June 15, 2026

Home › Financial Stability › Expense Compression › The 7-Day Spending Audit: Find the Leaks in Your Budget

What You Need to Know

— A spending audit is not a budget — it is a diagnostic tool that reveals where money is actually going versus where you think it goes

— Most people discover 10 to 25 percent of monthly spending goes to categories they cannot clearly account for when asked

— Seven days of tracked spending produces enough data to identify your highest-impact leak categories without requiring a full month of effort

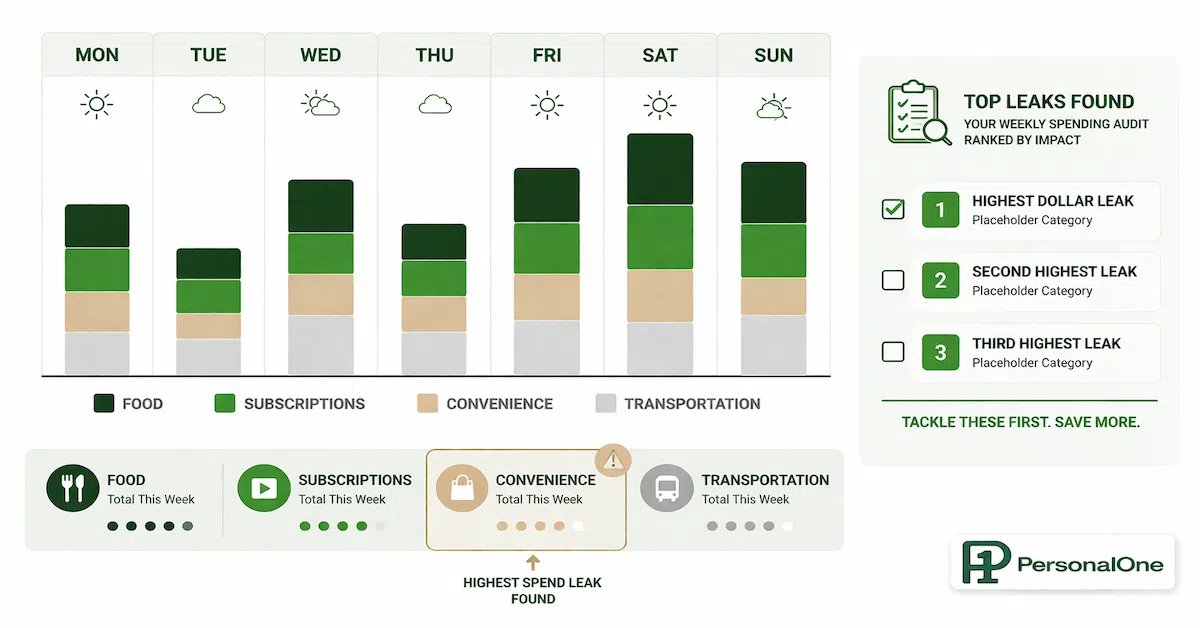

— The audit has three outputs: a spending map, a leak list, and a ranked action list — each builds on the last

— The goal is clarity, not judgment — what you find is data, not a verdict on your financial character

A 7-day spending audit is the fastest way to find the leaks in your budget — the recurring charges you forgot about, the spending categories that quietly consumed far more than you planned, and the patterns that explain why your balance is lower than your income should allow. Most people skip this step and jump straight to building a budget. That approach fails consistently because a budget built on estimated spending, rather than actual spending data, misses the real problem by design.

The expense compression strategy starts here — with visibility. You cannot compress what you cannot see. This audit gives you the complete spending map that makes every subsequent financial decision more accurate and more effective. The expense compression strategy is built around the principle that most households are spending significantly more than they realize in two or three specific categories, and that identifying those categories is worth more than any generic budgeting advice.

Seven days is the right window. Long enough to capture the full weekly spending cycle including weekend patterns. Short enough that you can maintain consistent tracking without audit fatigue. Long enough to surface the recurring charges that hit monthly but happen to fall within the window.

What a Spending Audit Is — and What It Is Not

A spending audit is a structured review of every financial transaction over a defined period. It is not a budget. It is not a spending plan. It is not a commitment to change anything. It is a diagnostic exercise that produces accurate data about where your money actually went.

The distinction matters because most people approach budgeting with assumptions about their spending that turn out to be wrong. They estimate they spend $400 per month on food and discover through an audit that the real number is $680 — split across groceries, delivery apps, coffee, and convenience store stops they did not count as food spending. They assume their subscriptions total $50 per month and find $140 in recurring charges spread across a dozen services, several of which they had forgotten entirely.

The audit replaces assumptions with facts. Once you have facts, building an effective compression strategy becomes straightforward. Without facts, every budget is a guess layered on top of an existing pattern you do not fully understand. A useful companion after the audit is the 50/30/20 budget calculator, which lets you map your actual spending against the framework targets once you know your real numbers.

Before You Start: Set Up the Tracking System

The audit requires a tracking method you will actually use for seven consecutive days. The method matters less than the consistency. Options that work: a notes app on your phone where you record each transaction immediately after it happens, a simple spreadsheet with date, amount, category, and merchant columns, or a banking app that automatically categorizes transactions if you review and correct the categories daily. What does not work: trying to reconstruct spending from memory at the end of each day, or waiting until the week is over to review statements.

Set up six spending categories before you start. These are broad enough to capture everything without creating decision fatigue about which category each transaction belongs to: Housing and Utilities, Food and Drink, Transportation, Subscriptions and Services, Personal and Lifestyle, and Debt Payments. Every transaction fits somewhere in these six. If something genuinely does not fit, add a seventh category called Other and note what it was.

Pull your last three months of bank and credit card statements before Day 1. You will not track these — you already have the data. But reviewing them during the audit week gives you the historical context to know whether what you observe in seven days is typical or atypical. It also surfaces monthly charges that may not fall within your seven-day window but are still part of your real spending picture.

Day 1 Through 3: Track Everything Without Editing

The first three days are pure data collection. Record every transaction as it happens. The coffee. The gas. The impulse purchase at checkout. The automatic charge that hit overnight. Do not evaluate. Do not categorize as good or bad. Do not make any spending decisions based on what you see. The goal for these three days is a complete, unedited record.

The most important instruction for this phase: capture cash spending. Electronic transactions appear automatically on statements, but cash spending disappears completely if you do not log it in the moment. If you withdraw cash or make a purchase with cash, record it immediately — amount, approximate category, and what it was for. Cash leaks are often the most surprising finding in a spending audit because they are completely invisible to any retrospective review.

Also capture subscriptions during this phase. Go into your email and search for billing receipts, confirmation emails, and renewal notices. Cross-reference these against your bank and credit card statements. List every recurring charge you find — amount, frequency, what it is for, and whether you have used it in the last 30 days. This list is often the highest-value output of the entire audit. A well-executed fast expense reduction plan almost always starts with subscription elimination because it produces immediate recurring monthly savings with one cancellation action.

Day 4 and 5: Identify the Patterns

At the midpoint, take your tracked data and look for three things: category totals, frequency patterns, and category surprises.

Category totals. Add up everything in each of your six categories through Day 4. Multiply by 30 to get a rough monthly projection. Compare each category projection to what you estimated you spend before the audit began. The categories where the projection significantly exceeds your estimate are your primary leak candidates.

Frequency patterns. Look at how often you spent in each category. Daily coffee purchases produce a different compression opportunity than a single large dining out charge. High-frequency small purchases in a category often produce more monthly spend than one or two larger purchases because they feel individually insignificant. The accumulation is only visible when you total them.

Category surprises. Note any transaction that surprised you when you saw it in the record. Either because you forgot about it, because the amount was higher than you thought, or because you genuinely cannot recall making the purchase. Surprises are the audit finding with the highest action value — they represent spending that produced no deliberate decision and is therefore easiest to eliminate without lifestyle impact.

Day 6 and 7: Complete the Map and Build the Leak List

Continue tracking through Days 6 and 7. By the end of Day 7, total every category. Add the subscription list to the overall category it belongs to. Pull the last three months of statements and identify any recurring charges that did not appear during your seven-day window — quarterly subscriptions, annual fees, insurance premiums — and convert these to monthly equivalents by dividing by 3 or 12 as appropriate.

Now build the leak list. A leak is any spending that meets at least one of these criteria: you would not have made the purchase if you had been actively aware of your running total; the category total significantly exceeded your estimate; the charge is recurring and you cannot name a clear value you receive from it; or the purchase was a convenience substitute for a cheaper alternative that you had access to. Your leak list is not a list of bad decisions — it is a list of compression opportunities with confirmed dollar values attached.

Rank the leak list by monthly dollar impact, highest to lowest. This ranking becomes your action list. The top items on the list produce the most monthly savings per action taken. The financial stability system at PersonalOne is built on the principle that finding these high-impact leaks is always the first step before any structural financial change — because compression frees up the margin that makes every other financial goal easier to execute.

See the leaks. Then compress them.

This audit is the first step in the Expense Compression system. The complete framework for cutting spending fast and sustaining the compression is in the cluster hub.

Expense Compression Strategy →After the Audit: What to Do With What You Found

The audit produces data. Data requires decisions. Work through your ranked leak list from the top. For each item, decide one of three things: eliminate it permanently, reduce it to a defined lower amount, or keep it intentionally because the value is genuine and the cost is conscious. Every item gets one of these three designations — no item stays in the unexamined middle where it was before the audit.

Execute eliminations immediately. Cancel subscriptions on the day you decide to cancel them. Do not wait for the next billing cycle, do not flag it to do later, do not tell yourself you will remember. If you identified a recurring charge as a leak, the cancellation takes three minutes and produces monthly savings starting now.

For category reductions, set a specific ceiling — not a vague intention to spend less. If your food spending leaked by $200 per month beyond what you thought, decide on a specific reduced target and a specific method for staying within it: a weekly grocery budget with a cash envelope, a meal planning commitment that eliminates delivery spending, or a defined number of dining out occasions per month. Vague reduction intentions do not hold. Specific ceilings with defined methods do. The emergency budget plan framework gives you the structure to formalize these ceilings into a complete compressed spending plan if the audit revealed significant leaks across multiple categories.

Resources

Official Sources

CFPB: Budget and Spending Tools — Consumer Financial Protection Bureau tools for tracking spending, building a budget, and understanding where your money goes.

BLS: Consumer Expenditure Survey — Bureau of Labor Statistics national data on average household spending by category — a useful benchmark for understanding whether your category totals are above or below typical patterns.

FDIC: Money Smart Financial Education — FDIC financial literacy program covering budgeting, tracking spending, and building financial awareness as foundational money management skills.

Continue Building Your Expense Compression System

This audit is the first step in the complete Expense Compression framework. The full system — including fast expense cuts, the needs vs wants framework, and lean living without lifestyle destruction — lives in the Expense Compression cluster hub inside the Financial Stability authority hub.

Frequently Asked Questions

Do I need a special app to do a spending audit?

No. A notes app, a spreadsheet, or pen and paper works. The tool is irrelevant — the habit of recording every transaction as it happens is what produces accurate data. Many banking apps now offer transaction categorization that can supplement your manual tracking, but they should not replace it because automatic categorization frequently miscategorizes transactions and misses cash spending entirely.

What if my spending during the audit week is not typical?

Run the audit anyway and note what was atypical. An audit during a week with a large one-time purchase or an unusually social weekend still produces useful data about your subscription landscape, your daily spending habits, and your category patterns. Supplement the seven-day data with your last three months of statements for categories that felt atypical during the window.

How often should I run a spending audit?

Once fully, then a lighter version quarterly. The initial seven-day audit establishes your baseline. A quarterly check — reviewing the previous month's statements against your category targets — catches new leaks that appear as circumstances change: new subscriptions you added and forgot, lifestyle creep in a specific category, or a new spending pattern that emerged without deliberate decision-making.

What is the most common spending leak people find?

Food spending is the most consistently underestimated category. Most people significantly undercount food costs because they mentally track grocery spending but do not include coffee, delivery apps, convenience store purchases, and work lunches in the same mental bucket. When all food-related spending is combined into a single category total, the real number is typically $150 to $400 higher per month than the estimate.

Should I tell my partner or family members about the audit?

If they contribute to household spending, yes — their tracking needs to be included for the data to be complete. The most effective approach is to do the audit together as a household exercise rather than as an individual one, because household spending leaks often sit in the categories each person assumes the other is managing.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial or legal advice. Individual financial situations vary. Consult a qualified financial advisor before making significant financial decisions. PersonalOne is not a licensed financial advisor.