January 30, 2026

Updated: March 18, 2026

Home › Banking Systems › Multi-Account Budgeting System › How to Fix Banking Mistakes That Are Quietly Costing You Money

This article is part of the Multi-Account Budgeting System cluster on PersonalOne. Use it to identify the banking fees and structural mistakes quietly draining your account — and the one-time fixes that stop each one permanently.

How to Fix Banking Mistakes That Are Quietly Costing You Money

Don Briscoe is a personal finance coach with 12+ years of experience helping people take control of their money. As the founder of PersonalOne.org, Don specializes in building financial systems for Millennials and Gen Z that work in real life, not just on paper.

TL;DR

— Overdraft fees average $35 per occurrence and consistently hit accounts with the least money to spare.

— Monthly maintenance fees, minimum balance requirements, and ATM charges drain hundreds of dollars annually — often without the account holder realizing it.

— Poor account structure and lack of spending visibility cause the same mistakes to repeat regardless of intention or effort.

— Switching to no-fee banks and separating money by purpose prevents most of these costs structurally — one fix, permanent result.

— The combined cost of common banking mistakes runs $800 or more per year — money that compounds significantly over time if redirected instead.

Banking mistakes do not usually announce themselves. There is no dramatic moment when you realize you have been losing money through overdraft fees, maintenance charges, and poor account structures. Instead, these costs accumulate quietly — $35 here, $12 there — until the total damage runs into the hundreds or thousands per year.

Most people do not realize how much these errors are costing them until they do the math. This article covers the most common and expensive banking mistakes, why they keep happening, and the structural fixes that stop them from recurring. Each mistake on this list has a one-time solution. The reason they keep occurring is that the underlying banking mistakes that drain your account all trace back to the same root cause: all money living in one account with no structure, no boundaries, and no visibility into what is actually available to spend.

The Most Expensive Mistake: Overdraft Fees

Overdraft fees are the single largest money drain in consumer banking. According to the CFPB, Americans paid over $8 billion in overdraft fees in a single recent year. The average fee is $35 per transaction — meaning a $7 coffee purchased on a $5 balance costs $42 total. Three purchases before you notice the account is negative? That is $105 in fees on ordinary daily spending.

What makes overdrafts particularly damaging is transaction ordering. Many banks process larger transactions before smaller ones, so one large purchase drains the account and then every subsequent small transaction triggers its own separate fee. Some banks charge multiple overdraft fees per day with no daily cap.

The Overdraft Trap

Overdraft "protection" is frequently the problem rather than the solution. Opting into coverage means the bank processes the transaction and charges the fee — a declined transaction costs nothing. If you have not explicitly opted out of overdraft coverage, check your account settings today.

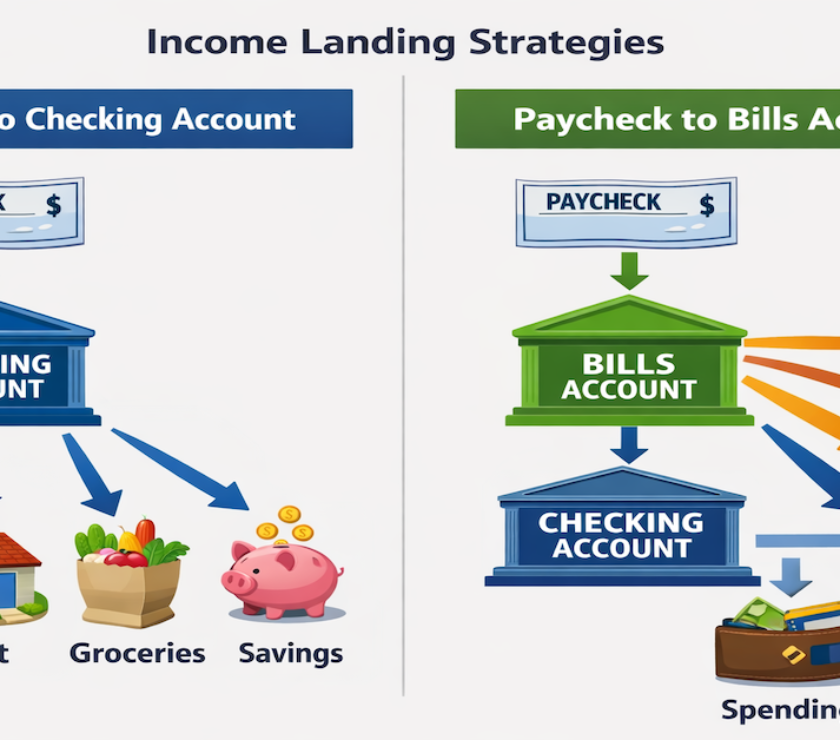

How to fix it: Opt out of overdraft coverage so your card gets declined instead of triggering a $35 fee — declined is better than $35 charged. Maintain a checking buffer by treating $150 to $200 as your mental zero and never letting the balance drop below that amount. Set low-balance alerts so a text or email fires when the account drops below $100, giving you time to act before a fee hits. Most importantly, separate bill money from spending money — when fixed expenses and daily spending share one account, it is structurally easy to overspend what is actually available. Account separation eliminates this at the source.

Monthly Maintenance Fees: Paying to Store Your Own Money

Traditional banks commonly charge $10 to $15 per month for a basic checking account — $120 to $180 per year for the privilege of holding your money. These fees are frequently waived if you meet conditions like maintaining a minimum balance or setting up direct deposit. But the waiver conditions are part of the problem: a $1,500 minimum balance sitting idle in a checking account earning nothing could instead be earning 4 to 5 percent APY in a high-yield savings account — roughly $60 to $75 per year in additional interest, on top of the $120 to $180 fee you would avoid by switching to a no-fee account.

How to fix it: Switch to a no-fee checking account that does not require minimum balances or conditional waivers. Online banks consistently offer full-featured checking at zero monthly cost. If staying at your current bank, calculate whether the minimum balance requirement actually costs more than the fee you are avoiding — it frequently does.

Why These Mistakes Keep Happening: The Visibility Problem

Most banking mistakes are not caused by carelessness — they are caused by structural invisibility. When money moves through subscriptions, autopay, and pending transactions simultaneously, the balance visible in your banking app is often not your true available balance. You see $300. But with a scheduled bill payment, a pending grocery charge, and a forgotten subscription renewal, you actually have $47. One grocery run later: overdraft fee.

This is the core problem that account separation solves. When bill money lives in a dedicated account that only covers bills, and spending money lives in a separate account with its own debit card, the balance in the spending account is your actual available money — no mental math, no invisible pending charges from other categories distorting the number.

ATM Fees: Small Charges, Large Annual Total

Out-of-network ATM fees appear minor per transaction — typically $2.50 to $3.50 from the ATM operator plus $2 to $3 from your own bank, totaling $4.50 to $6.50 per withdrawal. But two out-of-network ATM uses per week adds up to $468 to $676 per year. It is a cost that never appears as a line item in your budget and rarely registers as significant in the moment.

How to fix it: Choose banks with large ATM networks or fee reimbursement — many online banks refund all ATM fees monthly or participate in large fee-free ATM networks. Get cash back at checkout instead of visiting ATMs — grocery stores, pharmacies, and most major retailers offer free cash back with debit purchases. Reduce cash dependency by using payment apps for person-to-person transactions and digital wallets for daily spending wherever accepted.

Poor Account Structure: When Your Banking Works Against You

The most expensive banking mistake is not any individual fee — it is the account structure that makes all the other mistakes inevitable. When all money lives in one checking account, there is no natural boundary between bill money and spending money, no protection preventing impulse spending from hitting the savings balance, and no clear visibility into what is actually available for discretionary use at any given moment.

A Functional Account Structure

Account 1 — Bills: Fixed monthly expenses on autopay. No debit card needed. Never used for discretionary spending.

Account 2 — Spending: Groceries, gas, daily variable expenses. Debit card linked here only. Balance equals actual available money.

Account 3 — Emergency Fund: Three to six months of expenses in a high-yield savings account at a separate institution. Transfer friction protects it.

Account 4 — Goals: Vacation, car replacement, planned future purchases. Separate savings with labeled purpose.

With this structure, the spending account balance is your real available number. Overdrafts become structurally unlikely because bill payments draw from a dedicated account rather than the same pool you are spending from daily. Savings are protected at a separate institution where they cannot be accidentally depleted by discretionary spending.

Minimum Balance Requirements: The Hidden Opportunity Cost

Banks that waive monthly fees in exchange for maintaining a minimum balance — typically $1,000 to $2,500 — are not giving you something for free. The money sitting idle in a checking account is earning nothing while it could be earning 4 to 5 percent APY in a high-yield savings account. A $2,000 minimum balance requirement costs roughly $80 to $100 per year in foregone interest, on top of any fee you are already paying if the balance dips below the threshold.

How to fix it: Calculate the true cost of your current arrangement — the monthly fee plus the annual interest lost on the minimum balance. Compare that against a no-minimum account at an online bank with a high-yield savings option. In most cases the math strongly favors switching. Over ten years the difference compounds into thousands of dollars.

Forgotten Subscriptions and Recurring Payment Chaos

Subscriptions are a distinct category of banking drain — not a bank fee, but money disappearing monthly because no one is actively watching. The average person carries three to five subscriptions they have forgotten about or stopped using, costing $20 to $50 per month. Annual subscription renewals are worse: they arrive once, charge a lump sum, and are easily missed entirely.

How to fix it: Audit three months of statements and highlight every recurring charge regardless of size — most people find at least one subscription they had forgotten entirely. Cancel anything unused for 30 or more days. Route all subscriptions through one card so the complete list is visible in a single statement review. Set renewal reminders for annual charges 30 days in advance so you decide whether to keep or cancel before the charge posts.

Fees Most People Never Read Until It Is Too Late

Bank fee schedules are rarely read at account opening and almost never revisited. Most people learn about obscure fees by paying them. Common charges that appear without warning include paper statement fees ($1 to $5 per month), wire transfer fees ($15 to $30 per transfer), stop payment fees ($30 to $35 per check), returned item fees ($25 to $35 per item), and early account closure fees ($5 to $50 if you close within 90 to 180 days of opening).

How to fix it: Spend ten minutes reading your bank's fee schedule once — it is available on their website or in your account disclosures. Switch to e-statements immediately if you are paying for paper. Use ACH transfers instead of wires for non-urgent transfers since ACH is typically free while wires cost $15 to $30. If switching banks, keep the old account open for 60 days before closing to avoid early closure fees and ensure all autopay has fully transitioned.

The Real Annual Cost of Common Banking Mistakes

| Mistake | Estimated Annual Cost |

|---|---|

| Overdraft fees (3 to 4 per year) | $105 – $140 |

| Monthly maintenance fee | $144 |

| Out-of-network ATM fees (2 per week) | $120+ |

| Minimum balance opportunity cost | $80 – $100 |

| Forgotten subscriptions | $240 – $600 |

| Total | $689 – $1,100+ per year |

Over ten years, that is $6,900 to $11,000. If the same $800 annual savings were invested at a modest 6 percent return instead, the twenty-year value exceeds $31,000. These are not abstract numbers — they represent the real cost of banking arrangements most people have never consciously chosen and have never audited.

The fixes for most of these mistakes are not behavioral — they are structural. A no-fee bank eliminates the maintenance fee permanently. Account separation eliminates overdraft risk at the source. An automated savings transfer on payday removes the decision point entirely. Most of these problems solve once and stay solved.

Fixing individual mistakes is the tactic. Fixing the structure is the strategy.

Each mistake on this list has a one-time fix. But the reason they keep recurring is that the underlying account structure keeps creating the conditions for them. The complete Banking Systems framework covers account architecture, income routing, and automation setup so these mistakes become structurally unlikely from the start.

Explore the Banking Systems Hub →More From Multi-Account Budgeting System

How to Build a Banking System That Supports Your Budget — Structure your accounts around your budget so the two systems reinforce each other

The Modern Banking Stack — How to layer checking, savings, and apps into a complete banking infrastructure

How to Build a Banking System Where Overspending Is Structurally Impossible — Account architecture that makes the right behavior the default

The Psychology of Account Separation — Why physical boundaries beat mental accounting every time

The 4-Bucket Money System — Advanced multi-account strategy for complete financial visibility

Why You Need a Separate Account for Bills — The single most impactful account separation most people can make

You are here: How to Fix Banking Mistakes That Are Quietly Costing You Money

Resources

CFPB — Bank Account Consumer Tools and Resources

CFPB — Overdraft and NSF Fee Research Data

FDIC — Consumer Protection and Deposit Insurance Information

FDIC BankFind — Verify Institution Insurance Status

This article is part of the Banking Systems hub on PersonalOne — a complete framework for building the account structure and cash flow infrastructure that controls your financial outcomes automatically.

Frequently Asked Questions

Can I get overdraft fees refunded?

Sometimes. Call your bank, explain the situation, and ask for a courtesy refund. Banks will often waive one overdraft fee per year for customers in good standing with no recent overdrafts. This works best if it is your first occurrence in six months or more and you have a long account history with the institution. The refund is discretionary and not guaranteed, but it costs nothing to ask and frequently works.

How do I switch banks without missing payments?

Keep both accounts open for 60 days. Redirect direct deposits to the new account first to establish it as active. Then migrate autopay bills one at a time over several weeks, verifying each one confirms the updated payment method before moving the next. Maintain a buffer in the old account to catch any autopay that did not switch cleanly. Once two full billing cycles have cleared at the new account with no stragglers, close the old account in writing and request confirmation.

Are online banks as safe as traditional banks?

Yes, provided they are FDIC-insured. FDIC insurance protects deposits up to $250,000 per depositor per institution regardless of whether the bank has physical branches. Before opening any account, verify the institution's insurance status through the FDIC BankFind tool at fdic.gov.

What is the best way to track spending and avoid overdrafts?

The most effective approach is structural rather than behavioral — separate the money you are spending from the money already allocated to bills, so the balance in your spending account is your actual available number without any mental math required. Combine that with low-balance alerts set at $100 to $150 and you will catch potential shortfalls before they become overdraft fees.

Should I have multiple bank accounts?

For most people, yes — but with a specific purpose for each. A single checking account creates the structural conditions for most common banking mistakes. At minimum, a separate checking account for daily spending and a high-yield savings account at a different institution for your emergency fund eliminates the most common sources of overspending and savings depletion. The structure does more work than any amount of tracking or discipline applied to a single account.

Disclaimer: This content is for educational purposes only and does not constitute financial advice. Fee amounts vary by institution and change over time — always review current account agreements and fee schedules before opening new accounts or making banking changes. FDIC insurance covers up to $250,000 per depositor per institution — verify coverage directly with the FDIC before opening any account.