Updated: March 14, 2026

Home › FinTech & Modern Money Tools › Neobanks & Digital Banking Platforms

Neobanks & Digital Banking Platforms: What They Are, How They Work, and How to Use Them

PersonalOne Money System

This resource is part of the PersonalOne framework for building financial systems that run automatically — covering the tools, strategies, and infrastructure that replace willpower with structure. PersonalOne provides free financial education for Millennials and Gen Z.

Why the Best Neobanks and Digital Banking Platforms Changed What Banking Costs

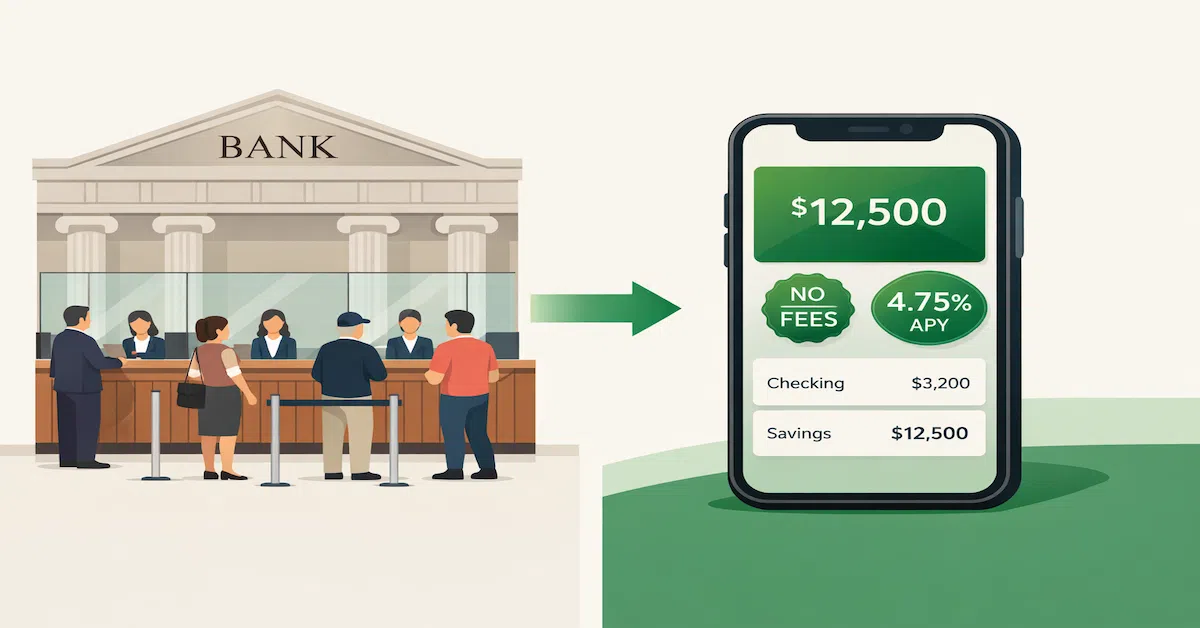

The best neobanks and digital banking platforms changed banking by removing the overhead that made traditional banking expensive and passing those savings directly to customers. No branches means no branch overhead. No tellers means no teller costs. No marble lobbies means no commercial real estate. The result is a category of financial platforms that can offer zero monthly fees, no minimum balances, early direct deposit, and savings rates that are orders of magnitude higher than traditional banking — not as promotional offers, but as standard product features sustained by a fundamentally lower cost structure.

The shift is not theoretical. Chime surpassed 20 million customers. SoFi became a chartered bank. Ally built one of the most recognized high-yield savings products in the country without a single physical branch. The competitive pressure these platforms created forced traditional banks to eliminate overdraft fees, improve mobile apps, and introduce high-yield savings products that did not exist at scale five years ago. Whether you use a neobank as your primary account or not, the existence of these platforms has already changed what you can demand from every financial institution you deal with.

This cluster covers the full neobank landscape: what digital banking platforms are and how they work, which platforms serve which financial needs, how to verify FDIC safety before depositing, and how neobanks fit into a complete banking architecture alongside traditional accounts.

What a Neobank Actually Is

A neobank is a financial technology company that delivers banking services entirely through software — no physical branches, no tellers, no in-person service. Most neobanks are not chartered banks themselves. They are technology platforms that partner with FDIC-insured banks to hold customer deposits, while the neobank provides the product layer: the app, the user experience, the features, and the customer relationship. The partner bank is the vault. The neobank is the interface.

This structure produces meaningful differences in what neobanks can offer. Without branch overhead, neobanks can sustain zero monthly fees and competitive savings rates as permanent product features rather than promotional offers. Without legacy systems to maintain, neobanks can push feature updates in weeks rather than years. Without the organizational inertia of a century-old institution, neobanks can build products specifically for how people manage money now — mobile-first, automated, and connected to the other apps in their financial lives.

The comparison that matters most for practical decision-making is not neobank vs traditional bank as abstract categories — it is which specific platform does which specific financial job best. The direct comparison of how digital banking platforms and traditional banks differ across fees, speed, lending, and mobile experience is covered in depth in the guide to traditional banking vs FinTech.

FDIC Coverage: The Only Question That Matters Before You Deposit

The single most important verification before opening any neobank account is confirming FDIC coverage. The question is not whether the app looks legitimate or whether the marketing is persuasive — it is whether your deposits are federally insured against bank failure.

FDIC coverage at neobanks works through the partner bank structure. When a neobank says "FDIC insured through [Bank Name]," your deposits are held at that chartered institution and insured up to $250,000 per depositor per bank — the same protection you have at Chase or Bank of America. The FDIC does not distinguish between digital and physical banks when paying out claims. The app going dark does not affect the underlying deposits at the partner bank.

The risk is not with established neobanks that clearly disclose their partner bank relationships. The risk is with payment apps and FinTech products that look like banking apps but are not FDIC-insured. Venmo balances, Cash App balances, and similar payment app balances are generally not FDIC-protected unless explicitly stated. Always verify at FDIC.gov before depositing significant funds in any digital financial platform — major neobanks and their current partner bank arrangements are searchable through the FDIC BankFind tool.

How Neobanks Make Money Without Monthly Fees

Understanding neobank business models is not just intellectually interesting — it tells you whether the platform’s incentives are aligned with yours or against you. Traditional banks make money when customers pay fees, carry credit card balances, and take out loans at high rates. The business model is built around products that cost the customer money.

Neobanks generate revenue through three primary mechanisms. Interchange fees on debit card transactions pay a small percentage of each purchase to the card issuer — typically 1–2% paid by the merchant, not the customer. This means every debit card swipe generates revenue for the neobank without costing you anything. Interest spread between what the neobank earns on deposits held at partner banks and what it pays you generates margin on the deposit base. Premium subscription tiers at many platforms offer additional features — higher savings rates, credit building tools, cash advance access — for a monthly fee that is always optional.

The alignment implication is significant: neobanks profit from your activity, not from charging you to exist as a customer. A platform that earns from your card usage has an incentive to make your card experience frictionless. A platform that earns from deposit spread has an incentive to make you want to keep more money there. These incentives generally favor the user in ways that traditional fee-based banking models do not.

Neobanks and Gen Z: Why This Generation Adopted Digital Banking Fastest

Gen Z’s adoption of neobanks and digital banking platforms is not primarily a technology preference story — it is a trust and alignment story. Gen Z entered financial life after the 2008 financial crisis and during a period of visible institutional failure. The generation that came of financial age watching traditional banks receive bailouts while customers lost homes has a different relationship with those institutions than previous generations.

Neobanks filled the gap not by being more technologically impressive, but by being more straightforward. Zero fees with no conditions. Savings rates disclosed clearly. No minimum balance requirements. No penalty structures for normal banking behavior. The transparency that neobanks built as a product feature — because they had to differentiate on something other than branch location — matched exactly what a skeptical generation needed to trust a financial platform. The behavioral patterns, mobile-first financial habits, and specific apps that define how Gen Z manages money are covered in the guide to why FinTech is winning Gen Z.

How Neobanks Fit Into a Complete Banking Architecture

The most common mistake with neobanks is treating the decision as binary: either stay with your traditional bank or switch entirely to a digital platform. The more productive framing is architectural. Every financial institution does some things better than others. Building a banking structure that assigns each account the jobs it does best produces better outcomes than forcing any single institution to do everything adequately.

The structure that works for most people assigns the daily operational layer to a neobank: the checking account where paycheck arrives and daily spending happens, the high-yield savings account earning 4–5% for emergency funds and short-term goals, the automated savings rules that move money between them without requiring weekly decisions. The lending and in-person layer stays with a traditional bank or credit union: the mortgage relationship, the auto loan, the cashier’s check, the notary service. The neobank handles the work that benefits from digital infrastructure. The traditional bank handles the work that requires physical infrastructure or established lending relationships.

Free Mobile Banking Apps: What to Look For

The free mobile banking app category has expanded significantly as neobank competition raised the minimum standard for what a zero-cost account delivers. Zero monthly fees is no longer a differentiator — it is a baseline expectation. The features that actually differentiate free mobile banking apps in 2026 are early direct deposit timing (how many days early), ATM network size and fee reimbursement policy, savings automation features built into the free tier, and the quality of real-time transaction alerts and fraud detection.

The evaluation criteria for free mobile banking apps, the specific platforms that rank highest on each feature dimension, and how to match platform capabilities to specific financial situations are covered in the guide to best free mobile banking apps.

ESG and Green Banking: Values-Aligned Digital Banking

A growing segment of digital banking platforms positions explicitly around environmental and social values — directing deposits toward green energy lending, refusing to fund fossil fuel projects, and publishing transparent impact reports on how customer deposits are deployed. For account holders who want their banking relationship to reflect their values alongside delivering competitive features and rates, this category offers alternatives to both traditional banks and mainstream neobanks.

The platforms in this category, how their impact claims hold up to scrutiny, and how to evaluate ESG banking options against mainstream alternatives on the dimensions that matter for everyday banking are covered in the guide to green banking and ESG-friendly banks.

Neobanks are one layer of a complete modern money system.

The complete framework for how digital banking platforms connect to payment tools, budgeting apps, open banking, and financial automation lives in the FinTech & Modern Money Tools guide.

Explore FinTech & Modern Money Tools →Resources

Official Sources

FDIC BankFind Suite — Search and verify FDIC insurance status for any neobank or its partner institution before depositing. The authoritative source for confirming deposit insurance coverage.

CFPB — Bank Accounts and Services — Consumer Financial Protection Bureau guidance on digital bank account rights, fee protections, dispute resolution, and how to file complaints against financial institutions.

Federal Reserve — Interest Rate Data — Benchmark interest rate data that directly influences neobank savings APYs and the spread between what digital banks pay and what they earn on deposits.

The Bigger Picture

Neobanks and digital banking platforms are one layer of a complete modern financial system. The full framework for how they connect to budgeting tools, payment infrastructure, and financial automation lives in the FinTech & Modern Money Tools guide.

Continue Learning: Neobanks & Digital Banking Platforms

Every article in this cluster covers a specific aspect of neobanks, digital banking platforms, and how they fit into a complete financial system.

Best Free Mobile Banking Apps: Which Ones Are Actually Worth Using

The free mobile banking apps that rank highest on early deposit timing, ATM network coverage, savings automation, and real-time fraud alerts — and how to match platform capabilities to your specific banking situation.

Why FinTech Banks Are Winning: The Smart Money Shift

Why millions of people moved money from traditional banks to digital platforms — and what the real advantages of neobanks are beyond zero fees.

How Gen Z Uses Banks, Apps, and FinTech (Complete Guide)

The four-layer Gen Z money stack, how neobanks fit into it, and why Gen Z adoption is reshaping product design across the entire financial services industry.

Digital-Only Banks Are Booming: Are Physical Branches Nearing Extinction?

Branch closure data, digital banking adoption rates, and what the structural shift means for consumers who still depend on in-person banking services.

Traditional Banking vs FinTech: A Complete Side-by-Side Comparison

How traditional banking and FinTech platforms differ in fees, speed, lending, mobile experience, and business model — and what those differences mean for your money in practice.

Why FinTech Is Winning Gen Z’s Wallets — And What That Means for Your Money

The behavioral patterns, mobile-first financial habits, and specific platforms that define how Gen Z manages money — and why neobank adoption rates are higher than any previous generation.

Green Banking and ESG-Friendly Banks: How to Align Your Money With Your Values

The digital banking platforms that direct deposits toward green energy and social impact — how their claims hold up to scrutiny and how to evaluate them against mainstream neobanks.

Top Digital Banking Trends in 2026 (What to Expect)

The eight structural changes reshaping digital banking in 2026 — from AI-powered financial management and real-time payment rails to regulatory tightening and open banking data rights — and what each means for your accounts.

Frequently Asked Questions

What is the difference between a neobank and a regular online bank?

A neobank is a technology company that delivers banking services through a partner bank — the neobank owns the app and the customer relationship, while a chartered bank holds the deposits. A regular online bank (like Ally or Marcus by Goldman Sachs) holds its own banking charter and is a bank in the full regulatory sense that happens to operate without branches. Both offer FDIC insurance, but neobanks are technology companies at their core while online banks are chartered financial institutions operating digitally.

Is my money safe in a neobank?

Yes, if the neobank is FDIC-insured or clearly discloses an FDIC-insured partner bank relationship. Look for "Member FDIC" or "FDIC-insured through [Bank Name]" on the neobank’s website and in the account agreement. If you see it, your deposits up to $250,000 are federally protected — identical coverage to any traditional bank. Verify the partner bank directly at FDIC.gov before depositing significant amounts.

Can I use a neobank as my only bank account?

Yes for most people — if you receive direct deposits, pay bills digitally, and rarely need to deposit physical cash. The main limitation is cash deposits: most neobanks do not accept them directly, though some partner with retail networks for cash deposit options at a small fee. If you regularly deposit cash from tips, gig work, or retail sales, maintain one traditional bank or credit union account alongside your neobank for that specific function.

What happens to my money if a neobank goes out of business?

If deposits are held at an FDIC-insured partner bank, your money is protected up to $250,000 regardless of what happens to the neobank’s app or company. The neobank shutting down does not affect the underlying deposits at the chartered bank behind it. The FDIC resolution process returns insured deposits to account holders. This is precisely why verifying FDIC coverage before depositing is non-negotiable — the partner bank structure is what makes the protection work.

Do neobanks affect your credit score?

Opening a standard neobank checking or savings account does not affect your credit score — no hard inquiry is generated for deposit accounts. Some neobanks offer credit-building products like secured cards or credit-builder loans that do report to credit bureaus and can positively impact your score over time. If a neobank runs a credit check for a premium account or lending product, that specific application may generate a hard inquiry.

Why do neobanks offer higher savings rates than traditional banks?

Lower operating costs. Without branch networks, physical infrastructure, or large branch staff, neobanks operate at a fraction of the overhead of traditional banks. The savings rate a bank can offer is determined partly by what it earns on deposits and partly by how much it needs to retain to cover operating costs. Lower costs allow neobanks to pass more of their deposit earnings to customers as higher APYs while still maintaining profitable operations.

Disclaimer: This content is for informational and educational purposes only and does not constitute financial advice. FDIC coverage, neobank features, APY rates, and fee structures change — verify current terms directly with each provider before opening an account. Neobank partner bank arrangements may affect FDIC coverage in specific circumstances; review each institution’s disclosure documentation for full details. PersonalOne does not endorse specific neobanks or financial products.