April, 2026

Home › Investing & Wealth Growth › Investing in Retirement & Later-Life Wealth Decisions

TL;DR

— Retirement investing is not the same as pre-retirement investing — the objective shifts from maximizing growth to sustaining income and protecting purchasing power.

— The central problem in later-life investing is no longer how to build wealth, but how to convert a portfolio into reliable cash flow without draining it too fast.

— Sequence of returns risk, withdrawal timing, inflation, taxes, and healthcare costs become more important than they were during the accumulation phase.

— A retirement portfolio still needs growth, but it needs structure even more — growth alone does not solve withdrawal risk.

— This cluster is where the PersonalOne Money System shifts from wealth accumulation to later-life wealth decisions, retirement income design, and long-term portfolio durability.

Most investing education is written for people who are still in the accumulation years. The assumptions underneath that advice are simple: you are earning income, adding new money to your accounts, and letting time do the heavy lifting. In that phase, mistakes can often be corrected with more contributions, more years of compounding, or a simple course correction in asset allocation.

Retirement changes the math. Once the paycheck slows or stops, the portfolio must do a different job. It is no longer just a growth engine. It becomes an income source, a volatility absorber, and in many cases the primary financial infrastructure supporting the rest of life. That is why retirement investing belongs in its own cluster rather than being treated like a footnote inside beginner investing or general portfolio design.

This cluster exists to deal with the questions that appear only after the accumulation system is already functioning: How much can safely be withdrawn? How should the portfolio be positioned when losses early in retirement matter more than losses ten years earlier? How should income be layered between accounts, Social Security, and taxable withdrawals? How should an investor think about stability without becoming so conservative that inflation quietly destroys the plan?

Those are not beginner questions. They are later-stage wealth questions. They sit at the far end of the PersonalOne system because they only become relevant after the earlier layers — financial stability, account structure, savings discipline, debt cleanup, and long-term investing consistency — are already in place.

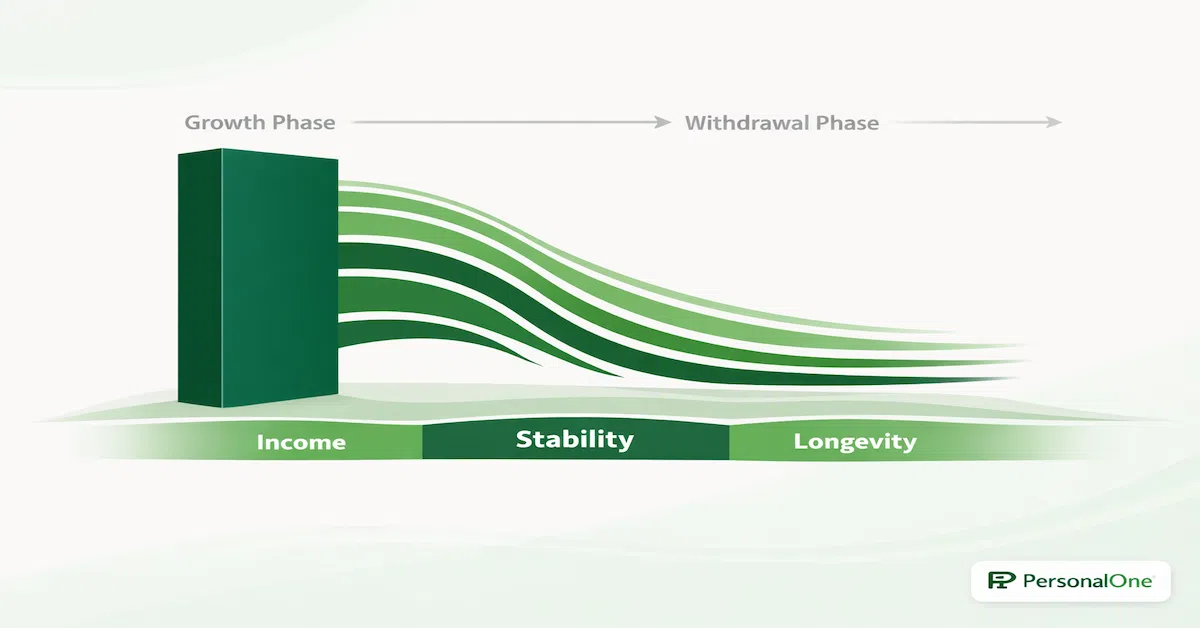

The Core Shift: From Accumulation to Distribution

The clearest way to understand this cluster is to understand the difference between accumulation and distribution.

During accumulation, the question is usually: How do I grow this portfolio as efficiently as possible? During distribution, the question becomes: How do I draw from this portfolio in a way that is sustainable, tax-aware, and emotionally stable?

That shift sounds small, but it changes the entire design of the system. In accumulation, volatility is uncomfortable but often beneficial if you are still contributing. Market declines mean you are buying future returns at lower prices. In retirement, the same decline can become far more dangerous because money may be leaving the portfolio at the same time the asset base is shrinking.

This is why retirement investing cannot simply reuse accumulation logic. The objective is not to eliminate growth; a portfolio still needs growth to keep up with inflation and longevity. The objective is to balance growth with durability. That balance is the center of this cluster.

The Real Problem Is Not Just \"How Much Do I Have?\" It Is \"How Does It Behave Under Pressure?\"

People often frame retirement readiness as a single number problem. They want to know whether they have enough. The more useful question is whether the portfolio behaves well under the pressures retirement introduces.

A portfolio can look large on paper and still be fragile if it depends on aggressive withdrawals, poor tax sequencing, or heavy exposure to early volatility. On the other hand, a somewhat smaller portfolio may perform better in practice if the withdrawal structure is disciplined, the asset mix is appropriate, and the income sources are layered intelligently.

That is one reason later-life investing decisions deserve cluster-level treatment in the system. Retirement is not only about account value. It is about portfolio behavior under pressure: pressure from market declines, inflation, healthcare expenses, longer life expectancy, and the uncertainty of not knowing exactly how many years the money must support.

This cluster is where those pressure points get organized into a coherent framework so the investor is not forced to improvise later.

Sequence of Returns Risk Changes Everything

One of the most important concepts in retirement investing is sequence of returns risk. This refers to the order in which gains and losses happen. Two portfolios can have the same average return over time and still produce very different outcomes depending on when the negative years occur.

During accumulation, a bad early sequence is often survivable because continued contributions help average down the cost basis and restore growth. During retirement, the opposite can happen. If the portfolio suffers losses early while withdrawals are being taken, the investor may be forced to sell assets at lower values, leaving fewer assets in place for the eventual recovery.

This creates one of the defining structural challenges of retirement: the investor cannot think only in averages. They have to think in pathways. A strategy that looks fine in a spreadsheet using average returns may behave very differently when the first three years of retirement are weak instead of strong.

That is why retirement investing needs buffer thinking, reserve planning, and withdrawal flexibility. It is not enough to say the portfolio should grow over time. The investor needs to know how the system responds when the first part of retirement is rough instead of smooth.

Retirement is where portfolio structure matters more than portfolio hype.

See how later-life investing connects back to the full PersonalOne investing framework.

Explore the Investing & Wealth Growth System →Withdrawal Strategy Is the Centerpiece of the Cluster

If retirement investing has a single control point, it is withdrawal strategy. Asset allocation matters. Tax location matters. Social Security timing matters. But the practical day-to-day reality of later-life investing usually comes down to this: how money is taken out, from where, in what order, and under what conditions.

A withdrawal strategy is not just a percentage rule. It is a behavioral and structural framework. It determines how much flexibility the retiree has when markets are down, whether income is drawn from taxable or tax-advantaged accounts first, how much cash reserve is held to avoid forced selling, and what adjustments are made when inflation or spending needs change.

This cluster will eventually expand around that idea. The support articles that belong here should not simply repeat generic retirement advice. They should answer later-life decision questions: how to invest after retiring, how to structure income withdrawals, how much market exposure still makes sense, how to protect against early retirement volatility, how to blend growth and preservation, and how to decide whether the current withdrawal pattern is still sustainable.

That is why this cluster is not broad lifestyle content. It is a specific portfolio-and-income decision cluster inside the Investing authority hub.

Retirement Portfolios Still Need Growth — But Growth Has a New Job

A common mistake in later-life investing is assuming retirement means abandoning growth completely. That feels safe, but it can quietly create a different kind of risk: purchasing power decay. Inflation does not stop because retirement starts. If the portfolio becomes too conservative too early, the investor may avoid short-term discomfort only to discover that the long-term spending power of the portfolio is weakening.

This is why retirement investing is a balancing act rather than a simple shift into “safe assets.” Growth still matters. But its job changes. During accumulation, growth is the main driver of wealth expansion. During retirement, growth becomes a support mechanism that helps the portfolio keep pace with inflation, support longer lifespans, and reduce the probability that the investor outlives the assets.

The cluster therefore has to talk about risk in two directions. Too much volatility can damage the portfolio during withdrawals. Too little growth can damage the portfolio over a longer horizon. Good retirement investing lives between those two extremes.

This Cluster Is About Decisions, Not Just Products

Another reason this cluster matters is that later-life investing decisions are rarely solved by choosing a single product. A new fund, annuity, bond ladder, or cash reserve structure may help in specific cases, but the deeper issue is decision architecture. What matters most is how the components work together.

This cluster is therefore built around decision categories:

Income timing. When does cash need to show up, and how predictable must that flow be?

Withdrawal sequencing. Which accounts are drawn from first, and how does that affect taxes and long-term sustainability?

Volatility management. How much fluctuation can the retiree realistically tolerate without abandoning the plan?

Longevity planning. How does the system behave if retirement lasts far longer than expected?

Behavior under stress. What protects the investor from making destructive decisions during difficult market periods?

That framing is what keeps the cluster strategic instead of turning it into a grab bag of disconnected retirement topics.

How This Cluster Fits Into the PersonalOne Money System

Inside the PersonalOne framework, this cluster belongs late in the sequence. It assumes the investor has already learned the fundamentals, used retirement accounts well, built a portfolio, and developed the discipline to hold through long-term cycles. Without those earlier pieces, later-life investing decisions become speculative because the foundation was never fully established.

That is also why this cluster should not be folded into a vague “life stage investing” category. It is not general life-stage content. It is the later-life end of the investing system — where the portfolio transitions from an accumulation machine to a distribution system.

In that sense, this cluster acts almost like a threshold. It marks the point where the investor is no longer asking how to build wealth from scratch. They are asking how to use wealth intelligently for the rest of life.

Explore the Investing & Wealth Growth Clusters

Investment Fundamentals — Learn the base rules of investing before portfolio decisions get more complex

Retirement Account Strategy — Build the account infrastructure that powers long-term retirement readiness

Index Fund Investing — Learn the core portfolio tools many investors use during the accumulation years

Portfolio Design & Discipline — Understand how allocation, behavior, and emotional control shape long-term outcomes

You are here: Investing in Retirement & Later-Life Wealth Decisions — Shift from growth-first investing to income, durability, and sustainability

Resources

Social Security Administration — Retirement Benefits

Investor.gov — Investor Education

SEC — Investor Education and Retirement Planning Resources

This cluster is part of the Investing & Wealth Growth system on PersonalOne — a full framework that connects beginner investing, account strategy, portfolio design, and later-life wealth decisions.

Continue Learning — Investing in Retirement & Later-Life Wealth Decisions

How Should I Invest Savings After Retiring? — The first support article in this cluster, focused on how to reposition investments once retirement begins

Retirement Accounts Explained — Revisit the account layer that feeds into later-life withdrawal decisions

Investment Psychology — Understand the emotional mistakes that become especially costly when withdrawals begin

Frequently Asked Questions

Why is retirement investing different from regular investing?

Because the job of the portfolio changes. During working years, the portfolio is mainly there to grow. During retirement, it must help fund life while still lasting long enough to support future spending. That means withdrawal design, volatility management, and sustainability become central issues.

What is the biggest risk in retirement investing?

One of the biggest risks is sequence of returns risk — early market losses combined with withdrawals. If the portfolio is forced to distribute cash while values are down, recovery becomes much harder because fewer assets remain invested when markets rebound.

Should retirees stop investing for growth?

Not completely. Retirement portfolios still need some growth to help offset inflation and support longer time horizons. The difference is that growth must be balanced against stability, withdrawal needs, and the retiree’s ability to tolerate volatility without abandoning the plan.

Why is withdrawal strategy more important than people think?

Because taking money out is not a neutral act. The timing, size, and source of withdrawals affect taxes, long-term sustainability, and portfolio durability. A poorly structured withdrawal pattern can do more damage than a moderately imperfect asset allocation.

Is this cluster only for people who are already retired?

No. It is also relevant for people approaching retirement who need to understand how the investing system changes before withdrawals start. The earlier that transition is understood, the easier it is to build a portfolio that can support both later-life spending and long-term stability.

PersonalOne Money System

This content is researched, written, and owned by PersonalOne — a free financial education platform built to help Millennials and Gen Z build real financial systems that can grow, adapt, and support later-life decisions.

Disclaimer: This content is for educational purposes only and does not constitute financial, tax, legal, or retirement-planning advice. Individual financial situations vary — consult a qualified professional for guidance specific to your situation.