February 6, 2026

Updated: June 3, 2026

Home › Credit Building & Protection › Credit Monitoring & Protection › How to Use Banking Tools to Rebuild Credit Faster

This article is part of the Credit Monitoring & Protection cluster on PersonalOne.

Don Briscoe is a financial systems strategist with 12+ years of experience helping Millennials and Gen Z build income and financial stability. He founded PersonalOne to provide the financial education he wished existed — structured, honest, and free.

What You Need to Know

— Banking tools directly support credit rebuilding when used strategically — secured cards, credit-builder loans, and checking account automation all feed into your recovery timeline.

— Credit monitoring completes the loop: banking tools generate activity; monitoring tools let you verify that activity is being reported correctly and catch improvements in real time.

— The fastest rebuilders structure their banking to create clean, consistent credit signals — and then watch those signals through monitoring to confirm progress.

— Free monitoring tools are sufficient for most rebuilders. The combination of the right banking setup and a free monitoring service is all most people need.

— Infrastructure beats willpower: automate payments at the bank level so positive credit signals happen without relying on memory.

Most credit rebuilding advice focuses on the credit side of the equation — dispute errors, pay down balances, wait it out. That advice is correct, but it misses half the picture. The banking tools to rebuild credit that are already sitting in your checking app, savings account, and credit card portal are some of the most powerful levers available — and most people never use them deliberately. Using them strategically, while keeping your progress visible through solid credit monitoring, turns a slow recovery into something you can actually track and control.

This article covers the specific banking tools that accelerate credit rebuilding, how they interact with your credit file, and how to connect them to a monitoring system so you can see results in real time — not six months later wondering if anything is working. Understanding how to increase your credit score quickly requires knowing both which credit actions move the needle and which banking structures make those actions automatic. That combination is what this guide is built around.

Why Banking and Credit Rebuilding Are the Same System

People treat banking and credit as separate topics, but they're deeply connected. Your bank account is where your financial behavior originates. Whether you pay on time, keep balances low, avoid overdrafts, and automate consistently — all of that starts in your banking infrastructure. Credit reporting is just the scoreboard. The game is played inside your bank.

When you understand that your bank is generating the raw material that feeds your credit file, the strategy becomes clearer: structure your banking to produce clean, consistent signals, then monitor those signals to make sure they're landing on your credit report correctly.

The three things your banking setup must do to support credit rebuilding are: eliminate the risk of late or missed payments through automation, create new positive tradelines through secured products and credit-builder tools, and keep utilization consistently low so reporting dates always show favorable ratios. The 3-account system is the structural framework that makes all three of those things happen automatically — separating spending money, bill payment, and savings into distinct accounts so each function operates cleanly without competing for the same balance.

The Banking Tools That Actually Move the Needle

Secured Credit Cards

A secured credit card is the most widely available and fastest-acting credit rebuilding tool in banking. You deposit a cash amount — typically $200 to $500 — which becomes your credit limit. The bank holds that deposit as collateral, but the card reports to all three credit bureaus exactly like a standard credit card. Every on-time payment builds payment history. Every statement with a low balance builds utilization history.

How to maximize a secured card: Use it for one or two recurring expenses — a monthly subscription, gas, or groceries. Set up autopay from your checking account for the full statement balance each month. Never let the balance sit above 10% of the limit when the statement closes. This strategy generates perfect payment history and optimal utilization at zero interest cost and minimal effort.

Graduation timelines: Most secured cards convert to unsecured cards after 12–18 months of positive behavior, returning your deposit and typically increasing your limit. This is a meaningful credit event — a limit increase without a new inquiry lowers your utilization ratio automatically.

What to look for: Choose secured cards that report to all three bureaus — Equifax, Experian, and TransUnion — charge no or low annual fees, and have a clear upgrade path to an unsecured product. Cards that don't report to all three bureaus are rebuilding your credit file at a fraction of the speed.

Credit-Builder Loans

Credit-builder loans are specifically designed for credit rebuilding and are offered by many credit unions, community banks, and online lenders. The structure is inverted from a traditional loan: the lender holds the loan amount in a savings account, and you make monthly payments over 12–24 months. Each payment is reported to the credit bureaus as an on-time installment loan payment. At the end of the term, you receive the accumulated funds.

Why they're valuable: Credit-builder loans add installment loan history to your credit file. If you only have credit cards right now, adding an installment account improves your credit mix, which contributes to 10% of your FICO score. More importantly, 12–24 months of perfect on-time installment payments is a powerful positive signal to lenders, particularly if your history includes past charge-offs or collections.

Cost consideration: Credit-builder loans charge interest, but the effective rate is often modest because you're receiving the principal back at the end. Think of it as paying for credit history. Loan amounts typically range from $300 to $1,500. A $500 credit-builder loan at a credit union with 12 monthly payments might cost $30–50 in total interest — a reasonable price for 12 months of positive installment history.

Autopay as a Credit Infrastructure Tool

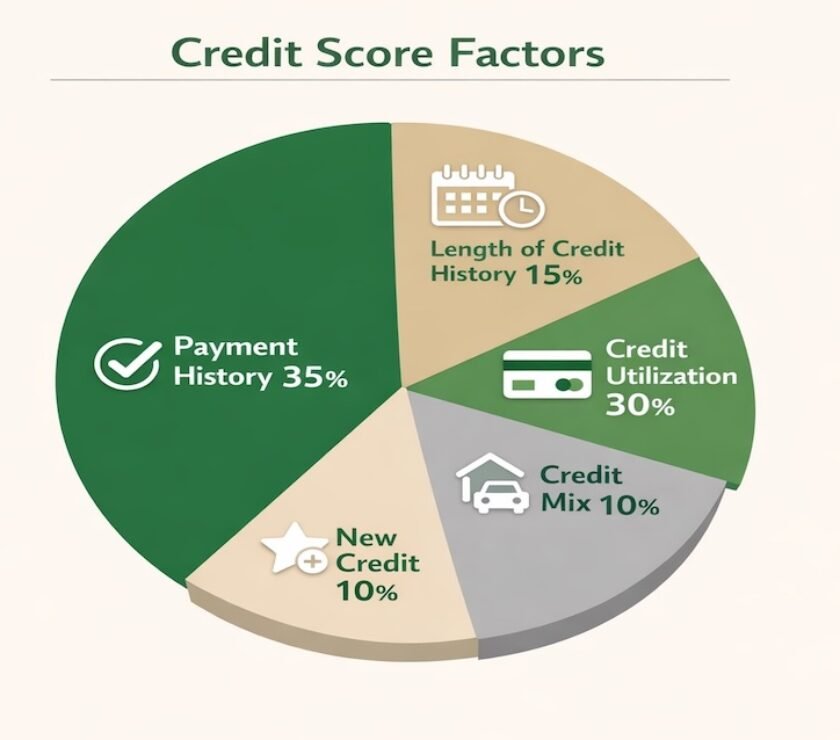

Autopay is not a convenience feature — it's credit infrastructure. Payment history is 35% of your credit score, and a single missed payment can drop a rebuilding score by 60–110 points. That wipes out months of progress in a single billing cycle. Setting up autopay for every credit account through your bank is the most reliable protection against that outcome.

The correct autopay setup during rebuilding: Set autopay for the statement balance — the full amount — not just the minimum. If paying the full balance strains your cash flow, set autopay for the minimum as a floor and then manually pay additional amounts throughout the month. This guarantees you never miss a payment regardless of what else is happening in your life.

Timing the autopay: Coordinate autopay dates with your pay schedule. If you get paid on the 1st and 15th, set payment due dates and autopay triggers that align with those deposits. Your bank's bill pay settings let you control exactly when payments leave your account. If payment dates are scattered, call each creditor and ask to move them to a single date each month — almost all will accommodate this. A dedicated bills system that helps prevent missed payments takes this further by structuring a separate account just for fixed obligations, so autopay pulls from a balance that is never competing with variable spending.

Experian Boost and Bank-Reported Payments

Experian Boost is a free tool that lets you connect your bank account directly to Experian and add rent, utility, streaming subscription, and phone payments to your Experian credit file. If you've been paying these on time for months or years, Boost can add positive payment history instantly. Users report average score increases of 10–20 points, with some seeing much higher gains when they have thin credit files.

The mechanism: Boost scans your bank transaction history for qualifying payments and lets you select which to add. It only adds positive history — any late payments in your bank history are not included. The boost applies only to your Experian score, not Equifax or TransUnion, so its impact depends on which bureau your lender uses. But for lenders who pull Experian — many major card issuers do — the improvement is real and immediate.

Who benefits most: People rebuilding from a thin credit file, recent immigrants, young adults just starting their credit journey, and anyone who has been paying rent and utilities on time but has limited traditional credit accounts. If you've been a reliable payer of everyday expenses, Boost lets you get credit for that behavior.

What I've Seen

The most consistent pattern across clients who stall during rebuilding is a mismatch between banking structure and credit strategy. They're doing the right things on the credit side — secured card, on-time payments — but the banking infrastructure is working against them. The checking account has no buffer, so autopay fails twice in twelve months and wipes out the streak. Or the secured card is being used for everything, so the balance is unpredictable and utilization spikes the month before they wanted to apply for a new account. The fix is almost never about the credit. It's about the bank account that's supposed to be funding it.

How Your Banking Structure Supports Credit Rebuilding

Beyond individual tools, the architecture of how you hold and move money affects your credit rebuilding speed. A well-structured personal banking system separates spending money from savings, automates outflows, and eliminates the decision-making friction that leads to missed payments and high utilization. When your banking infrastructure does the work automatically, your credit file improves as a side effect of good financial structure — not because you're constantly monitoring and manually managing every payment.

The Checking Account as Credit Command Center

Your primary checking account is where credit-rebuilding automation originates. All credit card autopayments, credit-builder loan payments, and utility payments flow out of it. Keeping a buffer in this account — typically one month of fixed expenses — ensures that autopay never fails due to an unexpected low balance. A failed autopay that results in a returned payment is not just a banking problem; if the creditor doesn't receive payment and reports it late, your credit file takes the hit.

Avoiding overdrafts: Overdrafts don't directly affect your credit score — unless the account goes into collections. But an overdraft that causes a bounced autopayment creates a chain reaction: the payment fails, the creditor charges a returned payment fee, and if the payment is then late by 30+ days, your score drops. Building a buffer eliminates this risk entirely.

Separating Spending from Credit Rebuilding Activity

During credit rebuilding, treat your secured credit card as a dedicated spending vehicle for a small number of fixed expenses — not as a general-purpose card for daily spending. When your secured card balance is predictable each month — same subscription, same gas, same utility — your utilization is predictable and controllable. Unpredictable spending creates unpredictable reporting balances, which creates unpredictable utilization — and high utilization in a single month can undo weeks of score progress.

High-Yield Savings as a Secured Card Deposit Source

Many people avoid opening secured cards because they don't want their deposit money sitting idle. Moving your secured card deposit to a bank that pays 4–5% APY on savings accounts — many online banks offer this as a standard rate — means the $300–500 you're holding as collateral is generating interest while it works. Over 12–18 months, that's a modest but meaningful offset to any annual fee. The deposit isn't locked up in the sense that you forfeit it; it's collateral that earns return while your credit rebuilds.

Connecting Banking Activity to Credit Monitoring

The most common mistake during credit rebuilding is doing the right things and then having no visibility into whether they're working. Banking tools generate credit activity. Monitoring tools verify that activity is being reported correctly, show you score changes as they happen, and alert you when something unexpected appears on your file. Without monitoring, you might spend 90 days on a strategy that isn't working — or miss a new collection account that appeared in month two.

Knowing how often you should check your credit report during active rebuilding is part of the system — it's not about obsessive score-watching, it's about timing your checks to the moments that matter, primarily right after your statement close dates when the new balances are freshly reported.

What to Monitor and When

Statement close dates: Your credit card company reports your balance to the bureaus on your statement closing date, not your payment due date. After you've made a mid-cycle payment to bring your balance down before the statement closes, check your monitoring app in the days following the closing date to confirm the lower balance was reported. This feedback loop — take action, confirm report — is how you know your utilization management is actually working.

New account reporting: When you open a secured card or credit-builder loan, it typically appears on your credit report within 30–60 days. Monitoring lets you confirm the account reported correctly, shows the right credit limit, and has the right payment status. Errors in new account reporting are more common than most people realize — monitoring catches them early while they're easiest to dispute. The process for how to dispute a credit report error with the bureaus is straightforward once you've identified the problem, but catching it early makes the resolution faster.

Payment history confirmation: Every time you make an on-time payment, it should eventually show as on-time on your credit report. Monitoring tools update score estimates monthly and often flag specific positive changes like "on-time payment streak increased." Seeing these updates confirms your autopay system is functioning and your payment history is accumulating correctly.

Alerts for new inquiries or accounts: Identity theft and unauthorized account openings are more common during periods when your credit is already damaged, because bad actors know monitoring is less likely. Credit monitoring alerts notify you immediately when a new inquiry or new account appears — giving you a chance to dispute it quickly before it ages into a harder-to-remove item. A thorough credit checkup and review of report errors at the start of your rebuilding process establishes your baseline and clears any inaccuracies that might be suppressing your score before you've even made your first new on-time payment.

Choosing the Right Monitoring Tool During Rebuilding

During active credit rebuilding, free monitoring tools provide everything most people need: score tracking, report updates, payment history summaries, utilization feedback, and alerts for new accounts or inquiries. You don't need daily monitoring or a paid service during the rebuilding phase. Checking your monitoring app once or twice a month — immediately after statement close dates — gives you the visibility you need without creating a habit of score-watching anxiety.

The question of free vs paid credit monitoring is worth understanding before you choose a tool — paid services add tri-bureau coverage and identity theft insurance that become more relevant once you've rebuilt a solid score and have more accounts worth protecting. For most people actively rebuilding, free tools are the right starting point. If you're specifically evaluating one of the most popular free options, the full breakdown of whether Credit Karma is worth using for credit monitoring covers the tradeoffs — including where its VantageScore data is reliable for tracking purposes and where it falls short of what a lender will actually see.

A Practical Timeline: Banking Tools to Score Progress

Here's a realistic timeline for someone starting credit rebuilding using the banking tools described above. These timelines assume no new negative marks. A single late payment resets progress significantly — which is exactly why autopay and a checking account buffer are the non-negotiable foundation.

Month 1: Infrastructure Setup

Open a secured credit card at a bank or credit union that reports to all three bureaus. Apply for a credit-builder loan at a credit union if available. Set up Experian Boost and link your bank account. Set up autopay — full statement balance — for every credit account. Choose a free credit monitoring tool and take a baseline score reading. Confirm your checking account has a one-month expense buffer to protect against failed autopayments.

Months 2–3: First Confirmed Progress

Your secured card and credit-builder loan appear on your credit report. Your monitoring tool shows the new accounts. Experian Boost adds alternative payment history. If utilization was previously high, any balances paid down in month one start showing lower on updated reports. First score movement is typically visible here — usually 10–30 points if you've addressed high utilization and have clean autopay running.

Months 4–6: Payment History Building

Consistent positive payment history starts accumulating at scale. Your secured card is showing three to five consecutive on-time payments. Your credit-builder loan is adding installment history. Monitoring shows payment streak updates. Score progress continues steadily, particularly if your file previously had thin positive history. Many rebuilders see 40–70 cumulative point improvement by month six.

Months 7–12: Momentum and Optimization

Older negative items are aging, losing scoring weight. Payment history is compounding positively. If you started with charge-offs or collections, their impact is diminishing while your positive history grows on the other side of the ledger. Many rebuilders are eligible for their first unsecured credit card by months nine to twelve. Consider requesting a credit limit increase on your secured card without spending more to further lower utilization. The monitoring tool remains your feedback mechanism throughout. For a focused 90-day version of this rebuild strategy, the guide on how to fix your credit in 90 days covers the three-action framework — dispute resolution, utilization reduction, and payment protection — in a compressed timeline format.

Month 12+: Infrastructure Payoff

Credit-builder loan completes and the savings funds are released. Secured card may convert to unsecured with limit increase. Score gains from the past year compound as the positive payment history length grows. At this stage, most rebuilders have seen 60–120 point improvements from their starting baseline, depending on the severity of starting credit damage and whether lingering collections or charge-offs remain on the file.

Build the Full Credit System

Banking tools get credit activity flowing. The Credit Building and Protection guide maps the complete system — score strategy, monitoring and protection, utilization tactics, authorized user strategy, and optimization for every financial decision you'll face.

Explore the Complete Credit GuideGovernment Resources

CFPB — What Is a Secured Credit Card? — Official guidance on how secured cards work and how to choose one.

CFPB — What Is a Credit-Builder Loan? — How credit-builder loans work and what to look for.

AnnualCreditReport.com — Free weekly credit reports from all three bureaus, authorized by federal law.

FDIC — Understanding Credit Scores — FDIC consumer resource on credit scoring and banking relationships.

Return to the full credit building and protection guide for a complete overview of every credit strategy covered on PersonalOne.

Frequently Asked Questions

How fast can banking tools actually improve a credit score?

The quickest improvements come from paying down high credit card balances, which can show up on your credit report within 30–60 days of the balance dropping. Experian Boost can add points immediately upon setup. Secured cards and credit-builder loans take one to two months to appear on your report, then generate steady improvement over 6–12 months. People starting from a damaged score with manageable past-due debt can realistically see 60–100+ point improvements over 12 months of consistent execution.

Does opening a secured card hurt your credit score at first?

Yes, briefly. Applying for a secured card triggers a hard inquiry, which typically reduces your score by two to five points. Opening the account also temporarily lowers your average account age. Both effects are short-lived — usually reversed within three to six months as on-time payments accumulate and the new credit limit lowers your overall utilization ratio. The temporary dip is a worthwhile trade for the 12–18 months of positive history that follows.

Can I use a regular checking account to build credit?

A standard checking account doesn't build credit directly — banking activity isn't reported to credit bureaus. However, your checking account is the infrastructure that enables credit-building: it's where autopayments originate, where secured card payments clear, and where credit-builder loan payments are funded. Some fintech accounts now offer debit-linked credit building features, but they vary widely in effectiveness. The most reliable path remains using your checking account to fund and automate credit products that do report to bureaus.

Should I use one secured card or multiple?

Start with one secured card and one credit-builder loan. Two tradelines with perfect history are more valuable than four tradelines with inconsistent management. Once you've demonstrated you can execute consistently for 6–12 months, adding a second secured card can accelerate progress by further diversifying your positive history and increasing your total available credit — which lowers utilization. Opening multiple accounts at once when rebuilding creates multiple hard inquiries and temporarily reduces your average account age — a disadvantageous combination when your score is already under pressure.

Does Experian Boost affect my score at all three bureaus?

No. Experian Boost only affects your Experian credit file and any score calculated from it. Your TransUnion and Equifax scores are unchanged. This matters because different lenders pull different bureaus — mortgage lenders typically pull all three, while many credit card issuers primarily use one. If your lender uses Experian, Boost is meaningful. If they use TransUnion or Equifax exclusively, the boost won't appear in their calculation. Check your monitoring tool to see which bureau score is being used for any specific application.

What's the difference between credit monitoring and credit protection?

Credit monitoring is the ongoing process of watching your score changes, report updates, and new account alerts. It tells you what's happening to your credit file in near real time. Credit protection is the set of defensive actions you take to prevent unauthorized access — credit freezes, fraud alerts, and identity theft response. During active rebuilding, monitoring is the higher priority: you need to confirm that positive activity is being reported correctly. Credit protection becomes more critical once you have a strong score worth defending.

This article is for educational purposes only and does not constitute financial, banking, or credit repair advice. Credit improvement timelines vary based on individual circumstances, credit history, and the specific products used. Tool availability and features may change — verify current terms directly with any financial institution before opening accounts. For personalized guidance, consult a qualified financial advisor or certified credit counselor.