December 4, 2024

December 26, 2025

PersonalOne Financial Team

⏱️ 8 min read

In today's economic landscape, millions of Americans find themselves trapped in a suffocating cycle of debt. PersonalOne understands that the journey to financial freedom can seem overwhelming, but hope is not lost. Debt relief and credit repair are two powerful strategies that can help you reclaim your financial health and peace of mind.

The Debt Dilemma: Understanding Your Options

According to recent financial studies, over 80% of Americans are carrying some form of debt. Navigating the complex world of debt relief requires knowledge, strategy, and the right approach. Whether you're struggling with credit card balances, medical bills, or personal loans, understanding your options is the first step toward financial recovery.

What is Debt Relief?

Debt relief is a comprehensive approach to reducing your overall debt burden. This strategy focuses on decreasing the actual amount you owe and making your payments more manageable. When exploring how to find debt relief, consider these primary methods:

- Debt Negotiation: Working directly with creditors to lower total debt amounts through professional mediation

- Debt Consolidation: Combining multiple debts into a single, more manageable payment with potentially lower interest rates

- Debt Settlement: Negotiating with creditors to pay less than the full amount owed in exchange for closing the account

Real-World Case Study: Sarah's Debt Transformation

Sarah, a 35-year-old marketing professional from Austin, Texas, was drowning in $45,000 of credit card debt accumulated from medical emergencies and living expenses. Her monthly minimum payments exceeded $1,200, leaving her unable to save or invest in her future.

By partnering with a debt relief specialist, Sarah achieved remarkable results:

- Reduced her total debt by 40% through strategic negotiation

- Consolidated her payments into one affordable monthly installment of $650

- Avoided bankruptcy and its long-term consequences

- Rebuilt her credit score from 520 to 680 within 18 months

"I thought I'd be paying off debt forever," Sarah shared. "The relief program gave me a roadmap and, more importantly, hope for a better financial future."

Credit Repair: A Complementary Strategy

While debt relief focuses on reducing what you owe, credit repair concentrates on improving your credit score and removing inaccuracies from your credit report. This distinction is crucial when determining which path aligns with your financial goals.

Credit repair strategies include:

- Challenging inaccurate credit report entries with the three major bureaus

- Negotiating the removal of negative marks through "pay-for-delete" agreements

- Developing a strategic credit rebuilding plan using secured cards and credit-builder loans

- Establishing positive payment history through timely bill payments

Choosing Between Debt Relief and Credit Repair

Understanding when to pursue each strategy is essential for achieving optimal financial results. Your individual circumstances will determine the best approach.

When to Choose Debt Relief

Consider debt relief programs when you're experiencing:

- Overwhelming debt exceeding 50% of your annual income

- Multiple missed payments or accounts in collections

- Risk of potential bankruptcy

- Inability to make minimum monthly payments

- High-interest debt preventing you from making progress

When to Prioritize Credit Repair

Credit repair may be your primary focus if you're dealing with:

- Minimal outstanding debt that's manageable with current income

- Errors or fraudulent accounts on your credit report

- Preparing for major financial decisions like buying a home or car

- A credit score that doesn't reflect your actual financial behavior

- Old negative marks that can potentially be removed

The PersonalOne Approach to Financial Recovery

At PersonalOne, we recognize that effective financial recovery rarely relies on a single strategy. We recommend a holistic approach that combines both debt relief and credit repair for maximum impact. For more detailed information, check out our comprehensive credit and debt relief guide.

- Assess Your Financial Situation: Conduct a comprehensive review of your debts, credit report, income, and expenses to understand your complete financial picture

- Create a Personalized Debt Reduction Plan: Develop a strategic approach tailored to your specific circumstances, timeline, and financial goals

- Implement Credit Repair Techniques: Simultaneously work on improving your credit profile while reducing debt obligations

- Monitor and Adjust Your Strategy: Regularly review progress and make necessary adjustments to stay on track toward financial freedom

This integrated methodology ensures you're not just reducing debt, but also building a foundation for long-term financial health and stability.

How to Find Debt Relief That Works for You

When searching for the right debt relief solution, consider these essential factors:

Research Reputable Providers: Look for organizations accredited by the American Fair Credit Council or the International Association of Professional Debt Arbitrators. Check reviews, ratings, and complaint histories with the Better Business Bureau.

Understand Fee Structures: Legitimate debt relief companies typically charge fees based on the amount of debt enrolled or the amount saved. Be wary of upfront fees before any services are rendered.

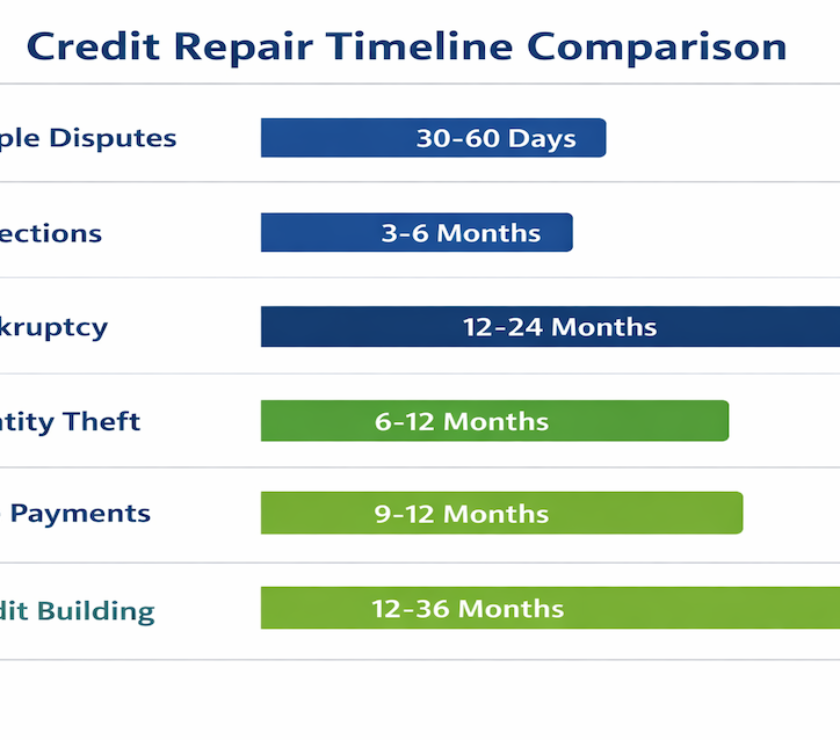

Evaluate Program Duration: Most debt relief programs take between two to four years to complete. Ensure the timeline aligns with your financial goals and capabilities.

Compare Multiple Options: Consult with several providers to understand different approaches, costs, and potential outcomes before committing to a program.

⚠️ Important Considerations

Both debt relief and credit repair can temporarily impact your credit score. During debt settlement negotiations, you may need to stop making payments to creditors, which will negatively affect your credit in the short term. However, the long-term benefits of becoming debt-free often outweigh these temporary setbacks.

Always remember to:

- Research thoroughly and verify credentials

- Work with reputable, transparent professionals

- Understand potential short-term credit implications

- Get all agreements in writing

- Avoid companies making unrealistic promises

The Long-Term Impact: Beyond Debt Freedom

Successfully navigating debt relief or credit repair extends far beyond the numbers on your credit report. The psychological relief of escaping financial stress can improve your overall quality of life, relationships, and mental health.

Studies show that individuals who successfully complete debt relief programs experience:

- Reduced stress and anxiety levels

- Improved sleep quality and physical health

- Better focus and productivity at work

- Stronger personal relationships

- Increased confidence in financial decision-making

Your Financial Freedom Starts Now!

Don't let debt control your life any longer. Take the first step toward financial recovery today with PersonalOne's expert guidance and proven strategies.

️ Schedule Your Free Consultation

Download "5 Secrets to Debt Freedom"

Share Your Story with Our Experts

Join thousands of Americans who have successfully transformed their financial lives through debt relief and strategic financial planning.

At PersonalOne, we believe everyone deserves a second chance at financial stability. Whether you're exploring how to find debt relief or considering credit repair options, our team of experienced financial professionals is here to guide you through every step of your journey.

Remember, the path to financial freedom begins with a single decision. Make today the day you choose to take control of your financial future with debt relief strategies that work.

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or professional advice. Individual results may vary based on specific circumstances. Always consult with a qualified financial advisor or debt relief professional before making significant financial decisions. PersonalOne recommends thoroughly researching any debt relief or credit repair program before enrollment.

References & Resources

- Federal Reserve Consumer Credit Report, 2024

- National Financial Educators Council - Debt Statistics

- Consumer Financial Protection Bureau - Debt Collection Guidelines

- American Fair Credit Council - Industry Standards

- Federal Trade Commission - Consumer Debt Information