September 2, 2024

Updated: February 18, 2026

Home › Financial Stability › Financial Shock Absorption › Financial Stress Relief: Build a 4-Layer Money System That Never Breaks

This article is part of the Financial Shock Absorption series — a collection of guides that cover building a money system that survives financial disruption.

About the Author

Don Briscoe is a financial systems coach with 12+ years helping Millennials and Gen Z escape paycheck-to-paycheck cycles. He’s worked with hundreds of people to build emergency funds, eliminate debt, and start investing using framework-first strategies that require less willpower and more infrastructure. He founded PersonalOne to provide the financial education he wished existed—structured, honest, and free.

TL;DR — Quick Takeaways

- Financial stress happens when you have no buffer layers — one unexpected expense spirals into debt, late payments, and panic.

- The 4-layer money system creates shock absorption — each layer catches different-sized financial hits so nothing cascades into crisis.

- Layer 1: Cash flow buffer ($500–1K) prevents timing issues between paychecks and bills.

- Layer 2: Expense buffer ($1K–2.5K) handles car repairs, medical bills, and surprise costs without credit cards.

- Layer 3: Income buffer (1–2 months) smooths income volatility for freelancers, commission workers, and seasonal earners.

- Layer 4: Emergency fund (3–6 months) protects against job loss, major life disruptions, and catastrophic events.

- Build sequentially from Layer 1 to Layer 4 — each layer strengthens the foundation for the next one.

Why Financial Stress Happens (And Why It Never Stops)

Financial stress doesn’t come from not making enough money. It comes from having no buffer between you and life’s inevitable disruptions. When your car needs a $600 repair and you have $47 in your checking account, that’s not a car problem—that’s a system problem. You’ve built a financial structure with no shock absorption.

Here’s what happens without buffers: One unexpected expense forces you onto a credit card at 24% APR. That payment crowds out next month’s groceries. You miss a utility payment. Your credit score drops. Insurance rates go up. The next emergency hits harder because you’re already wounded. This is the financial stress cascade—and it’s completely preventable.

The solution isn’t “make more money” or “cut your spending.” The solution is building a four-layer money system where each layer catches specific types of financial shocks before they escalate. When a $600 car repair hits, it gets absorbed by Layer 2, you pay cash, and you move on with your life. No stress. No debt. No cascade.

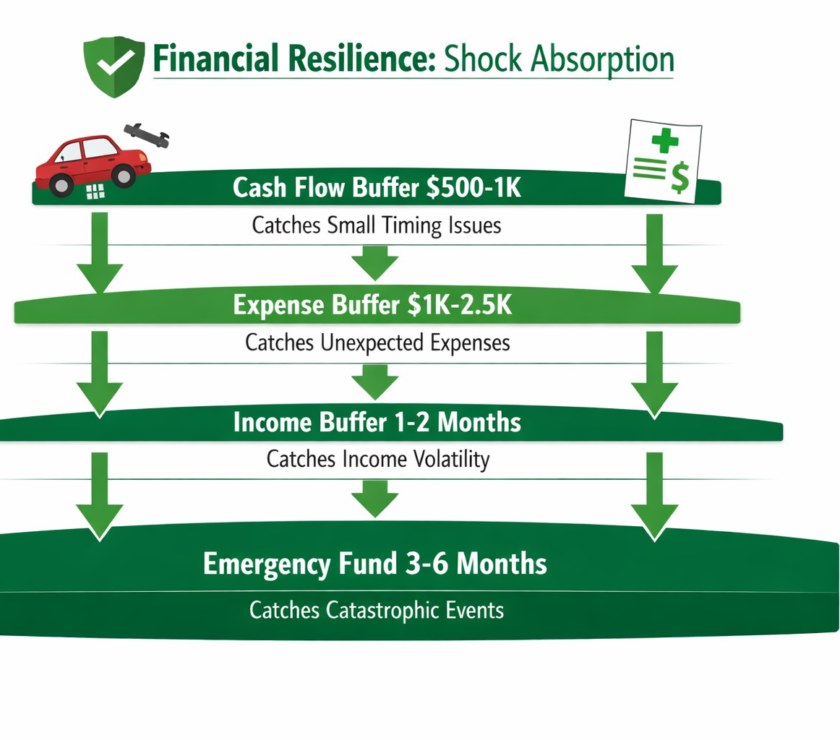

The 4-Layer Money System That Eliminates Financial Stress

Think of these layers like a car’s suspension system. Each component absorbs different impacts. Small bumps get handled by one layer. Medium jolts hit another. Big crashes activate the deepest protection. Nothing reaches your chassis—your long-term financial stability—until it overwhelms all four layers.

Layer 1: Cash Flow Buffer ($500–1,000)

Purpose: Handles timing mismatches between when bills are due and when you get paid.

What it catches: Rent due on the 1st but payday is the 5th. Grocery money runs out 3 days before payday.

Recovery time: Immediate (within same pay period)

Layer 2: Expense Buffer ($1,000–2,500)

Purpose: Covers unexpected but common expenses without triggering financial crisis.

What it catches: Car repairs, urgent medical bills, broken appliances, emergency vet visits.

Recovery time: 1–3 months to rebuild

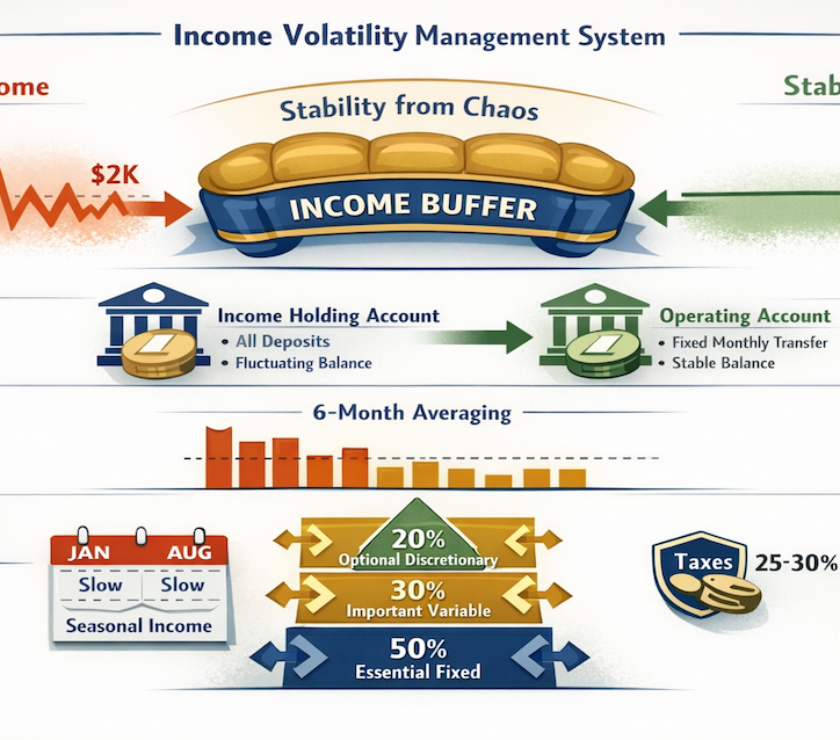

Layer 3: Income Buffer (1–2 months of expenses)

Purpose: Smooths income volatility for irregular earners.

What it catches: Slow freelance month, commission dry spell, seasonal business dips, bonus delays.

Recovery time: Ongoing (maintains consistent “paycheck” to yourself)

Layer 4: Emergency Fund (3–6 months of expenses)

Purpose: Protects against catastrophic life disruptions.

What it catches: Job loss, serious illness, family emergencies, major life transitions.

Recovery time: 6–24 months to rebuild fully

Critical principle: Each layer handles its own category of shock. When Layer 2 absorbs a $900 car repair, Layer 4 stays intact for real emergencies. This prevents cascade failure where small problems drain resources meant for big problems.

Layer 1: Build Your Cash Flow Buffer ($500–1,000)

This is your foundation. Without Layer 1, you’re living paycheck-to-paycheck even if you make $100K. The cash flow buffer eliminates the stress of bill due dates not aligning with payday.

How it works: Keep $500–1,000 in your checking account as a permanent cushion. This isn’t “spending money”—it’s infrastructure. Your bills hit on the 1st and 15th, but your paycheck comes on the 5th and 20th? The buffer handles the gap. You never overdraft. You never pay late fees. You never panic.

- Save $50–100 per paycheck until you hit $500, then continue to $1,000

- Use a “zero-based” starting point — once you reach your buffer amount, that becomes your new checking account $0

- Automate it — set up an automatic transfer from checking to a separate buffer sub-account the day you get paid

- Treat it as untouchable — this money is not available for discretionary spending, ever

Timeline: 3–6 months to build fully if saving $50–100 per paycheck. This layer eliminates 80% of paycheck-to-paycheck stress immediately once funded.

Layer 2: Build Your Expense Buffer ($1,000–2,500)

This layer handles life’s “expensive but expected” surprises. Cars break. Bodies need medical care. Appliances fail. These aren’t emergencies—they’re reality. Layer 2 keeps them from becoming financial catastrophes.

How it works: Keep $1,000–2,500 in a separate savings account—not your checking, not your emergency fund. When your car needs a $600 repair, you transfer $600 from this account, pay cash, and immediately start rebuilding it. No credit card debt. No payment plan. No stress.

Why $1,000–2,500? Data shows most unexpected household expenses fall in the $500–2,000 range. A fully-funded expense buffer of $2,500 covers roughly 95% of surprise costs without touching deeper layers.

- Start with $1,000 — this covers most car repairs, minor medical bills, and small emergencies

- Save $100–150 per month after Layer 1 is funded

- Keep it in a high-yield savings account — accessible within 1–2 business days but not instantly spendable

- Rebuild immediately after use — if you spend $800, pause all other savings goals until this layer is restored

Timeline: 6–12 months to build $1,000, another 10–15 months to reach $2,500. Most people stop at $1,500 and find that’s sufficient.

Layer 3: Build Your Income Buffer (1–2 Months of Expenses)

This layer is critical for anyone with irregular income. If you’re a freelancer, commission salesperson, seasonal worker, small business owner, or gig economy worker, Layer 3 eliminates income-based financial stress.

How it works: Build a separate account that holds 1–2 months of your expenses. All income lands here first. You pay yourself a consistent “salary” every month regardless of what you actually earned. Good month? Excess stays in the buffer. Bad month? The buffer supplements your income. Your monthly cash flow becomes predictable even when your income isn’t.

Who needs this:

- Freelancers and contractors with inconsistent client work

- Commission-based salespeople with variable monthly earnings

- Seasonal workers (construction, tourism, retail)

- Small business owners with uneven cash flow

- Gig economy workers (Uber, DoorDash, freelance platforms)

- Anyone who gets bonuses that make up more than 20% of annual income

- Calculate your monthly expenses — your “salary” should cover all fixed costs and essential variable spending

- Save aggressively during high-income months — if you make $8K in March but only pay yourself $4K, the other $4K builds your buffer

- Budget to your minimum income, not your average — use your lowest earning month from the past 6 months as your baseline

- Maintain the buffer forever — unlike Layers 1 and 2, this isn’t “use and rebuild”—it’s perpetual smoothing

Timeline: 6–12 months to build if you’re currently breaking even. Faster if you’re already profitable. This layer transforms irregular income stress into consistent cash flow confidence.

Layer 4: Build Your Emergency Fund (3–6 Months of Expenses)

This is your deepest protection. Layer 4 handles true catastrophes: job loss, serious illness, family emergencies, major life disruptions. Because Layers 1–3 handle smaller shocks, your emergency fund stays intact for actual emergencies.

How much you need:

- 3 months if you have stable W-2 income — predictable paycheck, good job security, low likelihood of sudden unemployment

- 4–5 months if you have moderate stability — contract work with renewals, commission but with base salary, seasonal but predictable

- 6+ months if you have high income volatility or risk — 100% freelance/self-employed, single income household, specialized field with limited job opportunities

- Only start after Layers 1–3 are funded — building a 6-month emergency fund while having no expense buffer is backwards

- Save 10–15% of income — if you make $5,000/month, that’s $500–750 per month to emergency fund

- Keep it in a high-yield savings account — separate from your other accounts, harder to access impulsively

- Define what qualifies as an emergency — job loss, medical emergency, family crisis. Not “the TV broke” or “I want a vacation.”

Timeline: 18–36 months for most people to build 3–6 months of expenses. This is slow by design—quick money is fragile money.

How to Build All 4 Layers Sequentially

Critical rule: Build from Layer 1 to Layer 4 in order. Don’t skip ahead. Each layer strengthens the foundation for the next one.

Month 1–6: Build Layer 1 (Cash Flow Buffer)

- Save $50–100 per paycheck until you reach $500–1,000

- Keep this in your checking account as a permanent cushion

- Track when you would have overdrafted without it—celebrate these wins

Month 7–18: Build Layer 2 (Expense Buffer)

- Save $100–150 per month in a separate savings account

- Target $1,000 first (achievable in 7–10 months)

- Continue to $1,500–2,500 if you own a car or home

- When you use it, pause all other savings until it’s restored

Month 19–30: Build Layer 3 (Income Buffer) — If Needed

- Skip this layer if you have W-2 income with consistent paychecks

- Build aggressively if you have irregular income—save 20–30% during high-earning months

- Target 1 month of expenses minimum, 2 months ideal

Month 31+: Build Layer 4 (Emergency Fund)

- Only start after Layers 1–3 are funded

- Save 10–15% of gross income consistently

- Target 3 months first, then decide if you need more based on your situation

- This takes 18–36 months for most people—that’s normal

Total timeline: 30–54 months to build a complete 4-layer system. Building financial resilience is slow, methodical work. But once built, it lasts forever and eliminates chronic financial stress completely.

Common Mistakes That Keep You Stressed

Mistake #1: Building Layer 4 before Layers 1–3

You save $5,000 for “emergencies” but have no cash flow buffer. Your checking account hits $0 before payday. You “borrow” from your emergency fund for groceries. Now your emergency fund is your checking account. This doesn’t work.

Mistake #2: Using your expense buffer for non-expenses

Your Layer 2 buffer is for unexpected costs, not “I want new shoes” or “let’s go out to dinner.” If you raid it for discretionary spending, it’s not a buffer—it’s just extra spending money. When the actual car repair comes, you’re back to stress and credit cards.

Mistake #3: Not rebuilding immediately after use

You use $800 from Layer 2 for a car repair. Great—that’s what it’s for. But then you continue saving toward Layer 4 while Layer 2 sits depleted at $200. Rebuild Layer 2 to full strength before resuming other savings. Otherwise the next expense hits exposed infrastructure.

Mistake #4: Keeping all layers in one account

You have $8,000 in savings. Technically you have a cash flow buffer, expense buffer, and partial emergency fund—but it’s all in one account marked “savings.” When you see $8,000, your brain says “I have $8,000.” You spend $3,000 on a vacation. Now you have $5,000 and no expense buffer. Separate accounts for each layer prevent this psychological trap.

What Financial Stress Relief Actually Feels Like

When you’ve built all four layers, here’s what changes:

- You stop checking your bank balance obsessively — your cash flow buffer means you’re never wondering if you can afford gas until Friday

- Unexpected expenses become logistics problems, not financial crises — “$700 car repair” becomes “Which day this week can I drop it off?” instead of “How do I come up with $700?”

- You can make career decisions based on fit, not desperation — your income buffer and emergency fund mean you can leave a toxic job, negotiate hard, or take a calculated risk

- Credit cards become convenience tools, not survival tools — you charge things for rewards or fraud protection, then pay in full, because your buffer layers handle cash flow gaps

- You sleep better — financial stress disrupts sleep, increases cortisol, and degrades decision-making. Buffers eliminate chronic money anxiety

This isn’t “being rich.” This is having a financial system that doesn’t break when life happens. That’s what stress relief actually means.

Start Building Your First Layer This Week

You don’t need to build all four layers at once. You need to start Layer 1 today.

- Open a separate savings account if you don’t have one — most banks let you do this online in 5 minutes

- Transfer $50–100 from your next paycheck into that account

- Label it “Cash Flow Buffer” in your banking app

- Repeat every paycheck until you hit $500

That’s it. That’s how you start eliminating financial stress. One layer at a time. One paycheck at a time. No gimmicks. No tips. Just a system that works.

Ready to Build Complete Financial Stability?

The 4-layer buffer system is the foundation of a complete financial stability strategy. Learn how emergency funds, shock absorption, and cash flow infrastructure work together as one system built to last.

Explore the financial stability system →Frequently Asked Questions

Can I build all four layers at the same time?

No. Spreading thin contributions across multiple layers means none of them reach full strength. You end up with $250 in Layer 1, $400 in Layer 2, and $600 in Layer 4—which means nothing is functional. Build sequentially. Fund Layer 1 completely, then move to Layer 2. This takes longer but actually works.

What if I have debt? Should I still build buffer layers?

Yes. Build Layer 1 first—even before aggressive debt payoff. Without Layer 1, every small timing issue forces you onto credit cards, creating new debt faster than you pay off old debt. Build $500–1,000 in Layer 1, then split your extra money between debt payoff and building Layer 2.

Do I need Layer 3 if I have W-2 income with consistent paychecks?

No. Layer 3 is specifically for income volatility. If your paycheck is the same amount every two weeks, skip Layer 3 entirely and go directly from Layer 2 to Layer 4. Layer 3 only matters for freelancers, commission workers, seasonal earners, and business owners with irregular income.

How do I know when to use each layer?

Use Layer 1: When the expense is regular but the timing is off — rent due before payday.

Use Layer 2: When it’s an unexpected but reasonable expense in the $500–2,000 range like car repair, urgent medical, broken appliance.

Use Layer 3: When your income is unusually low this month and you need to supplement your “salary” to yourself.

Use Layer 4: Only for true catastrophes — job loss, serious illness, or major life disruption.

What if I can only save $25 per paycheck?

That’s enough to start. $25 per paycheck is $50/month, which builds a $500 cash flow buffer in 10 months. Financial resilience isn’t about how fast you build—it’s about building systematically and not stopping. Someone saving $25/paycheck for 3 years ends up with stronger layers than someone saving $200/month for 6 months who then quits.

Where should I physically keep each layer?

Layer 1: Main checking account — it’s your new $0 balance

Layer 2: Separate savings account, same bank — transfer takes 1 day max

Layer 3: Separate “income holding” account, same bank

Layer 4: High-yield savings account, preferably at a different bank to reduce temptation

Resources & Further Reading

Official Sources

- CFPB — Building an Emergency Savings Fund

- Federal Reserve — Economic Well-Being Report: Unexpected Expenses

- FDIC Consumer News — Emergency Savings Strategies

More in This Series

This article is part of the Financial Shock Absorption series. Explore the other guides in this collection:

- Financial Resilience: Build a Money System That Survives Crisis

- How to Build an Emergency Fund That Actually Protects You

- How to Budget with Irregular Income (Freelance & Gig Work)

This series is part of the Financial Stability system › — the complete framework for building a money foundation that doesn’t break.

Disclaimer: The information provided on PersonalOne is for educational purposes only and does not constitute financial, legal, tax, or investment advice. PersonalOne and its content creators are not licensed financial advisors, attorneys, CPAs, or investment professionals. The frameworks, systems, and strategies presented here are general approaches to personal finance management and may not be suitable for every individual’s unique circumstances. Before making significant financial decisions, consult with qualified professionals such as a licensed financial advisor, CPA, or attorney who can assess your specific situation. Past performance and example scenarios do not guarantee future results. All financial strategies involve risk, and outcomes vary.