June 12, 2026

June, 2026

Home › Financial Stability › Financial Shock Absorption › The 30-Day Income Disruption Plan

This article is part of the Financial Shock Absorption cluster on PersonalOne — the tactical framework for managing job loss, surprise expenses, and crisis cash flow sequencing.

Don Briscoe is a financial systems strategist with 12+ years of experience helping Millennials and Gen Z build financial stability and income systems. He founded PersonalOne to provide the financial education he wished existed — structured, honest, and free.

What You Need to Know

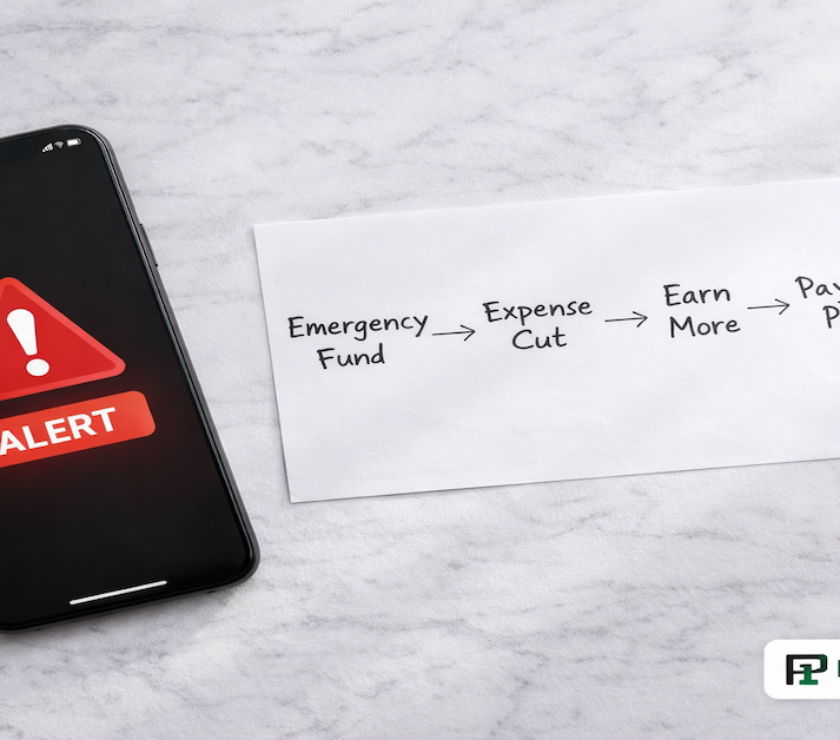

— The first 30 days after income stops are the most financially consequential — the decisions made in this window determine how long your resources last

— Day 1 through 7 is triage: calculate your runway, switch to bare-bones budget, and file for unemployment benefits immediately

— Day 8 through 14 is communication: contact creditors, landlord, and lenders before you miss payments — not after

— Day 15 through 21 is cash flow protection: identify every asset and income source available and sequence them correctly

— Day 22 through 30 is recovery activation: build your income replacement plan with a realistic timeline and daily action structure

Income disruption is a financial blizzard. It can arrive suddenly, cut off normal cash flow, cloud judgment, and turn a manageable situation into a crisis if you move without a plan. Whether it shows up as a layoff, lost clients, a business collapse, or an unexpected medical leave, the first 30 days are everything. Most people spend that window in shock, reacting emotionally and exhausting resources faster than necessary, when careful sequencing is what actually gets you through.

This plan gives you the exact sequence for the first 30 days: what to do, when to do it, and in what order. The financial shock absorption strategy is built around the insight that income disruption is survivable when managed structurally — and catastrophic when managed emotionally. The plan works whether you saw the disruption coming or it arrived without warning. The sequence is the same. The timeline is the same. The only variable is how much preparation you had in place before it happened.

Before the Plan: The Three Numbers You Need Immediately

Before executing any week of the plan, you need three numbers. These are not estimates. They are exact figures pulled from your accounts within the first 24 hours of income disruption.

Number 1: Your bare-bones monthly expense total. The absolute minimum required to maintain shelter, utilities, food, transportation, and minimum debt payments. Not your normal budget. Not your comfortable budget. The number that covers only survival categories. For most single individuals in mid-cost cities, this falls between $1,800 and $2,800 per month. For couples, between $2,800 and $4,200. If you have not calculated this number yet, the worst-case scenario budget guide walks through the exact calculation step by step.

Number 2: Your available liquid resources. Total your emergency fund, all savings accounts, and any liquid investments you could access within 48 hours without penalty. Do not include retirement accounts in this number — early withdrawal penalties and tax consequences make retirement accounts a last resort, not a first response.

Number 3: Your runway in months. Divide your liquid resources by your bare-bones monthly number. Add any expected unemployment benefits to your monthly resource pool before dividing. The result is your runway — the number of months you can cover essential expenses before liquid resources are exhausted. This number drives every subsequent decision in the plan.

Days 1 Through 7: Triage

The first week is entirely about triage. You are not solving the income problem this week. You are stabilizing the financial situation so that solving the income problem has time and resources to work.

File for unemployment immediately. If your disruption qualifies for unemployment insurance, file on Day 1 — not Day 7, not next week. Most states have a waiting period before benefits begin. Every day you delay filing extends the period before benefits arrive. File online the same day income stops. The complete immediate-action checklist for what to do financially if you lose your job covers this first-day sequence in full detail.

Switch to the bare-bones budget today. Do not wait until money gets tight to cut spending. Cut it now. Cancel every non-essential subscription and recurring charge this week. Stop all discretionary spending. The goal is to extend your runway by reducing the monthly burn rate as quickly as possible. The emergency budget plan walks through exactly how to build your bare-bones number and structure your survival spending by category.

Freeze all non-essential automatic payments. Review every automatic charge on your accounts. Cancel or pause anything not in the bare-bones category. Do this before the next billing cycle to prevent charges from hitting your account while you are in the process of reducing spend.

Do not touch retirement accounts. Early withdrawal from a 401(k) or IRA triggers a 10% penalty plus income tax on the amount withdrawn. A $10,000 withdrawal can cost $3,000 to $4,000 in immediate tax consequences. This is not a Day 1 resource. It may never be necessary if the plan is executed correctly. The financial stability framework specifically sequences this as a final resort, not a first response.

Days 8 Through 14: Creditor Communication

The second week is about proactive communication with every creditor and landlord. This is the step most people skip — and skipping it is expensive. Creditors have hardship programs. Landlords can negotiate. Lenders have deferral options. None of these become available after you miss a payment. They are available before.

Contact your landlord or mortgage servicer. If you rent, inform your landlord of your situation and ask specifically about deferral, partial payment arrangements, or temporary rent reduction. Many landlords prefer a negotiated arrangement over an eviction process. If you have a mortgage, contact your servicer and ask about forbearance options.

Contact credit card issuers. Call the hardship number on the back of each card and explain that you have experienced income disruption. Ask specifically about hardship programs that reduce interest rates, waive minimum payments temporarily, or suspend late fees during the hardship period. These programs exist. They are not advertised. You must ask for them explicitly. The full script and strategy for how to negotiate with creditors during financial hardship gives you the exact language and approach for each type of creditor.

Contact utility providers. Most utility companies offer payment plans, low-income assistance programs, or temporary deferral for customers experiencing financial hardship. Call before a bill is overdue. Programs available to customers in good standing are different from programs available to customers already in arrears.

Contact student loan servicers if applicable. Federal student loans have income-driven repayment options, deferment, and forbearance available for income disruption. Private student loans vary by lender but many have hardship programs. Contact your servicer this week, not when a payment is missed.

Days 15 Through 21: Cash Flow Protection

Week three is about identifying every available resource and sequencing it correctly to maximize runway. You are building a complete picture of what is available and in what order it should be used.

Identify all income sources available now. Beyond unemployment benefits, assess: any freelance or gig work you can begin immediately, any skills that can generate short-term contract income, any assets that can be sold without major loss, any government assistance programs you qualify for (SNAP, LIHEAP, Medicaid), and any family support options that do not create long-term financial obligation.

Sequence your resources correctly. The correct draw-down sequence for most people: first, incoming unemployment or any active income; second, emergency fund; third, general savings; fourth, taxable investment accounts if applicable; fifth, Roth IRA contributions (not earnings) which can be withdrawn without penalty; and only as a last resort, pre-tax retirement accounts. Each step in this sequence should be exhausted or nearly exhausted before moving to the next. Skipping ahead costs money in penalties and taxes that your runway cannot absorb.

Review your insurance situation. If you lost employer-sponsored health insurance, you have a limited window to elect COBRA coverage or enroll in a marketplace plan through a Special Enrollment Period triggered by job loss. Missing this window can leave you uninsured with no recourse until the next open enrollment period. Handle this in week three, not when a medical need arises. The income disruption management framework is in the income volatility management cluster.

Days 22 Through 30: Recovery Activation

By week four, the financial triage is complete and the recovery plan needs to be operational. This is a structured income replacement plan with a specific timeline and daily accountability structure.

Calculate your income replacement deadline. Using your runway number, identify the latest date by which you need replacement income to begin in order to avoid resource exhaustion. Work backward from that deadline to set weekly income milestones. If your runway is 4 months, your replacement income target date is not 4 months from now — it is 2 to 3 months from now, leaving buffer for ramp-up time.

Structure your recovery as a job. Set daily work hours, weekly output targets, and weekly review checkpoints. Treat income recovery with the same structure you would apply to paid work. Define daily minimums: number of applications, number of network contacts, number of follow-ups.

Identify short-term and long-term income tracks simultaneously. The short-term track is immediate income to extend runway — freelance work, contract positions, gig work, temporary employment. The long-term track is your primary career or income path recovery. Running both tracks in parallel prevents the short-term income from displacing the long-term recovery. The budgeting through income transitions framework covers how to manage spending allocation as income recovery begins and ramps up.

30 days. Clear sequence. Your resources intact.

This plan is one part of the complete Financial Shock Absorption system — the full framework for managing crisis cash flow, creditor negotiation, and financial recovery is in the cluster hub.

Financial Shock Absorption → Financial Stability Hub →After Day 30: The Recovery Arc

Day 30 is not the end of the disruption plan — it is the transition point from crisis management to structured recovery. By Day 30, the bare-bones budget should be operational, all creditor communications should be complete, the resource sequencing plan should be in place, and the income recovery structure should be active.

From Day 30 onward, the plan operates on monthly review cycles. Every 30 days: confirm current runway based on actual spending versus bare-bones budget, assess income recovery progress against the timeline, adjust resource sequencing if income has partially recovered, and determine whether creditor arrangements need renegotiation. The recovery is complete when replacement income consistently covers the bare-bones budget and begins rebuilding the emergency fund. Not when income reaches the pre-disruption level — that comes later. The first milestone is coverage. Everything above coverage goes back to rebuilding the buffer and reserves the disruption consumed. If you want to avoid being in this position in the future, the preparation checklist for a voluntary departure is in the guide on how to prepare financially before you quit a job.

Resources

Official Sources

DOL: Unemployment Insurance Overview — Department of Labor guidance on unemployment insurance eligibility, how to file, and what to expect from the benefits process.

CFPB: Dealing with Debt and Creditors — Consumer Financial Protection Bureau resources on your rights when communicating with creditors, including hardship program guidance.

Healthcare.gov: Special Enrollment Periods — Official guidance on health insurance enrollment windows triggered by job loss.

Benefits.gov: Federal Assistance Programs — Official federal resource for identifying government assistance programs available during income disruption.

Continue Building Your Shock Absorption System

The Worst-Case Scenario Budget — Build your bare-bones monthly number before income stops — the calculation you need on Day 1.

Why Organizing Your Key Financial Documents Is a Smart Move — The document preparation that makes Days 1 through 7 faster and less costly.

The full Financial Stability framework is in the Financial Stability guide.

Frequently Asked Questions

What if I do not qualify for unemployment insurance?

Self-employed workers, independent contractors, and gig workers typically do not qualify for traditional state unemployment insurance. Your resource sequencing plan relies more heavily on emergency savings and short-term income activation. The bare-bones budget and runway calculation are even more critical in this situation because there is no unemployment benefit to include in the monthly resource pool.

How do I talk to creditors without making the situation worse?

Lead with facts, not emotion. State clearly that you have experienced income disruption, give a realistic timeline for when you expect the situation to change, and ask specifically what hardship options are available. Do not make commitments you cannot keep. Keep records of every call — date, time, representative name, and what was agreed.

Should I stop paying credit cards to preserve cash?

Only as a deliberate last-resort decision, not as a default. Missing credit card payments triggers late fees, penalty interest rates, and credit score damage that creates lasting financial consequences. Before stopping payments, exhaust the hardship program options available through the card issuer. If you must choose between a credit card minimum and housing or food, housing and food take priority — but this should be a deliberate sequencing decision, not an accidental one.

What is the right bare-bones grocery budget?

The USDA publishes monthly food plan cost data by household size that serves as a useful benchmark. The Thrifty Food Plan represents the lowest-cost nutritionally adequate food budget. For a single adult, this typically falls between $200 and $280 per month. For a couple, between $380 and $470. These are genuine minimums based on home cooking with deliberate meal planning.

How do I know when the income disruption plan is officially over?

The disruption plan ends when three conditions are met simultaneously: replacement income is consistently covering your bare-bones budget, you have begun rebuilding your emergency fund from the disruption drawdown, and you have exited any creditor hardship arrangements and returned to normal payment schedules.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, legal, or tax advice. Unemployment insurance eligibility, creditor hardship programs, and government assistance programs vary by state, lender, and individual circumstance. Consult qualified professionals for guidance specific to your situation. PersonalOne is not a licensed financial advisor.