April 16, 2025

Are banks quietly draining your wallet? A recent report from the Consumer Financial Protection Bureau (CFPB) reveals that Americans paid a massive amount in hidden banking fees in 2024. The total exceeded $40 billion. Many of these fees were never clearly disclosed. Now in 2025, the stakes are even higher as financial institutions ramp up lesser-known charges under the radar, especially for mortgage holders.

From maintenance fees to early withdrawal penalties and even confusing mortgage rate locks, these fees can quietly sabotage your financial goals. If you’re trying to save money on your mortgage, hidden fees may be the biggest roadblock you didn’t even know you had.

Let’s unpack where your money might be slipping away—and how to stop it.

The Hidden Banking Fees Trap: What to Watch Out for in 2025

Primary Hidden Bank Fees in 2025 (Updated List)

Here’s what banks are charging you for—often without you noticing:

- Monthly maintenance fees – Often around $10–$25 just to keep your account open.

- Overdraft protection fees – Sounds like help, but it can cost up to $35 per transaction.

- ATM out-of-network fees – Some now exceed $5 per withdrawal.

- Returned deposit fees – You’re charged when someone else’s check bounces. Yep.

- Mortgage service fees – Includes payment processing or payoff statement charges.

- Mortgage rate lock extension fees – Can cost hundreds if your loan takes longer to close.

“We’re seeing a surge in junk fees being rebranded with new names in 2025. The goal? To confuse consumers,” said David Uejio, Senior Advisor at the CFPB.

How Mortgage Customers Are Hit the Hardest

Trying to Save Money on Your Mortgage? These Fees Could Cost You More

If you’re refinancing or buying a home this year, beware of:

- Application and origination fees

- “Rate lock” fees if closing is delayed

- Hidden document handling fees

- Early payoff penalties

A Bankrate survey in March 2025 found 38% of borrowers paid unexpected fees at closing—most over $500.

And it’s not just traditional banks. Digital lenders and mortgage servicers are joining the party. Even “no fee” claims often hide costs in the fine print.

How to Spot and Avoid These Hidden Costs

Here’s how to protect yourself and save real money:

✅ Read the full fee schedule (yes, that PDF link).

✅ Ask for a Loan Estimate form when applying for a mortgage.

✅ Opt for fee-free or low-fee banks or credit unions.

✅ Use apps like NerdWallet or Rocket Money to track fees.

✅ Ask your bank to waive maintenance or overdraft fees—many will.

“Fees aren’t always avoidable, but they are often negotiable,” says Erin Lowry, author of Broke Millennial.

Real People, Real Impact

In New Jersey, newlywed couple Jasmine and Marcus thought they were locked into a 6.5% mortgage rate—until their bank tacked on a $600 extension fee just days before closing.

“We felt blindsided. That money was supposed to go toward our first home repair,” said Jasmine. “Now we’re telling our friends to double-check everything.”

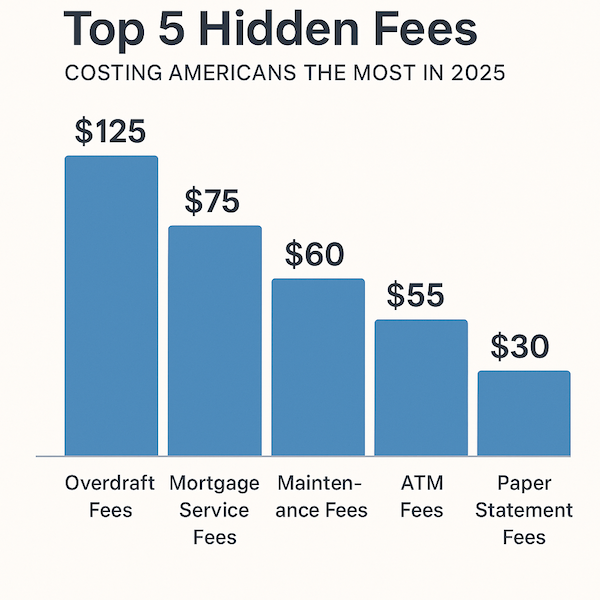

📊 Infographic: Top 5 Hidden Fees Costing Americans the Most in 2025

✅ What You Can Do Right Now

- Compare banks using fee transparency ratings (see CFPB Consumer Bank Rankings).

- Switch to fee-free or online banks like Ally, Chime, or Capital One 360.

- Ask mortgage lenders about every fee upfront—and get it in writing.

🛠️ Closing Summary

In 2025, banks are using new tricks to sneak in old fees. Whether you’re opening a checking account or trying to save money on your mortgage, staying informed is your best defense. Hidden fees are real, they’re rising, and they can quietly cost you hundreds—or more—if you’re not paying attention.

🔎 FAQ: Hidden Bank Fees in 2025

Q: What’s the most common hidden bank fee in 2025?

A: Overdraft protection fees, especially from traditional banks.

Q: Can mortgage fees be negotiated?

A: Yes. Many lenders will waive or reduce application or rate lock fees if you ask.

Q: How do I find out if my bank is charging me hidden fees?

A: Check your statements monthly and request a full fee disclosure document.

📣 Ready to fight back against hidden fees?

Subscribe to the PersonalOne newsletter for weekly tips. Learn how to cut banking costs. Discover ways to lower your mortgage payments. Build real wealth—no smoke and mirrors.

👉 Subscribe Now

Sources:

- Consumer Financial Protection Bureau – “Junk Fees Report 2025”

- Bankrate – Mortgage Fee Survey (2025)

- Federal Reserve – Banking Industry Fee Analysis

- How to Save Thousands on Your Mortgage

⚠️ Financial Disclaimer

This article is for informational purposes only and should not be considered financial advice. Always consult a licensed financial advisor before making banking or mortgage decisions.

Tags: hidden fees, mortgage costs, bank fees 2025, save money, personal finance, CFPB, mortgage rate lock