June 11, 2025

Published: March 6, 2026

Home › Credit Building & Protection › Credit Score Building Strategies › Buy Now Pay Later: Avoid the Traps and Protect Your Credit

About the Author

Don Briscoe is a financial systems coach with 12+ years helping Millennials and Gen Z escape paycheck-to-paycheck cycles. He has worked with hundreds of people to build emergency funds, eliminate debt, and start investing using framework-first strategies that require less willpower and more infrastructure. He founded PersonalOne to provide the financial education he wished existed -- structured, honest, and free.

TL;DR

Buy Now Pay Later has matured into a legitimate payment tool -- but it comes with real credit score consequences that most users do not read about before they click. Used intentionally for purchases you could already afford, BNPL costs you nothing extra. Used as a substitute for cash you do not have, it can create compounding payment obligations and credit damage that take months to undo. This guide covers how BNPL actually works, how it interacts with your credit file, and how to use it without letting it use you.

What Buy Now Pay Later Actually Is

Buy Now Pay Later is a short-term installment product that splits a purchase into a series of fixed payments -- typically four payments made every two weeks, though terms vary by provider and purchase size. Most standard BNPL plans charge zero interest if all payments are made on schedule. The provider pays the merchant upfront and collects from you over the payment period.

What distinguishes BNPL from a credit card is the structure. A credit card is an open revolving line -- you can carry a balance indefinitely and are charged interest on whatever remains unpaid after each billing cycle. BNPL is a closed installment product with a fixed repayment schedule tied to a specific purchase. Once the plan is paid off, it is closed. There is no revolving balance and no ongoing credit line to manage.

That structural difference is why BNPL appeals to people who are wary of credit card debt. The ceiling is defined at the moment of purchase. You know exactly what you owe, when each payment is due, and when the obligation ends. The problem is that this clarity can create false confidence -- and the consequences of missing payments are more significant than most users realize when they first sign up.

How BNPL Has Changed: Bureau Reporting Is Now the Norm

The most important shift in BNPL over the past few years is that major providers now report payment activity to the credit bureaus. This was not always the case. Early BNPL products operated largely outside the credit reporting system -- missed payments might trigger late fees and collection activity, but they did not directly affect your FICO score. That has changed.

Affirm reports to Experian for most of its loan products, and the account appears on your credit report similarly to a personal installment loan. Klarna began reporting to all three major bureaus for its financing products, though reporting practices vary by product type -- their pay-in-four plans may be handled differently than longer-term financing. PayPal Pay Later reports to credit bureaus for its longer-term monthly payment plans. Afterpay has historically not reported standard pay-in-four transactions to bureaus, though this may change as the regulatory environment tightens.

The practical implication is that you need to check the credit reporting policy of any BNPL service before you use it -- not after. If a provider reports to the bureaus, on-time payments can help your credit history, which is a genuine benefit. But missed payments will hurt your score just as a missed credit card payment would, and the late fees and potential collections activity compound that damage.

Understanding How BNPL Fits Your Credit Strategy

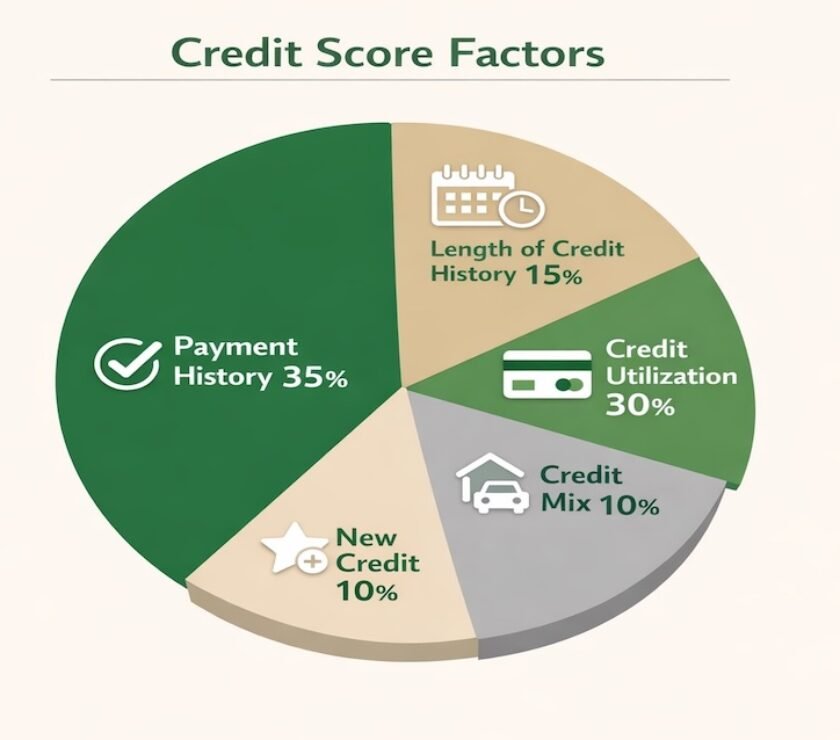

BNPL is one piece of a broader credit picture. For the full framework on managing payment history, utilization, and account mix across all your credit products, visit our Credit Score Building Strategies guide.

The Real Risks: What Goes Wrong and Why

The most common BNPL problem is not a misunderstanding of the product -- it is accumulation. Each individual BNPL plan looks manageable in isolation. A $200 purchase split into four $50 payments feels painless. The issue is that most people do not open one BNPL plan at a time. They open three or four across different retailers over the course of a few weeks, and suddenly have eight to sixteen payments due across multiple services on different biweekly schedules. Tracking those obligations without a system is genuinely difficult, and a missed payment on any of them triggers consequences.

Late fees on BNPL plans are typically capped -- often between $7 and $15 per missed payment, with a maximum per plan -- but they accumulate quickly across multiple open plans. More seriously, some providers escalate to collections after a certain number of missed payments, which creates a collections account on your credit report. A collections entry can drop a good score by 100 points or more and stays on your credit file for seven years.

Deferred interest promotions are a separate risk. Some BNPL products marketed as 0% financing actually use a deferred interest structure rather than a true zero-interest plan. In a deferred interest product, interest accrues on the full purchase amount throughout the promotional period but is waived if you pay the balance in full before the promotion ends. Miss that deadline -- even by a day -- and the full accumulated interest gets added to your balance at once. These offers can carry APRs of 25% to 30% or higher. Reading the distinction between "0% interest" and "0% APR if paid in full within promotional period" matters before you accept financing terms.

The psychological dimension of BNPL is also worth taking seriously. Installment framing reduces the perceived cost of a purchase. Research consistently shows that people spend more when paying in installments than when paying in full upfront -- the same cognitive pattern that makes subscription pricing so effective. A $400 item broken into four $100 payments feels like a $100 decision at checkout. The full $400 still leaves your accounts; the framing just delays the full impact of that reality.

The Regulatory Landscape: CFPB Oversight and What It Means for You

The Consumer Financial Protection Bureau has been actively examining BNPL's role in consumer lending. The CFPB's research found that BNPL users are more likely to carry revolving credit card balances, have higher overall debt loads, and experience more financial distress than non-BNPL users -- a pattern that suggests BNPL tends to supplement existing financial stress rather than replace higher-cost debt.

In response, the CFPB has moved to apply credit card-style consumer protections to BNPL products, including requirements for dispute resolution processes, refund handling, and clearer disclosure of terms. These protections bring BNPL closer to the regulatory framework that governs traditional credit products and give consumers clearer recourse when things go wrong.

The practical takeaway is that BNPL is no longer a regulatory gray area. If a BNPL provider is failing to honor a dispute or refund after a return, you have more formal recourse than you did several years ago. You can file a complaint with the CFPB directly at consumerfinance.gov. That said, regulatory protections do not prevent you from taking on more BNPL obligations than you can manage -- that protection has to come from your own system.

How to Use BNPL Without Letting It Damage Your Credit

The system for using BNPL responsibly is simple, but it requires committing to it before you open a plan rather than after something goes wrong.

The first rule is to only use BNPL for purchases you could pay for in full right now if you had to. BNPL should be a cash flow management tool, not access to money you do not have. If you cannot afford the full purchase price from your current budget, BNPL is not making it affordable -- it is financing a purchase you cannot afford, with late fees and credit consequences if anything disrupts your payment schedule.

The second rule is to limit yourself to one active BNPL plan at a time. Multiple simultaneous plans create the scheduling and tracking problem described above. One plan with a clear payment schedule is manageable. Four plans on four different biweekly cycles, across four different apps, is a system that will fail under any disruption to your cash flow.

The third rule is to automate every payment. Set up autopay for the full installment amount on every BNPL plan you open, using the same bank account you use for other automated bill payments. Manual payment tracking is the single most common failure point. Autopay eliminates it.

The fourth rule is to check the credit reporting policy before you use a new BNPL service. If the provider reports to the bureaus, treat that plan the same way you treat a credit card payment -- because a miss will have the same consequences. If the provider does not report, the credit downside is lower, but you also get no credit-building benefit from on-time payments.

Can BNPL Help Build Credit?

For providers that report to the bureaus, BNPL on-time payments can contribute positively to your payment history, which is the largest single factor in your FICO score. This is a genuine benefit, particularly for someone with a thin credit file who is actively trying to build history.

The limitation is that BNPL installment plans typically show up on your credit report as closed accounts once paid -- they do not maintain an ongoing open trade line the way a credit card does. The long-term contribution to your credit profile is therefore smaller than what a secured card or credit-builder loan produces, because those accounts stay open and continue generating positive payment history over time.

BNPL credit building also has a hard dependency on the provider actually reporting your on-time payments. Some providers report only negative activity -- missed payments get reported but on-time payments do not. That is the worst possible outcome from a credit perspective: you take on the risk of credit score damage without any of the potential benefit. Confirming what and how a provider reports before you open a plan is not optional if you are using BNPL with credit-building intent.

Build a Credit Strategy That Works With Your Spending Habits

BNPL is one tool in a broader credit system. The PersonalOne Credit Building & Protection guide covers how to manage payment history, utilization, and account mix across every type of credit product -- so your full credit picture works in your favor. Free, no signup required.

Framework-first. Less willpower. More infrastructure.

Frequently Asked Questions

Is BNPL better than using a credit card?

It depends on the purchase and how you manage credit. For a planned purchase you intend to pay off immediately, BNPL with a 0% installment plan has no interest cost, whereas a credit card charges interest on any balance you carry month to month. However, credit cards offer stronger consumer protections -- dispute rights, fraud coverage, and established chargeback processes -- that BNPL products are only beginning to match. For someone who pays their credit card in full every month, the credit card is generally the more flexible and better-protected option. For someone who tends to carry a balance, a no-interest BNPL plan for a specific purchase can be cheaper if managed carefully.

Does opening a BNPL plan hurt my credit score?

It may trigger a soft or hard credit inquiry depending on the provider and loan amount. Standard pay-in-four plans typically use a soft inquiry, which does not affect your score. Larger financing amounts -- six-month or twelve-month plans -- more often require a hard inquiry, which can temporarily reduce your score by 5 to 10 points. Check the provider's terms before applying for any BNPL financing above a standard pay-in-four plan.

What happens if I miss a BNPL payment?

At minimum, you will be charged a late fee -- typically $7 to $15, depending on the provider, with a cap per plan. If the provider reports to credit bureaus and the payment goes 30 days past due, the late payment will appear on your credit report and can drop your score significantly. Continued non-payment can result in the account being sent to collections, which creates a collections entry on your credit file that remains for seven years. If a payment is missed, contact the provider immediately -- most will work out a payment arrangement before escalating to collections if you reach out proactively.

How do I get a refund if I return something I bought with BNPL?

Returns with BNPL require coordinating both with the retailer and the BNPL provider. Most providers will pause your payment schedule once a return is initiated, but the timing varies. You generally need to return the item to the retailer first, then notify the BNPL provider with proof of return to get your installment plan adjusted or refunded. Do not stop making payments while waiting for the refund to process -- if you miss an installment while the return is pending, you may still incur a late fee. Follow up with both the retailer and the provider in writing so you have a record.

How many BNPL plans can I have open at once?

There is no universal limit -- providers set their own approval criteria independently of each other. The practical limit should be one at a time based on your ability to track and manage the payment schedule. Each plan is a fixed obligation that competes with your other financial commitments. If you currently have multiple open plans and are struggling to track payments, consolidate them onto a single payment date using whatever manual or automated method your providers support, and close each plan as it is paid off before opening a new one.

Resources

CFPB: Consumer Use of Buy Now, Pay Later (2025 Report) — The Consumer Financial Protection Bureau's full research report on BNPL usage patterns, debt correlations, and consumer risk.

Federal Reserve Bank of Richmond: BNPL Market Impact and Policy Considerations — Economic research on BNPL's systemic role in consumer credit and the regulatory response.

CFPB: Submit a Complaint — File a complaint against a BNPL provider for unresolved disputes, refund failures, or unfair practices.

Disclaimer: The content on PersonalOne.org is for informational and educational purposes only and does not constitute financial, legal, or credit advice. Buy Now Pay Later terms, credit reporting practices, and fee structures vary by provider and change over time. Always review the current terms of any BNPL service before opening a plan. PersonalOne is not a credit repair organization and does not offer credit repair services.