May 18, 2026

Updated: May 2026

Home › Financial Stability › Long-Term Financial Resilience › Stability Before Investing

Part of the Financial Stability hub — Stage 1 of the PersonalOne Money System.

This article is in the Long-Term Financial Resilience cluster — building the foundation that makes wealth possible.

Don Briscoe is a financial systems strategist with 12+ years of experience helping Millennials and Gen Z build income and financial stability. He founded PersonalOne to provide the financial education he wished existed — structured, honest, and free.

What You Need to Know

— Stability before investing is not about waiting forever — it’s about removing the conditions that force you to sell or withdraw at the worst time.

— There are three specific stability layers required before investing makes sense: income floor, expense control, and emergency buffer.

— Skipping stability doesn’t make you an early investor. It makes you a forced seller.

— A clear readiness checklist exists — most people can reach it faster than they think if they sequence correctly.

— Once stability is in place, the transition to investing is straightforward. The foundation is the hard part.

The most common investing mistake is not picking the wrong stock. It’s starting to invest before the conditions exist for investing to work. Stability before investing is the sequencing principle that separates people who build wealth consistently from those who invest, panic, withdraw, and end up worse than when they started. If you have ever wondered whether you are ready to start investing — or whether you should be putting more in right now — this framework gives you a direct answer.

The financial content machine has one message: start investing as early as possible. That advice is not wrong in isolation. Time in the market matters. Compound growth is real. But that message skips the prerequisite entirely. You can invest early and still build no wealth if your foundation is missing, because an unstable financial situation will force decisions that erase the gains investing was supposed to create.

Building a long-term financial resilience system starts with sequencing — doing the right things in the right order. Investing is not the first step. It is the step that works after other work is done.

Real-World Experience:

One of the most common patterns I’ve seen working with people trying to build wealth is this: they start investing before their financial foundation is stable, not because they’re reckless — but because they’re trying to get ahead.

Here’s how it usually plays out. Someone builds up $1,000–$3,000, puts it into the market, and feels like they’re finally doing the “right thing.” Then life happens — a car repair, medical bill, job gap, or unexpected expense — and suddenly that investment account becomes their only available cash.

They withdraw the money early, often during a market dip, lock in losses or miss recovery gains, and end up right back where they started — or worse, discouraged from investing altogether.

The counterintuitive part is this: the biggest risk in investing early isn’t market volatility — it’s instability in your personal finances forcing bad timing decisions.

The fix isn’t to avoid investing — it’s to build a system first. That means stabilizing your income floor, controlling fixed expenses, and putting a real buffer between your daily life and your investments. Once that structure is in place, investing stops feeling risky — and starts working the way it’s supposed to.

Why Stability Before Investing Matters

The conventional framing of investment risk is market risk — the risk that the value of your portfolio declines. That is a real risk, but it is not the risk that actually derails most people. The risk that derails most people is personal liquidity risk: needing money at the wrong time. When your financial situation is unstable, you are far more likely to need to access your investment accounts during a market downturn — which means selling at a loss and locking in the damage that a patient investor would have recovered from.

Investing without stability is building on sand. The investment itself may be sound. The returns may be historically strong. But if a job loss, a medical bill, a car repair, or three slow months of income forces you to liquidate before a recovery, the investment did not fail — the sequencing did. Market volatility combined with personal financial instability creates forced decisions. You stop being an investor making choices and become someone responding to emergencies with whatever assets are available.

For anyone navigating variable income, this risk is amplified. People with irregular income face month-to-month uncertainty that makes investing premature without a proper income floor in place. Understanding how to build financial stability even when income is not consistent is the prerequisite step — not a detour from the investing path but the foundation of it.

The goal of stability before investing is not to delay wealth building indefinitely. It is to remove the conditions that make investing counterproductive. The complete framework for building that foundation — buffer layers, income stability, and the sequencing that makes each stage work — is covered in the Financial Stability hub. When your financial foundation is solid, market volatility becomes noise rather than a threat. That is when investing works the way it is supposed to.

The 3 Stability Layers You Need Before You Invest

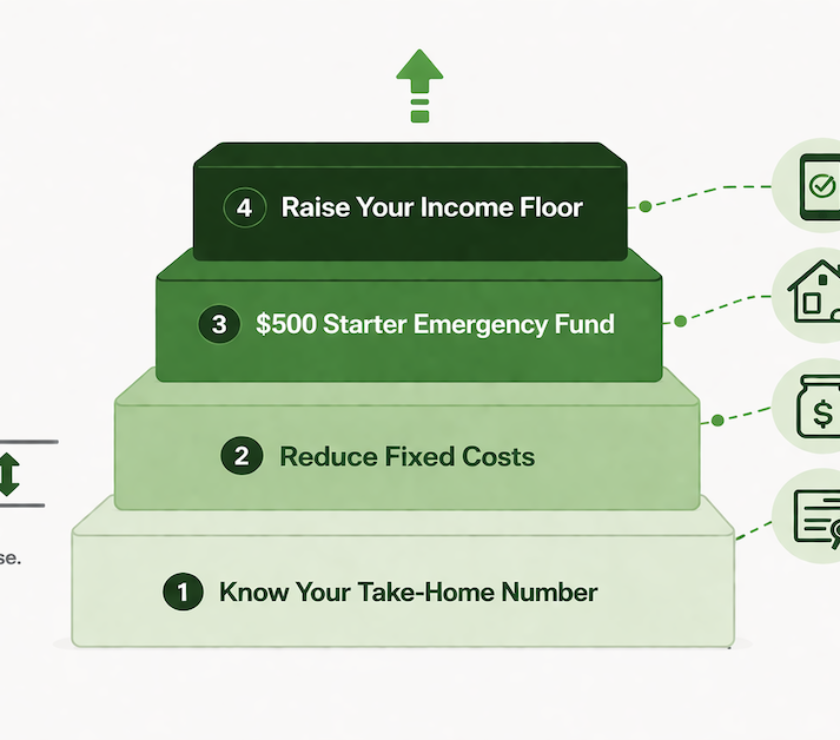

Stability is not a single condition. It is three distinct layers that build on each other. Each layer removes a specific type of vulnerability. Missing any one of them leaves a gap that will surface at the worst possible time. The layers are income stability, expense control, and an emergency buffer. All three need to be in place before investing moves from theory to action.

1. Income Stability (or Income Floor)

Income stability does not mean high income. It means predictable minimum income — a consistent floor you can rely on to cover obligations every month. The amount matters less than the reliability. Someone earning $3,800 per month consistently is in a better position to invest than someone whose income swings between $2,000 and $7,000 with no predictability, even if the average is higher.

The income floor concept is especially relevant for freelancers, gig workers, contractors, and anyone in commission-based or seasonal work. These income profiles are not barriers to building wealth, but they require a specific setup before investing makes sense. The irregular income survival guide covers the mechanics of how to establish a floor when your income is variable — this is the income stability work that must precede the investing conversation.

Without an income floor, investing is speculation on your own financial stability. You are betting that your income will stay consistent enough that you will not need to touch your investments. That is a bet that regularly loses. Building financial resilience starts by establishing what your minimum reliable income actually is — and structuring your obligations around that number, not your best month. Developing the financial habits in your 20s that prioritize income floor before investment contributions is one of the highest-leverage sequencing decisions you can make early in your financial life.

2. Expense Control (Fixed Cost Discipline)

If your fixed expenses are not under control, investing becomes irrelevant. Every dollar that goes into an investment account is a dollar that cannot cover an obligation. When fixed costs are misaligned with income — too high relative to the income floor, or loaded with discretionary spending disguised as recurring commitments — the investment account becomes a pressure relief valve rather than a wealth-building vehicle.

Expense control is not about cutting everything down to nothing. It is about understanding exactly what your financial obligations are each month and ensuring there is a workable gap between your income floor and those obligations. That gap is where investing, saving, and flexibility live. Without the gap, you are plugging leaks. The investment may technically exist, but it will be raided whenever the gap closes. Learning how to build a budget that actually works is what creates that gap deliberately rather than by accident.

Fixed cost discipline also means distinguishing between true fixed costs — rent, utilities, debt obligations — and creeping commitments that have become fixed in practice but could be restructured. Subscription stacks, auto-renewals, lifestyle inflation that has hardened into obligation — these need to be audited before any investment plan is sound. The goal is a fixed cost structure low enough that your income floor can cover it with margin to spare.

3. Emergency Buffer (Non-Negotiable)

The emergency buffer is the layer that makes everything else work. Without it, your investment account is your emergency fund — regardless of whether you intend it to be. Life does not ask permission before generating expenses. When an unexpected cost hits and there is no buffer, something gets liquidated. The investment account is almost always the first option people reach for, especially if other debt obligations are also being managed.

Three to six months of essential expenses in a separate, accessible account is the standard target. This is not an arbitrary number. It reflects the realistic duration of most income disruptions — job loss, medical recovery, major repair — before they resolve. Under three months leaves you exposed to events that take longer than expected. Over six months is fine but should not come at the expense of delaying investing indefinitely once the lower threshold is reached.

Understanding how to build an emergency fund that protects you from setbacks is the structural foundation of the entire investing readiness framework. This layer does not compete with your investment account. It protects it. Once the buffer exists, market volatility is not your problem — it is just movement you can wait out.

What Happens If You Skip This Step

The investing content ecosystem is filled with advice that is technically accurate but contextually dangerous. “Start investing with $10 and you will be rich.” “You do not need savings — just invest.” “Time in the market beats timing the market.” Each of these statements has truth in it. None of them acknowledge the conditions required for that truth to apply to your specific situation.

Here is what the skipped-step outcome actually looks like. Someone starts investing $200 per month. Six months in, a car transmission fails — $1,400. No emergency fund. They withdraw from their investment account. They pay an early withdrawal penalty if it is a retirement account. They sell during a normal market dip because the timing of emergencies does not respect market cycles. They feel like investing did not work. They stop. Their actual outcome after 18 months of effort is worse than if they had just built the emergency buffer first and started investing three months later.

This is not a rare scenario. It is the most common pattern. The failure is not the investment. The failure is the sequencing. The financial goal setting framework that works is one built around sequencing — not just setting a savings target but placing the right financial moves in the right order so each one creates the conditions for the next to succeed.

The emotional cost compounds the financial one. People who invest before they are stable often walk away from investing entirely after the first disruption forces them to withdraw. They do not just lose the gains — they lose confidence in the system. Getting the sequence right the first time is not just financially optimal. It is the difference between someone who becomes a long-term investor and someone who tried and stopped.

When You Are Actually Ready to Start Investing

Readiness is not a feeling — it is a checklist. The emotional desire to invest, the fear of missing out on market gains, or the social pressure to be building wealth are not readiness signals. The following conditions are. When all of these are true at the same time, investing is appropriate and structurally sound.

You are ready to invest when your monthly income floor covers all fixed obligations with a consistent surplus. Not occasionally — consistently. The surplus does not need to be large, but it needs to be reliable. If your income is variable, your income floor — not your average or your best month — needs to cover obligations. This means the floor has been calculated and the expense structure has been adjusted to match it.

You are ready when your emergency fund holds three to six months of essential expenses in a liquid, accessible account. Not in an investment account. Not in a retirement account. In something you can access within 24 to 48 hours without penalty or tax consequence. This is the buffer that allows your investment account to stay invested during disruptions.

You are ready when you are not carrying high-interest debt — typically anything above 7 to 8 percent APR. Paying down high-interest debt first is almost always the higher mathematical return. The guaranteed return of eliminating a 22 percent APR credit card balance outperforms most reasonable investment return expectations. Once high-interest debt is cleared and the buffer is in place, investment contributions become the next right move.

Finally, you are ready when market fluctuations do not feel like a crisis. If checking your account balance during a down week creates genuine financial anxiety — not just emotional discomfort but actual concern about covering obligations — that is a signal the foundation is not yet solid enough. When the foundation is in place, a 12 percent portfolio drawdown is just a number. When it is not, it is a threat. Understanding how to start investing with confidence starts with reaching the conditions where confidence is structurally justified, not just emotionally willed.

Build the Foundation First

The Long-Term Financial Resilience hub covers the complete sequencing system — from income floor to wealth building — in one place.

Go to the HubThe Transition: Stability to Wealth Building

Once the three stability layers are in place, the transition to investing is not complicated. It is simply the next step in a sequence that is already working. The income floor is set. Fixed costs are under control. The emergency buffer means that market fluctuations are a non-event. At that point, investment contributions are just a matter of deciding how much of the monthly surplus to allocate and selecting the vehicle — retirement account, brokerage account, index fund strategy — that fits the goal.

This is where the payoff of doing the foundation work becomes visible. Investors who built stability first do not panic sell. They do not withdraw during downturns. They contribute consistently because their financial structure does not require them to make desperate decisions. Over a ten-to-twenty year horizon, the difference between a consistent investor and an inconsistent one — driven almost entirely by whether the foundation existed — is significant.

Stability removes fear from investing. When you are not worried about covering rent if the market drops 15 percent, you stay invested. Staying invested is the primary mechanism through which compound growth actually works at scale. The foundation is not a delay to wealth building — it is the condition that makes wealth building structurally possible.

Understanding how investing and wealth growth actually works long term makes clear that the behavioral component — staying invested through volatility — is more important than any specific investment selection. Stability is what makes that behavior possible. The financial stability system is not separate from the investing strategy. It is the first layer of it.

Official Sources

Consumer Financial Protection Bureau — Building an Emergency Fund: Federal guidance on emergency savings targets and structure. consumerfinance.gov

IRS — Early Withdrawal Rules: Official documentation on penalties and tax consequences of early investment account withdrawals. irs.gov

Federal Reserve — Report on the Economic Well-Being of U.S. Households: Annual data on emergency savings readiness and financial fragility across income levels. federalreserve.gov

Continue Building Your System

This article is part of the Long-Term Financial Resilience cluster. Start there for the complete sequencing framework from income foundation to wealth building.

Does stability before investing mean I should wait until I have no debt?

Not all debt disqualifies you from investing. The threshold is high-interest debt — typically above 7 to 8 percent APR. Student loans at 4 percent, a mortgage, or a car loan at 5 percent do not need to be fully paid off before investing. The math simply does not support waiting on low-interest debt when investment returns are likely to exceed the interest cost. High-interest consumer debt — credit cards, payday loans, personal loans above 8 percent — should be cleared first. The rule is not zero debt. It is no high-cost debt.

How long does it realistically take to reach investing readiness?

For most people starting from a position of limited savings and moderate debt, six to eighteen months of focused stability work gets the foundation in place. The income floor is usually clarified within the first month of tracking. Expense restructuring typically takes two to three months to settle. The emergency fund — targeting three months of essentials — is the longest piece. At $300 per month of dedicated savings, that is roughly nine to twelve months. This timeline can compress significantly with any income increase or expense reduction. The point is not that it is fast — it is that it is finite. The foundation work has an end.

What if my employer offers a 401k match? Should I still wait?

Employer matching is the one exception to the stability-first sequence. If your employer matches contributions up to a certain percentage, contributing at least enough to capture the full match is almost always worth doing even before the full stability foundation is built. A 50 percent or 100 percent match is an immediate guaranteed return that no other financial move can match. Contribute enough to capture the match. Then prioritize the stability layers. Once the foundation is in place, increase contributions.

How is an emergency fund different from investment savings?

An emergency fund must be liquid, accessible, and stable in value. A high-yield savings account or money market account is appropriate. An investment account — even a conservative one — is not. The critical difference is that an emergency fund needs to be accessible within 24 to 48 hours without penalty, tax consequence, or concern about selling at a loss. Investments can decline in value at exactly the moment you need the funds. The emergency fund exists to ensure you never have to touch the investment account in an emergency. They serve different structural purposes and should be in separate accounts.

Can you invest and build an emergency fund at the same time?

In theory, yes. In practice, splitting focus usually means the emergency fund grows slowly enough that it never actually provides protection. A partial emergency fund does not remove the risk of a forced sale — it just means the disruption has to be smaller to trigger it. The higher-leverage approach for most people is to build the emergency fund to the three-month target first, then redirect the savings contribution to investing. This usually adds three to nine months to the start date but substantially improves the probability of staying invested once you do start.

Is stability before investing relevant for high earners?

Yes, and this catches a lot of high earners off guard. High income does not equal stability. High income with high fixed costs, no emergency buffer, variable bonus structures, and high-interest debt is financially fragile regardless of the gross income number. The stability framework applies at every income level. The thresholds are larger for high earners — three months of a higher expense base is more money — but the logic is identical. Income level is not a proxy for financial foundation quality.

This content is for educational purposes only and does not constitute financial advice. PersonalOne is not a licensed financial advisor, broker, or investment professional. Individual financial situations vary — consult a qualified financial professional for personalized guidance.