Updated: May 23, 2026

Home › Banking Systems › Bills Systems That Never Overdrafts

What You Need to Know

— Overdrafts are not a discipline problem. They are a design problem. When bill money and spending money share the same account, overdrafts are structurally inevitable.

— A dedicated bills account eliminates the collision. Bills money lives separately, runs on autopay, and never competes with discretionary spending.

— The system requires one-time setup — not ongoing willpower. Once the bills account is funded and autopay is configured, it runs without intervention every month.

— The exact amount your bills account needs can be calculated. Most people underestimate it because they forget irregular expenses — annual subscriptions, quarterly insurance, semi-annual fees.

— The support articles in this cluster cover every step of building this system: setup, calculation, timing, autopay audit, overdraft protection, and what to do when something breaks.

Most people who overdraft are not bad with money. They are bad at infrastructure. The money was there. It was just in the wrong place at the wrong time — rent and Netflix and a car insurance payment all pulling from the same account that also needed to cover groceries and gas and a dinner out on Friday. The collision was structural, not behavioral. And the fix is structural too.

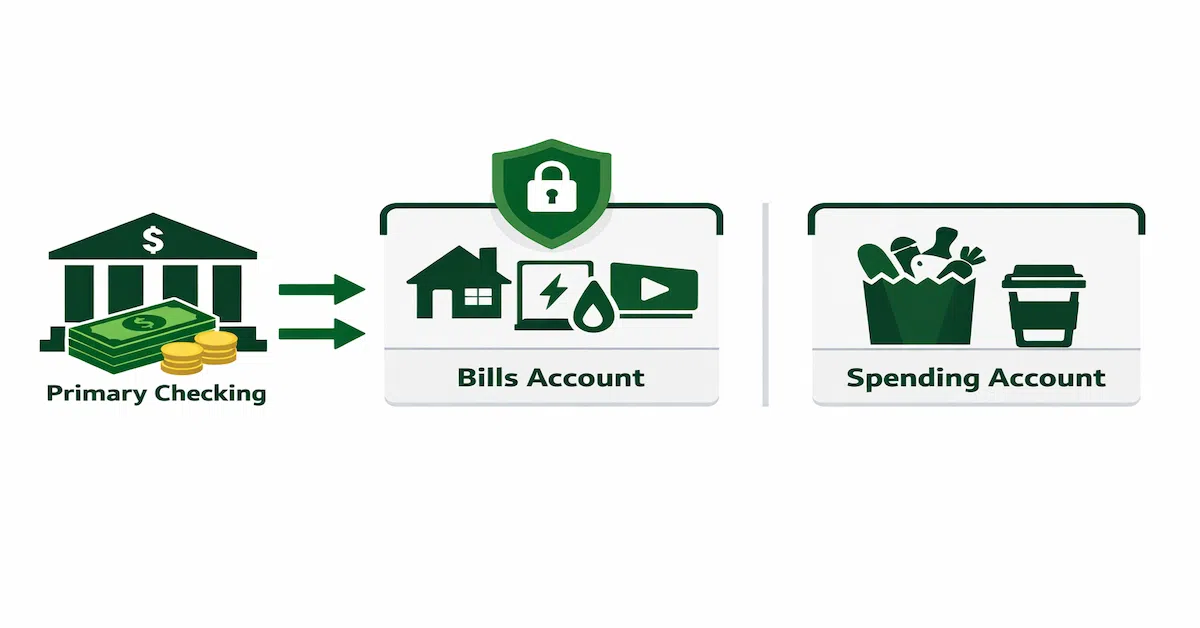

A bills system that prevents overdrafts works by separating the money that is already spoken for from the money available to spend. Bills go into a dedicated account that runs on autopay. Spending money lives in a separate checking account. The two pools never compete, so the collision that causes overdrafts cannot happen. The complete framework for how all your accounts connect — where the paycheck lands, how money flows between checking, bills, and savings — is in the banking systems account structure guide. This cluster goes deep on the bills layer specifically.

This cluster covers the complete build of an overdraft-proof bills account — from calculating the right amount to keep in it, to setting up autopay correctly, to protecting the system against timing gaps when a bill hits before your paycheck does.

Why Bills and Spending Money Cannot Share the Same Account

The standard checking account setup — one account, everything in it — creates a permanent tension between money that is committed and money that is available. Your rent is committed. Your car payment is committed. Your electricity bill is committed. But when they all live in the same account as your discretionary spending, nothing is visually separated, and every spending decision you make is implicitly a calculation against money that is already gone.

This is where most overdrafts originate. Not from reckless spending, but from a timing mismatch between when bills pull and when spending happens. You check your balance on a Tuesday and it looks fine. A car insurance payment hits Thursday. A utility autopay fires Friday. Your Friday grocery run puts you in the red. None of those individual decisions was wrong — the system design was wrong.

The structural fix: A dedicated bills account holds only money committed to recurring fixed expenses. It funds autopay and nothing else. Your spending account holds only discretionary money — the amount actually available after bills are covered. With those two pools separated, there is nothing to collide.

How the Bills System Works

The mechanics are simple. On payday, a portion of your income routes automatically to your bills account — exactly enough to cover every recurring fixed expense for the month, plus a small buffer for timing variation. Bills pull from this account via autopay. Your spending account receives the remainder — the actual discretionary money available after all committed expenses are covered.

The bills account does three things and nothing else. It receives the bills allocation from each paycheck. It pays bills via autopay. It maintains a small standing balance as a timing buffer. No debit card swipes. No discretionary transactions. No "borrowing from bills" to cover an unexpected expense. The containment is what makes the system work.

| Account | What Goes In | What Comes Out | Purpose |

|---|---|---|---|

| Bills Account | Fixed bills allocation from each paycheck | Rent, utilities, insurance, subscriptions — via autopay only | Contain committed expenses, eliminate overdraft risk |

| Spending Account | Remaining income after bills allocation | Groceries, gas, dining, discretionary purchases | Spend freely within available balance |

| Savings Account | Automatic transfer from spending account on payday | Emergency fund draws, planned withdrawals only | Build reserves, grow interest, stay untouched |

The Most Common Setup Mistakes

The bills system concept is straightforward. The implementation is where most people run into trouble — not because the system is hard, but because a few specific mistakes undermine it before it has a chance to work.

Underestimating the bills amount. The most common error. People calculate their monthly bills correctly for regular expenses but forget irregular ones — annual car registration, semi-annual insurance premiums, quarterly software subscriptions, holiday memberships. These hit and wipe out the buffer because they were never factored into the monthly allocation. The correct calculation accounts for every recurring expense across a full 12-month window, then divides the annual total by 12 to get the true monthly amount.

Not maintaining a standing buffer. A bills account with exactly the right amount — no more — has no room for timing variation. If a bill pulls two days before the paycheck allocation arrives, the account goes negative. A standing buffer of $200–$500, never touched, absorbs those timing gaps. The buffer is not spending money. It is infrastructure.

Using the bills account for non-bill spending. The containment only works if the account is never used for discretionary transactions. One debit card swipe from the bills account breaks the separation. Most people find that removing the debit card from their wallet — or using a bank that does not issue a card for secondary accounts — removes the temptation entirely.

Skipping the autopay audit. Bills accounts fail when autopay is not fully set up. If some bills still pull from the spending account, the separation is incomplete and the collision risk remains. A thorough autopay audit — reviewing three to six months of statements — catches every recurring charge before the system goes live.

What This Cluster Covers

Building an overdraft-proof bills system involves several distinct steps, each of which surfaces its own questions. The support articles below go deeper on each one — the calculation, the setup, the timing problems, and the ongoing maintenance that keeps the system running without friction.

How to Calculate Your True Monthly Bills (Including Irregular Expenses)

"I thought I knew what my bills were. Then the car registration hit."

The complete calculation for funding a bills account correctly — monthly fixed bills plus irregular annual and quarterly expenses, divided into a true monthly allocation. How to build the 12-month bills inventory, which expense categories most people miss, and how to fund the account from scratch without a paycheck gap.

How to Separate Your Bills From Spending So You Never Accidentally Overspend

"My balance looks fine — until three things hit on the same day."

The foundational account separation logic — why one account cannot serve both roles, how to open and configure a dedicated bills account, and how to route paycheck income correctly so the separation holds automatically from the first payday. The structural principle that makes everything else in this cluster work.

What to Do When All Your Bills Hit at the Same Time

"The first of the month wipes me out every single time."

The timing infrastructure solution for bills that cluster around the first of the month or around payday. How to spread bill due dates across the month, which bills can be rescheduled with one phone call, and how a bills account buffer absorbs the impact of clustered due dates without requiring any rescheduling at all.

How to Set Up a Dedicated Bills Account That Runs on Autopilot

"I want the bills to just handle themselves every month."

The step-by-step setup guide for a bills account that operates without monthly intervention — which type of account to use, how to configure autopay for every bill, how to set up the recurring transfer from the spending account, and how to verify the system is running correctly after the first full cycle.

Biweekly Pay vs Monthly Bills: How to Structure Your Accounts Correctly

"I get paid every two weeks but my bills are monthly. The timing never works."

The paycheck-to-bill alignment problem solved structurally. How biweekly income creates a mismatch with monthly bills, the allocation strategy that resolves it, and how to handle the two-paycheck months where extra income arrives. The specific routing logic that makes biweekly pay work seamlessly with a monthly bills system.

The Two-Week Buffer Strategy for Bill Stability

"What if a bill hits before my paycheck gets there?"

The timing cushion that makes an automated bills account completely resilient — how to build two weeks of bills coverage as a standing balance, why this buffer eliminates the paycheck timing problem permanently, and how to accumulate it without disrupting your current cash flow. The difference between a bills account that sometimes overdrafts and one that never does.

How to Audit Your Autopay Before It Costs You Money

"I know I'm paying for things I've forgotten about. I just don't know what."

The complete autopay audit process — how to surface every recurring charge across all accounts, which ones belong in the bills account versus the spending account, which ones to cancel, and how to migrate all surviving autopay to the bills account cleanly. The step that makes the bills system complete and the one most people skip.

What to Do When a Bill Hits Before Your Paycheck Does

"My electric bill always hits three days before I get paid. Every month."

The crisis prevention framework for timing gaps — the specific options when a bill is scheduled to pull before the next paycheck arrives, how to request due date changes from providers, when early direct deposit solves the problem, and how a properly funded bills buffer eliminates this stress permanently. The short-term fixes and the permanent structural solution.

The Bills System Is One Layer. The Full Framework Goes Deeper.

Separating bills from spending is the foundation of overdraft prevention. The broader system — how your paycheck lands, how savings grow automatically, how the entire structure stays funded without constant management — is in the PersonalOne banking systems account structure guide.

Frequently Asked Questions

How much should I keep in a bills account? The correct amount is your total monthly fixed bills — rent, utilities, insurance, subscriptions, loan payments — plus a buffer of $200–$500 that never gets spent. The most common mistake is calculating only the bills you pay every month and forgetting irregular ones: annual car registration, semi-annual insurance premiums, quarterly charges. The accurate number comes from a 12-month bills inventory, not just this month's statement.

Should my bills account be a checking account or savings account? A checking account works better for a bills account because it allows unlimited transactions, including autopay pulls. A savings account at many institutions limits withdrawals and may charge fees if autopay transactions exceed the monthly limit. Use a checking account with no monthly fees — online banks offer these with no minimum balance requirements. The bills account does not need to earn interest; its job is containment, not growth.

What if I can't fund a separate bills account right now? Start by tracking. Before the account is funded, spend one full month mapping every bill that pulls from your current account — the amount, the date, and whether it is fixed or variable. This inventory is the input for calculating the correct bills account balance. You can begin the system with a partial buffer and build toward the full amount over two to three pay cycles. A partially funded bills account still reduces overdraft risk compared to a single combined account.

What happens if a bill amount changes and my bills account comes up short? Variable bills — electricity in summer, heating in winter — are the main source of bills account shortfalls. Two approaches work: fund the bills account based on the highest expected monthly amount rather than the average, or maintain a larger standing buffer that absorbs the seasonal variation. The autopay audit article covers how to identify which bills are variable and how to account for their range in the monthly allocation.

Can I use this system if I have irregular income? Yes, with a modification. Variable income earners need a larger bills buffer — typically four to six weeks of bills coverage rather than two — to absorb the gap between paydays. The bills allocation percentage stays fixed; only the buffer size changes. The biweekly pay article covers the timing alignment in detail, and the same principles apply to freelance and irregular income with larger buffer targets.

Government & Official Sources

CFPB — Bank Account Tools and Overdraft Resources — Consumer guidance on overdraft coverage, your rights to opt out, and how to evaluate bank account terms.

FDIC — Deposit Insurance Coverage — Verify that any institution you use for your bills account is FDIC-insured before depositing.

Federal Reserve — Consumer Information on Bank Accounts — Federal Reserve guidance on checking accounts, overdraft fees, and deposit account rights.

Continue Learning

How to Calculate Your True Monthly Bills — Build the 12-month bills inventory and fund your bills account with the correct amount from day one.

How to Separate Your Bills From Spending — The foundational account separation that eliminates the overdraft collision structurally.

What to Do When All Your Bills Hit at the Same Time — The timing infrastructure solution for first-of-month bill clustering.

How to Set Up a Dedicated Bills Account That Runs on Autopilot — The step-by-step configuration guide for a bills account that operates without monthly intervention.

The Two-Week Buffer Strategy for Bill Stability — The timing cushion that makes the bills account completely resilient against paycheck gaps.

How to Audit Your Autopay Before It Costs You Money — Surface every recurring charge, decide what stays and what goes, and migrate everything to the bills account cleanly.

What to Do When a Bill Hits Before Your Paycheck Does — The short-term fixes and permanent structural solution for timing gap emergencies.

Your Bills Are Draining Your Accounts — Overdrafts are a structure problem, not a money problem. Here is permanent structural solutions.

PersonalOne Money System

This content is researched, written, and owned by PersonalOne — a free financial education platform built to help Millennials and Gen Z build real financial systems.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Account features, fees, and overdraft policies vary by institution and are subject to change. Always verify FDIC insurance status and review current account terms directly with the institution before opening an account. PersonalOne provides educational content and does not provide personalized financial planning services.