April, 2026

Home › Financial Stability › Financial Shock Absorption › Emergency Budget Plan

What You Need to Know

— An emergency budget plan has one goal: get your monthly spending below your available income or benefits as quickly as possible

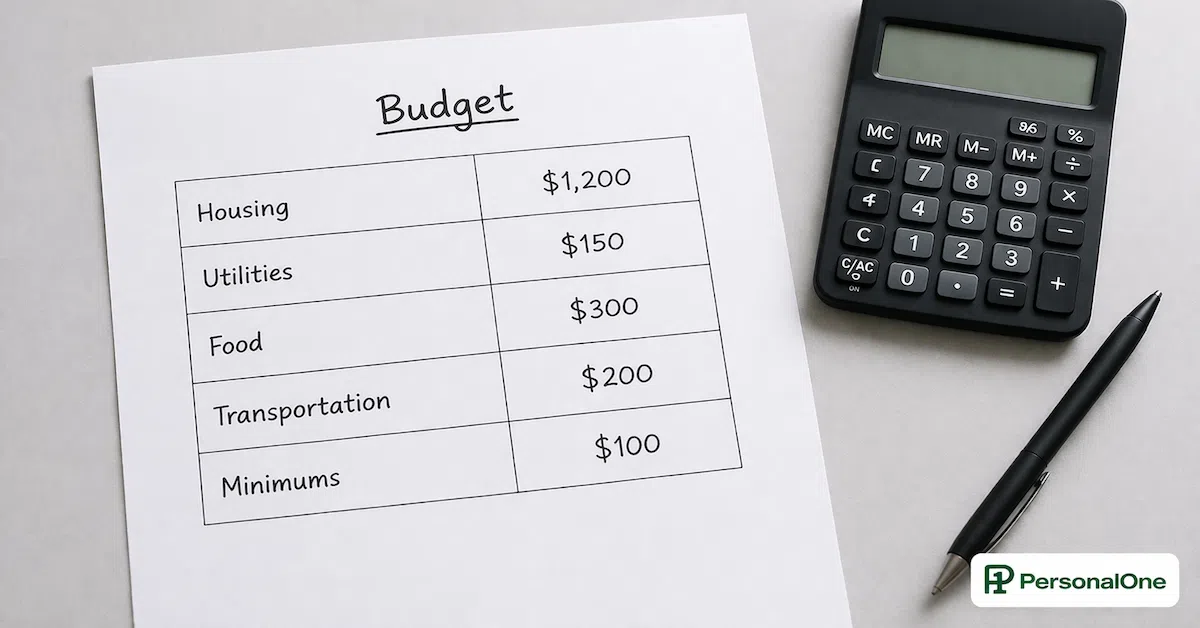

— A bare-bones budget includes only five categories: housing, utilities, food, transportation, and minimum debt payments — nothing else

— Most people discover their bare-bones monthly number is significantly lower than their normal spending — often 40–60% less

— The minimum survival budget is not about deprivation — it is about clarity. Knowing your true floor eliminates the financial anxiety of not knowing

— This budget is temporary. Define a specific income trigger that returns you to your normal budget structure

An emergency budget plan is the structured financial response to income disruption — a bare-bones budget that covers only survival expenses while extending your available cash runway as far as possible. Most people in a financial crisis are spending more than they need to because they have not done the specific calculation of their minimum survival budget. Doing that calculation is the first action of a financial shock absorption strategy that actually works. The complete framework for shock absorption is in the Financial Shock Absorption guide.

The value of building an emergency spending plan is not just the savings it produces — it is the clarity it creates. When you know your exact bare-bones number, you can calculate precisely how many months your emergency fund and any benefits will last. That calculation removes the fear of the unknown and replaces it with a specific timeline you are working within. How this connects to your broader financial stability system is covered in the financial stability guide.

Step 1: Calculate Your True Bare-Bones Number

Your bare-bones number is the minimum monthly amount required to maintain shelter, basic utilities, food, transportation, and minimum debt obligations. Nothing else. Open your last three months of bank and credit card statements and identify every recurring charge. For the emergency budget, categorize each charge as either:

Bare-Bones Budget Categories (Include Only These)

✓ Rent or minimum mortgage payment

✓ Electricity, gas, water (at reduced usage)

✓ Groceries — home cooking only, no dining out

✓ Transportation to work or job search (fuel + insurance minimum)

✓ Health insurance (minimum coverage to stay insured)

✓ Minimum debt payments (credit cards, loans)

✓ Phone (minimum plan only)

✓ Internet (minimum plan required for job search)

Everything else — subscriptions, dining out, entertainment, clothing, gym memberships, non-essential insurance riders, savings contributions above minimum survival — is temporarily suspended. Add up every item in the bare-bones list. That total is your emergency budget number.

Step 2: Calculate Your Runway

With your bare-bones number calculated, determine your available cash: emergency fund balance plus expected monthly unemployment benefits or any other income. Divide total available cash by your monthly bare-bones number. The result is your runway in months.

Example: Emergency fund of $6,000 plus $1,400/month unemployment = approximately $2,600 effective monthly resource if you are drawing $1,200/month from savings. At a bare-bones budget of $2,400/month, this produces roughly 5 months of runway. Knowing this specific number is the difference between unfocused anxiety about money running out and a defined 5-month window to resolve income.

Step 3: Identify Any Negotiated Reductions to Lower the Number Further

Once you have your initial bare-bones number, go through each line item and identify which ones can be reduced through provider contact. Auto insurance may qualify for a low-mileage rate if you are not commuting. Credit card minimums may be reducible through hardship programs. Utilities may qualify for assistance programs. Each negotiated reduction extends your runway further.

Document every negotiated reduction with the provider name, date, agreement terms, and any reference numbers. Treat these as formal agreements. If a provider agrees to reduce your payment and later charges the original amount, having documentation allows you to dispute the charge and enforce the agreement.

Step 4: Define the Trigger That Ends the Emergency Budget

An emergency budget without a defined end condition tends to become permanent even after the emergency passes. Before you implement it, define the specific income or financial milestone that triggers a return to your normal budget: new employment with X monthly take-home, emergency fund rebuilt to $Y, or a specific date if income recovery has a predictable timeline. This trigger keeps the emergency budget what it is supposed to be — temporary — and gives you a goal rather than just a constraint.

Know your number. Know your runway. Operate with clarity.

The complete Financial Shock Absorption guide covers every tactical step for managing income disruption — from the emergency budget through creditor negotiation and recovery.

Explore Financial Shock Absorption →Resources

Official Sources

CFPB — Budgeting and Spending Tools — Consumer Financial Protection Bureau budget-building tools and guidance on building an emergency spending plan calibrated to reduced income.

BLS — Consumer Expenditure Survey — Bureau of Labor Statistics data on average household spending by category — the benchmark for understanding which of your expense categories have the most room for reduction.

Return to the financial stability guide for the complete system this cluster is part of.

Frequently Asked Questions

How low can a bare-bones budget realistically go?

For a single person renting in a mid-cost city, a genuine bare-bones budget typically falls between $1,800 and $2,800/month covering rent, utilities, groceries, transportation, health insurance, and minimum debt payments. For a couple in a lower-cost area with no debt beyond a car payment, it may be as low as $2,200–$3,000. For households with mortgages or significant debt minimums, the floor is higher. The calculation must use your actual numbers — not national averages.

Should I include savings contributions in my emergency budget?

Only to the extent required to capture an employer retirement match. Above-match retirement contributions, additional emergency fund contributions, and any discretionary savings are suspended during the emergency budget period. The emergency fund itself is the savings mechanism during a crisis — the goal is to draw from it as slowly as possible, not to add to it while income is disrupted.

What about irregular expenses that fall during the crisis period?

Car registration, insurance renewals, and similar irregular expenses that fall during the crisis period need to be accommodated within the bare-bones budget in the month they occur. Identify any such expenses in the coming 90 days when you build the budget and add them as one-time line items in the relevant months. Failing to plan for them creates budget surprises that feel like new crises even though they were predictable.

Disclaimer: This article is for informational and educational purposes only. Budget figures are illustrative estimates — calculate your actual numbers from your own expense data.