April 3, 2026

April, 2026

Home › Financial Stability › Financial Shock Absorption › What To Do If You Lose Your Job

This article is part of the Financial Shock Absorption cluster on PersonalOne — the complete tactical framework for managing acute financial crises, income disruption, and emergency cash flow.

Don Briscoe is a financial systems coach with 12+ years of experience helping Millennials and Gen Z build income and financial stability. He founded PersonalOne to provide the financial education he wished existed — structured, honest, and free.

What You Need to Know

— The first 48 hours after job loss determine how much financial damage the disruption causes — most people wait too long to act

— File for unemployment benefits the same day or the day after — there is typically a waiting period before payments start, so every day of delay costs money

— Switch immediately to a bare-bones budget that covers only survival expenses — discretionary spending stops until income is replaced

— Contact your landlord, lenders, and utility providers proactively — most have hardship programs that are only available if you ask before falling behind

— Your emergency fund is designed for exactly this situation — use it, but deploy it strategically to extend your runway as long as possible

If you are reading this because you just lost your job — or because you can see it coming — a job loss financial plan that you execute immediately is worth more than any amount of planning done after the financial damage has already accumulated. The financial steps after losing a job follow a specific sequence that most people get wrong because they delay the most critical actions while focusing on the least urgent ones. The complete framework for managing financial shocks of all kinds is in the Financial Shock Absorption guide.

The financial shock absorption strategy for job loss is built around one principle: extend your cash runway as long as possible while income is being replaced. Every week of runway you add — through cutting expenses, accessing benefits, and deploying emergency funds strategically — is a week of reduced pressure during the job search. Pressure reduces decision quality. Extended runway improves it. The complete financial stability framework that supports recovery is in the financial stability guide.

Step 1: File for Unemployment Benefits Today

Unemployment insurance is the most important financial action after job loss and the one most people delay. File the same day you lose your job or the following morning. Most states have a 1–2 week waiting period before your first payment arrives — that clock does not start until you file. Every day you wait is a day you push your first payment further into the future.

File online through your state’s unemployment insurance portal. You will need your employer’s name and address, your employment start and end dates, your reason for separation, and your Social Security number. If you were laid off or let go without cause, you almost certainly qualify. If you were fired for cause or quit voluntarily, eligibility depends on the specific circumstances and state law — file anyway and let the agency make the determination. You can appeal a denial.

Unemployment insurance typically replaces 40–60% of your previous wages up to a state-set weekly maximum. It will not cover everything, but it significantly extends your runway. Treat it as the floor your budget is built on during the job search period.

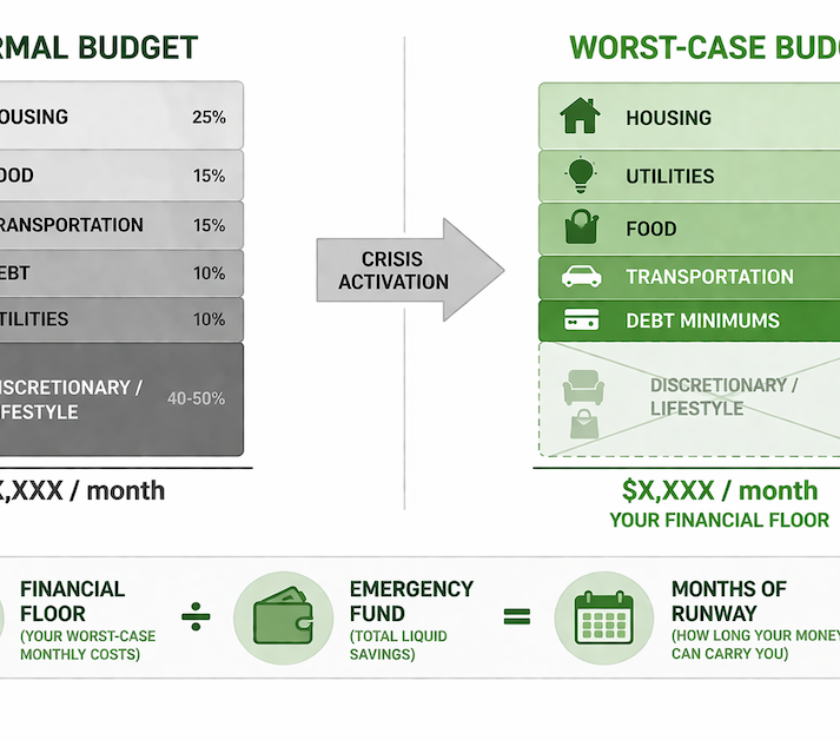

Step 2: Switch to a Bare-Bones Budget Immediately

The day you lose your job, discretionary spending stops. Not gradually — immediately. Dining out, entertainment, subscriptions, clothing, and any non-essential spending are paused until income is replaced. This is not punishment; it is runway math. Every $50 of discretionary spending you eliminate extends the time your emergency fund and unemployment benefits cover your survival expenses.

Calculate your bare-bones monthly number: rent or mortgage, utilities, groceries, minimum debt payments, transportation to job search and interviews, and health insurance. Everything else is deferred. This number is your target monthly burn rate during the job search. Divide your available cash (emergency fund plus anticipated unemployment benefits) by this number to determine how many months of runway you have. Knowing your runway number removes the panic from the situation and allows you to make deliberate decisions.

Step 3: Contact Every Lender and Service Provider Proactively

Call your landlord, mortgage servicer, auto lender, credit card companies, and utility providers before you miss a payment. Every one of these entities has hardship programs that most people never access because they wait until they are already behind. Hardship programs typically include deferred payments, reduced minimum payments, interest rate reductions, or waived late fees during a documented financial hardship period.

When you call, say: “I was recently laid off and I want to discuss hardship options before I fall behind. What programs do you have available?” Document every call — the representative’s name, date, and what was offered. Get any agreement in writing or via email before relying on it. Proactive contact before a missed payment produces significantly better outcomes than reactive contact after one.

Step 4: Review Health Insurance Options Within 30 Days

Job loss is a qualifying life event that triggers a 30–60 day special enrollment window for health insurance marketplace plans. This is critical: if you miss this window, you may not be able to get non-emergency coverage until the next open enrollment period. Review your options immediately after job loss. COBRA continuation coverage allows you to keep your employer plan but you pay the full premium — often $400–$700/month for an individual. A marketplace plan through Healthcare.gov may be significantly less expensive given your reduced income. Compare both options within the first week.

Step 5: Deploy Your Emergency Fund Strategically

If you have an emergency fund, this is its purpose. Use it. But deploy it strategically rather than drawing it down all at once. Keep it in your FDIC-insured high-yield savings account and transfer only what is needed for each month’s survival expenses. This keeps the money earning interest and makes your runway visible month by month. Do not consolidate it into checking, where it will get spent without a clear accounting of what it is covering.

If you do not have an emergency fund, the priority order is: file for unemployment, contact all lenders for hardship options, cut to bare-bones budget, and exhaust all available assistance programs before using credit cards to cover living expenses. Credit card debt on top of job loss compounds the recovery period significantly.

Job loss is a financial shock. The framework exists for exactly this.

The complete tactical guide to managing income disruption, cutting expenses fast, and protecting your financial position is in the Financial Shock Absorption guide.

Explore Financial Shock Absorption →Resources

Official Sources

DOL — Unemployment Insurance — Department of Labor guidance on unemployment insurance eligibility, how to file, state-by-state benefit information, and your rights during the claims process.

SSA — Benefits Information — Social Security Administration overview of available federal benefits during income disruption, including disability and survivor benefits that may apply to your situation.

CFPB — Consumer Tools — Consumer Financial Protection Bureau tools for managing debt, understanding your rights with creditors, and navigating financial hardship programs during income disruption.

Return to the financial stability guide for the complete system this cluster is part of.

Frequently Asked Questions

Should I use my emergency fund or wait for unemployment first?

File for unemployment immediately and begin your bare-bones budget the same day. Use your emergency fund to bridge the gap during the unemployment waiting period rather than charging living expenses to credit. Once unemployment payments begin, reduce emergency fund draws to only cover the difference between benefits and your bare-bones budget. Preserve as much emergency fund as possible as runway insurance.

How long can I collect unemployment?

Standard unemployment benefits last up to 26 weeks in most states, though this varies by state. During periods of high unemployment, federal extended benefits programs may be available. Your state workforce agency will provide the specific duration and benefit amount applicable to your situation when you file. Do not assume the maximum — get the actual numbers from the agency.

What if I was fired rather than laid off?

Unemployment eligibility after termination depends on the reason for separation and your state’s specific standards. Termination without misconduct often qualifies. Termination for documented misconduct may disqualify you. File anyway and allow the agency to make the determination — you have the right to appeal a denial and to provide your account of the separation circumstances.

Disclaimer: This article is for informational and educational purposes only. Unemployment eligibility, benefit amounts, and hardship program terms vary by state and institution. Verify current details with your state workforce agency and individual creditors.