November 15, 2024

Updated: May 17, 2026

Home › Banking Systems › The 3-Account System Explained › How Much Money Should You Keep in a Money Market Account

Part of the 3-Account System Explained cluster — the complete framework for structuring your banking so every dollar has a job.

Don Briscoe is a financial systems strategist with 12+ years of experience helping Millennials and Gen Z build income and financial stability. He founded PersonalOne to provide the financial education he wished existed — structured, honest, and free.

What You Need to Know

— Emergency fund baseline: Keep 3–6 months of essential expenses in your money market account.

— Short-term goals: Add savings for any goals you will reach within 1–3 years — vacation, down payment, car replacement.

— Safety plus liquidity: MMAs are FDIC-insured up to $250,000 and accessible within 24 hours.

— Do not overdo it: Money market accounts earn less than investments — keep only what you need for near-term access.

— The right balance: Every dollar in your MMA should serve a specific, near-term purpose. Everything else belongs in investments.

What is the right amount of money to keep in a money market account? The honest answer: it depends entirely on what role the account is playing in your financial system — and whether you have defined that role at all. If you are operating a structured 3 account banking system — with separate accounts for spending, bills, and savings — your MMA fits into the savings slot of that structure, and the formula below will tell you exactly how much it should hold.

A money market account (MMA) bridges the gap between traditional savings accounts and investment accounts. It offers better interest rates than standard savings while keeping funds accessible — making it well-suited for money with a near-term purpose. The problem most people run into is not finding a good MMA. It is not knowing how much should live there versus somewhere else. For the complete architecture showing how a money market account connects to checking and bills inside a structured banking system for money management, the Banking Systems hub covers the full setup.

Before sizing your MMA, it helps to understand how it compares to the alternative. A high-yield savings account typically offers higher APYs with lower minimums — the full breakdown of when each wins is in the savings vs money market account comparison. If a HYSA is the better fit for your goals, the high interest savings account options guide covers the top picks side by side. If an MMA is the right call, the framework below tells you exactly how much to put in it.

The Three-Part Money Market Formula

Think of your MMA balance as three potential layers stacked on top of each other. Not everyone needs all three, but understanding each one helps you land on a number that is defensible rather than arbitrary.

Layer 1 — Emergency Fund (Primary Purpose)

Your emergency fund is the non-negotiable foundation. It should cover three to six months of essential living expenses — rent or mortgage, groceries, utilities, insurance, minimum debt payments, and transportation. Nothing discretionary counts here: this is the number that keeps your life running if income stops.

A money market account is a strong home for an emergency fund because it provides FDIC insurance (up to $250,000), competitive interest rates that beat standard savings, and access to funds within 24 hours if needed — without the temptation of daily spending access that a checking account creates.

How to Calculate Your Emergency Fund Target

Add up your monthly essential expenses. Multiply by the number of months appropriate for your situation:

3 months: Dual income household, stable employment, minimal dependents

4–5 months: Single income, moderate job stability, or one dependent

6 months: Freelancer, single income, volatile industry, or multiple dependents

Example: $3,500/month in essential expenses × 4 months = $14,000 emergency fund target.

For more detail on how to calculate the right emergency fund size — including the factors that push your number higher or lower — the cash reserve savings plan guide covers the complete strategy, including how to sequence building it and where to keep it at each stage.

Layer 2 — Short-Term Goals (1–3 Year Timeline)

Money you will need within three years should not be invested in the market — too much risk of being down exactly when you need it. An MMA provides meaningful growth (4%+ APY in 2026) without exposing near-term goal money to volatility.

Common short-term goals that belong in an MMA: home down payment, car replacement, wedding, vacation fund, or a large planned purchase. Calculate the total cost, determine your timeline in months, and divide to get your monthly savings contribution target. The interest you earn accelerates the timeline.

Example: Saving $12,000 for a home repair reserve over 18 months requires $667/month in contributions. At 4.50% APY, interest earned over that period adds roughly $400 — effectively giving you one free month of contributions.

Layer 3 — Variable Expense Buffer (Optional)

An optional third layer: a buffer for unexpected but non-emergency expenses — car repairs, medical costs not covered by insurance, or home maintenance surprises. Keeping an extra 10–20% above your core emergency fund prevents small surprises from requiring you to draw down the emergency fund proper. If your emergency fund target is $15,000, a $1,500–3,000 buffer on top of it provides coverage without putting the full fund at risk.

How Much Is Too Much?

This is the question most people do not think to ask — but it matters. Money market accounts offer safety and liquidity, but they are not optimal for long-term growth. Keeping excess cash in an MMA when it should be invested is a form of financial friction that costs real money over time.

In 2026, a top MMA earns approximately 4.00–4.25% APY. That is competitive for near-term money. But over a 20-year horizon, diversified stock index fund investments have historically averaged 7–10% annually — significantly more. Every dollar sitting in an MMA beyond its intended purpose is a dollar not compounding at investment-grade returns.

The Rule: Purpose Before Balance

Keep only what you need for emergencies and short-term goals (1–3 year timeline) in your MMA. Every dollar beyond that should be working harder in a retirement account, brokerage account, or other investment vehicle matched to your timeline and risk tolerance. If you cannot name a specific purpose for a portion of your MMA balance, that money probably belongs somewhere else.

The inflation math reinforces this: if your MMA earns 4% but inflation runs at 3%, your real return is 1%. On $50,000 held in an MMA that should be invested, the opportunity cost over 10 years is substantial. Safety is appropriate for near-term money. It is a liability for long-term money.

What a Fully Funded MMA Looks Like in Practice

Here is how the three-layer framework translates to a real balance for two different financial situations:

| Layer | Single Renter, Stable Job | Homeowner, One Income |

|---|---|---|

| Monthly essentials | $2,800 | $4,200 |

| Emergency fund (x months) | $8,400 (3 months) | $25,200 (6 months) |

| Short-term goal savings | $6,000 (vacation + car fund) | $15,000 (home repair + car) |

| Variable expense buffer (15%) | $1,260 | $3,780 |

| Total MMA target | ~$15,660 | ~$43,980 |

These numbers illustrate why a single rule like “keep $10,000 in savings” fails most people — the right number varies dramatically based on income, expenses, housing situation, job stability, and what goals are on the horizon. The framework gives you a number grounded in your actual life, not someone else’s average.

Four Strategies to Build Your MMA Balance Faster

Automate Contributions on Payday

Set up an automatic transfer from your checking account to your MMA on the same day your paycheck hits. This removes the decision entirely — money moves before you can spend it. Even $100/month automated over 12 months is $1,200 plus interest. The consistency compounds over time; the manual intention does not.

Shop for the Best Rate Annually

MMA rates vary dramatically between institutions and change as the Fed moves rates. Top online banks offer APYs above 4% while traditional banks still pay under 1%. Moving $20,000 from a 0.5% account to a 4.5% account generates $800 in additional interest annually — for doing nothing other than switching. Review your rate once a year and move if you are more than 0.50% below the top available rate.

Route Windfalls Directly to MMA

Tax refunds, work bonuses, cash gifts, or any unexpected income should go directly into your MMA before hitting your checking account. Money that lands in checking tends to be absorbed by spending within weeks. Money that goes directly to MMA accumulates toward its purpose. Create a standing rule: windfalls go to MMA first, then you decide how to allocate them — rather than spending first and saving what is left.

Assign Every Dollar a Purpose

Unnamed savings gets spent. If your MMA holds $18,000 but you have not defined what each portion is for, you are managing a number instead of a system. Label your layers: $10,000 = emergency fund, $5,000 = down payment savings, $3,000 = car replacement. When a withdrawal happens, you know exactly which layer it draws from — and exactly what needs to be rebuilt.

Why MMA Accounts Work Better Inside a System

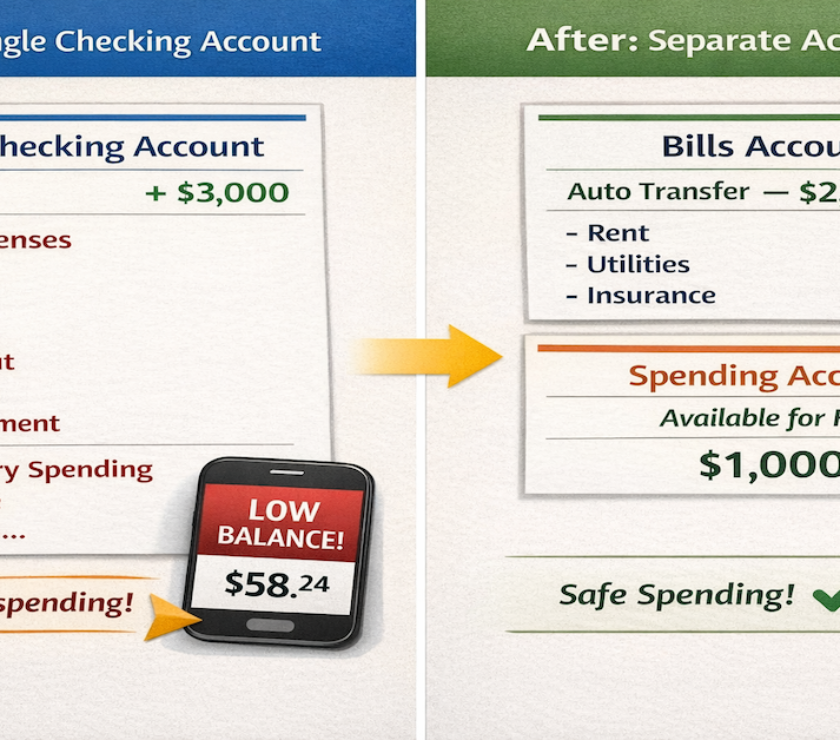

A money market account sitting in isolation is a savings account with a better interest rate. That is useful, but it does not prevent the main failure mode: treating savings as a backup spending account rather than a protected financial resource.

The reason MMA balances erode for most people is not that they chose the wrong account — it is that they never built the structural separation between spending money and savings money. When checking and savings live at the same institution with instant transfer capability, the behavioral friction between spending and saving disappears. Savings becomes a reserve tank that quietly drains toward discretionary spending labeled “emergencies.”

Keeping your MMA at a separate institution from your primary checking account solves this structurally. The 1–3 day transfer window creates enough friction to prevent impulse withdrawals while remaining fast enough for genuine emergencies. This is one of the core mechanics of a banking system that actually holds savings instead of just holding it temporarily.

Know Your Number. Then Build the System That Funds It.

Calculating the right MMA balance is step one. Step two is making sure money flows there automatically — from every paycheck, before spending decisions happen. The 3-Account System connects your checking account, your bills account, and your savings account so that your MMA target gets funded consistently, not accidentally. For the full architecture, see the banking system for money management guide.

Official Sources

FDIC — Deposit Insurance Coverage and Limits

Continue Building Your System

This article is part of the 3-Account System Explained cluster. The full cluster covers how to structure your checking, bills, and savings accounts into one automated system where money flows correctly every pay period without manual management.

Frequently Asked Questions

Should my MMA be at the same bank as my checking account?

Not necessarily, and often no. The best MMA rates are typically at online banks — institutions that specialize in savings products and pass their lower overhead to customers through higher APYs. If your checking account is at a traditional bank or credit union, keeping your MMA at a separate online bank for the rate advantage makes sense. The 1–3 day ACH transfer window between institutions provides protective friction against impulsive withdrawals while remaining fast enough for genuine emergencies.

Is a money market account or a high-yield savings account better for an emergency fund?

For most people, a high-yield savings account is the better fit. HYSAs typically offer higher APYs than MMAs (4.50–5.00% vs. 3.75–4.25% in 2026), have lower or no minimum balance requirements, and charge no monthly fees. The structural difference — no debit card access on an HYSA — also reinforces the savings discipline that an emergency fund requires. If you have decided a HYSA is the right call, the high yield savings account setup guide walks through the full process in under 10 minutes. MMAs become more competitive at higher balances where tiered rates kick in, or when you need direct payment capability for specific expenses.

How quickly can I access money from an MMA if I need it?

Most money market accounts offer two access paths: ACH transfer to linked checking (1–3 business days) and, for many MMAs, direct access via check or debit card. If your MMA includes check-writing or debit capabilities, emergency funds are accessible immediately. If it is a pure savings-style MMA, initiate the transfer the moment you know you need it — most true emergencies do not require cash in under 24 hours, making the transfer window manageable.

What if I am not at my MMA target yet — should I invest in the meantime?

Build the emergency fund first before directing money toward long-term investments. If you invest while your emergency fund is underfunded and an emergency hits, you may be forced to liquidate investments at an inopportune moment — potentially at a loss and with tax consequences. A 3–4 month emergency fund is the floor for beginning significant investment contributions. Once that is established, investment contributions and continued MMA growth can happen in parallel.

Can I use one MMA for both my emergency fund and short-term goals?

Yes — one account can hold both, as long as you track the allocation internally. The simplest approach is a spreadsheet or notes file labeling what each portion of the balance is earmarked for. Some online banks allow you to create labeled sub-savings “vaults” within a single account, which does this tracking automatically. The key is that the emergency fund portion is mentally off-limits except for genuine emergencies, regardless of whether it lives in the same account as your vacation fund.

This content is for educational purposes only and does not constitute financial or investment advice. PersonalOne is not a licensed financial advisor, broker, or investment professional. Money market account rates, terms, and FDIC insurance limits are subject to change. Individual financial situations vary significantly. Always verify current rates and terms directly with financial institutions before opening accounts.