identity choice — it is a structural decision that impacts every stage of your money architecture.

A career determines income velocity, debt exposure, stress tolerance, geographic flexibility, and wealth-building capacity. It influences how quickly you move through Stage 1 (Financial Stability), how efficiently you structure Stage 2 (Banking Systems), and how aggressively you can build Stage 5 (Investing & Wealth Growth).

If you ignore the financial implications of a career path, you may unknowingly design a system that struggles for decades.

Why Career Decisions Belong Inside the PersonalOne Money System

The PersonalOne framework is sequential. Every stage builds on the previous one. Your career is the engine that powers the system.

- Stage 1: Financial Stability — Income determines how fast you build buffers.

- Stage 2: Structure & Control — Predictable pay affects account architecture.

- Stage 3: Credit Authority — Debt from education influences credit trajectory.

- Stage 4: Automation — Stable income makes automation sustainable.

- Stage 5: Investing — Surplus income fuels compounding.

- Stage 6: Income Expansion — Career growth accelerates the entire system.

According to the U.S. Bureau of Labor Statistics, median weekly earnings vary dramatically by education level and occupation. Workers with bachelor’s degrees earn significantly more than those without, but they may also carry substantial student debt (BLS.gov).

Career decisions must be evaluated through both sides of the equation:

Income Potential vs. Cost of Entry

The Hidden Financial Variables Behind Career Choices

1. Education Debt Exposure

The Federal Reserve reports that student loan debt in the U.S. exceeds $1.7 trillion (FederalReserve.gov). Some careers require advanced degrees, which means delayed earnings and high repayment burdens.

Before pursuing a career that requires significant education:

- Calculate total tuition cost.

- Estimate expected starting salary.

- Model repayment timeline under realistic scenarios.

- Compare debt-to-income ratio at graduation.

If your expected starting salary is $55,000 but debt exceeds $120,000, your Stage 3 (Credit & Debt) will be under pressure for years.

2. Income Stability

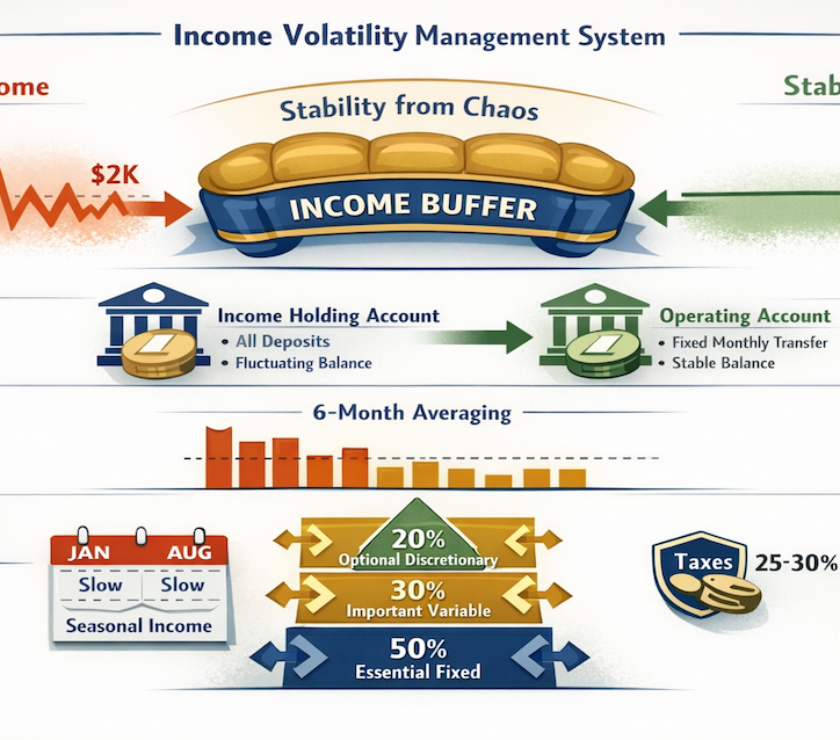

Some careers offer predictable salaries. Others rely on commissions, contract work, or seasonal income.

Irregular income affects:

- Emergency fund size requirements

- Buffer layering in Stage 1

- Banking architecture in Stage 2

- Automation feasibility in Stage 4

Entrepreneurs and freelancers must build larger income buffers before advancing to aggressive investing strategies.

3. Income Ceiling vs Growth Potential

Some professions cap out early. Others scale dramatically over time.

The difference between a career that tops out at $70,000 and one that scales beyond $150,000 over 15 years changes:

- Total lifetime earnings

- Investment contributions

- Retirement timeline

- Financial independence trajectory

Career growth rate influences how quickly Stage 5 compounds.

Internet Red Flags: What Career Advice Gets Wrong

Social media often promotes extremes:

- “College is useless.”

- “Quit your job and start a business immediately.”

- “Six-figure jobs are easy.”

These statements ignore system sequencing.

A business started without Stage 1 stability increases collapse risk. A degree pursued without financial modeling creates debt strain. The correct approach is integration — aligning career ambition with financial architecture.

Career Decision Checklist (System-Based)

Before committing to a new career path, ask:

- What is the realistic starting salary?

- What is the 5-year salary trajectory?

- How much debt will this require?

- What is the employment stability?

- Does this career allow geographic flexibility?

- How will this affect my emergency fund timeline?

- Will automation be sustainable?

This moves you from emotional decision-making to structural evaluation.

Related: If you are still building income capacity, review the Income Expansion Hub to understand how multiple income streams accelerate every stage of the system.

Career Transitions and System Disruption

Changing careers resets parts of your system.

A transition may:

- Reduce income temporarily

- Interrupt investing contributions

- Increase short-term expenses

- Impact credit utilization

Before making a transition:

- Build 6–12 months of reserves.

- Pause non-essential financial risk.

- Protect credit standing.

- Maintain automation discipline.

Career changes are not dangerous — unplanned transitions are.

Career Choice and Long-Term Wealth

The Social Security Administration shows lifetime earnings significantly affect retirement income (SSA.gov).

Higher lifetime income:

- Increases 401(k) contributions

- Accelerates Roth IRA funding

- Allows taxable brokerage investing

- Improves retirement security

Career decisions compound — just like investments.

When Passion and Profit Conflict

Some careers offer fulfillment but modest pay. Others offer strong income but low satisfaction.

The system approach asks:

Can I design balance?

- High-income primary career + passion side hustle

- Moderate income career + aggressive investing discipline

- Lower income career + dual-income household strategy

You don’t need the “perfect” career. You need one that fits your money system.

The Long Game Perspective

Most career decisions are viewed short-term. But from a system perspective:

- What does this look like in 10 years?

- Does this career support Stage 5 wealth building?

- Can this income sustain Stage 4 automation?

- Will this path increase or decrease financial stress?

Career is not separate from money. It is the foundation of income architecture.

Final Thought: Design Your Income Engine Intentionally

The PersonalOne Money System is sequential. It is infrastructure-based. It is long-term.

Your career powers every stage. Choose it strategically. Model it financially. Integrate it structurally.

Align Your Career With Your Financial System

Before making your next career move, review the complete 7-stage framework and understand how each decision affects your long-term wealth trajectory.

Explore the PersonalOne Money SystemAuthoritative Sources

- U.S. Bureau of Labor Statistics — https://www.bls.gov

- Federal Reserve — https://www.federalreserve.gov

- Social Security Administration — https://www.ssa.gov

Financial Disclaimer

This content is for educational purposes only and does not constitute financial, legal, tax, or career advice. Individual circumstances vary. Consult qualified professionals before making significant financial or career decisions.