June 24, 2026

June, 2026

Home › Financial Automation › Banking Infrastructure for Automation › The Right Number of Bank Accounts for Full Automation

This article is part of the Banking Infrastructure for Automation cluster on PersonalOne. Use it to determine how many accounts your automated system actually needs — and when adding more accounts helps versus creates unnecessary complexity.

Don Briscoe is a financial systems strategist with 12+ years of experience helping people take control of their money. As the founder of PersonalOne.org, Don specializes in building financial systems for Millennials and Gen Z that work in real life, not just on paper.

What You Need to Know

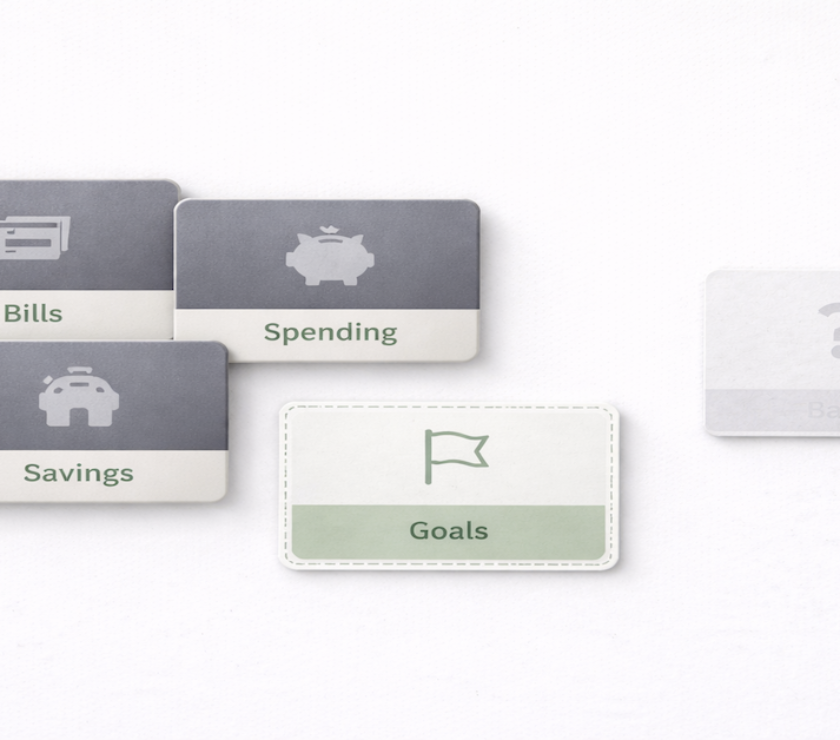

— The minimum viable automated system requires three accounts — bills checking, spending checking, and high-yield savings — and covers every essential financial category for most people.

— A fourth account for goals or sinking funds is worth adding once the core three are automated and running smoothly for at least 60 days.

— Beyond four accounts, each addition should solve a specific identified problem — not be added because more seems better or because a financial influencer recommended a certain number.

— The right number of accounts is the minimum that cleanly separates your money into its functional categories without requiring more management overhead than the separation saves.

— One account too few creates category confusion. One account too many creates management burden. The right number is the minimum that maintains clarity.

Personal finance content tends toward two extremes on account count. Some advice says to keep everything in one or two accounts for simplicity. Other advice prescribes seven, eight, or ten accounts with elaborate naming systems for every possible spending category. Both extremes miss the point.

The right number of accounts is determined by one criterion: how many functionally distinct categories of money do you actually have? Money that serves different purposes — obligations, spending, savings, investments — belongs in separate accounts. Money that serves the same purpose belongs in the same account. Adding accounts beyond that creates management overhead without adding clarity. Having too few creates the category confusion that account separation is designed to eliminate.

The right number of bank accounts for automation is not a fixed number for everyone. It is the minimum number that cleanly separates your money into its actual functional categories — and for most people that number is three to four. Here is how to determine the right number for your specific situation.

The Core Three: What Every Automated System Needs

Three accounts form the foundation that every automated system requires regardless of income level, financial complexity, or specific goals.

Account 1 — Bills Checking: Holds money for fixed monthly obligations. All autopay draws from here. Nothing else does. This account eliminates the confusion between money that is already committed and money that is genuinely available to spend.

Account 2 — Spending Checking: Holds only genuinely available discretionary money. Its balance is always accurate because nothing else draws from it. This account makes every spending decision simple: is there money here? Spend. Is there not? Stop.

Account 3 — High-Yield Savings: Holds the emergency fund and short-term savings goals at a separate institution. The transfer delay protects savings from impulsive access. The interest rate makes growth meaningful over time.

These three accounts handle every essential financial flow: income, bills, spending, and savings. For most people at most life stages, this is sufficient. The question of whether to add a fourth, fifth, or sixth account should be answered only after running the three-account system long enough to identify specific gaps it does not cover.

When a Fourth Account Is Worth Adding

The most common legitimate reason to add a fourth account is a goals fund that is distinct from the emergency fund. An emergency fund is not a goals account — it exists for genuine financial emergencies and should not be touched for vacation savings, a home down payment, or a car replacement fund. When those goals compete for space in the same savings account, the emergency fund gets raided for non-emergencies and the goals never fully fund because the emergency fund replenishment competes with goal contributions.

A separate goals account solves this by giving non-emergency savings their own dedicated space. Contributions are automated separately from the emergency fund contribution. The goals account can hold multiple purposes — most online banks allow sub-accounts or labeled vaults within one account — without requiring a separate account for each goal.

The fourth account is worth adding when: the emergency fund is fully funded and the savings contribution needs to redirect toward specific goals, when you have a specific medium-term goal (home purchase, car replacement) that needs dedicated tracking, or when the savings account balance has become unclear because emergency fund and goal savings are mixed together and you cannot tell which is which.

Accounts Five and Beyond: When More Helps and When It Hurts

Beyond four accounts, the case for each additional account needs to clear a higher bar. Each account adds management overhead: one more account to monitor, one more transfer to configure, one more balance to check during monthly review. That overhead is worth paying for genuine functional separation. It is not worth paying for theoretical organization that does not change actual behavior.

Accounts that are worth adding for specific situations:

Variable income buffer account: For freelancers, commission earners, and gig workers, a dedicated income buffer account that all variable income lands in before being distributed to the operational accounts is genuinely necessary. It smooths income variability and allows the rest of the system to operate on a consistent schedule. This is worth adding before the core three are stable for variable earners because the buffer is prerequisite infrastructure, not optional enhancement.

Business checking account: Anyone with meaningful self-employment income should separate business income and expenses from personal finances. A business checking account serves a legal and tax purpose in addition to organizational clarity. This is worth adding when self-employment income is consistent and significant enough to require its own tax treatment.

Tax reserve account: Self-employed earners who do not withhold taxes through payroll need a dedicated account for quarterly estimated tax payments. Without it, tax money gets spent and the quarterly bill becomes a crisis. A dedicated tax reserve that receives a percentage of every deposit and is never touched for anything other than taxes is worth adding alongside the business checking account.

Accounts that are rarely worth adding:

A separate account for every spending category: Grocery account, gas account, entertainment account. This level of separation creates more tracking work than it saves and effectively recreates the envelope budgeting system inside a banking architecture that was not designed for it. Sub-accounts or labeled vaults within a single savings account accomplish category separation for savings goals. For spending, the spending account with a low-balance alert is sufficient.

A separate account for each savings goal: One savings account with labeled sub-accounts or vaults handles multiple goals more efficiently than multiple accounts at different institutions. The organizational benefit of a separate account per goal rarely justifies the overhead of managing five separate savings accounts across potentially five different institutions.

The Account Count Decision Framework

When considering whether to add an account, apply four questions in order:

1. Does this money serve a genuinely different purpose than money in an existing account? If the answer is no — if the money is savings and you already have a savings account — the new account adds overhead without adding clarity. Use a sub-account or vault instead.

2. Is mixing this money with an existing account causing a specific, identified problem? If you cannot point to a concrete problem the new account solves — an overdraft caused by mixing, an inability to track a specific balance, a behavioral pattern you cannot break with existing structure — the problem may not actually exist. Adding accounts preemptively for theoretical organization is the most common source of unnecessary complexity.

3. Can you maintain this account with your existing monthly review process? Each account adds five to ten minutes to a monthly review. If the current three to four account review is already feeling like too much, adding a fifth account may reduce the quality of oversight across all accounts rather than improving it.

4. Have you run the current system for at least 60 days? Most gaps that seem like they require a new account resolve themselves once the existing system has been running long enough to reveal actual patterns. Resist adding accounts before the current system has produced real data about what is and is not working.

Start with three. Build from there when the need is clear.

The Financial Automation hub covers everything that goes on top of the account structure — budget automation, savings goals, debt payoff, and investment contributions that all connect to the infrastructure you build here.

Explore the Financial Automation Hub →More From Banking Infrastructure for Automation

The 3-Account System That Fixes Money Chaos — The complete framework: which accounts to open, where they live, and how money flows between them

Bills Account vs Spending Account: The Correct Setup — The exact configuration for each account and how to keep them from bleeding into each other

Where Your Paycheck Should Land First — The income landing account strategy that makes every automated transfer fire correctly

How to Build a Buffer Account That Prevents Overdrafts — The cash cushion that keeps automation running when timing does not align perfectly

Best Bank Features for Automation — What to look for in a bank before you build your automated system on top of it

How to Set Up Your Bank Accounts So Money Moves Without You — Step-by-step account configuration for a fully hands-off money flow

You are here: The Right Number of Bank Accounts for Full Automation

Why Your Checking Account Is Sabotaging Your Automation System — The specific checking account errors that silently break every automated system

Resources

CFPB — Bank Account Consumer Tools and Resources

FDIC — Consumer Protection and Deposit Insurance

FDIC — Deposit Insurance: How Your Accounts Are Protected

This article is part of the Financial Automation hub on PersonalOne — a complete framework for building financial systems that run without daily decisions.

Frequently Asked Questions

Does having multiple accounts hurt my credit score?

No. Checking and savings accounts do not appear on credit reports and have no impact on credit scores. Only credit accounts — credit cards, loans, lines of credit — affect credit scoring. Opening multiple bank accounts has zero credit score impact regardless of how many you open or how frequently.

What if I want to track multiple savings goals separately?

Most online savings institutions allow sub-accounts or labeled vaults within a single savings account. You can have one savings account with five labeled buckets — Emergency Fund, Vacation, Car, Home Down Payment, Annual Expenses — each tracking its own balance and contribution rate without opening five separate accounts. This approach accomplishes goal separation with a single account to manage.

Is five accounts too many?

Not inherently — it depends on whether each account serves a genuinely distinct purpose and whether you can maintain oversight across all of them with a manageable monthly review. A freelancer with bills checking, spending checking, income buffer, high-yield savings, and tax reserve has five accounts each serving a non-overlapping function. That is appropriate complexity. Five accounts where three serve overlapping savings purposes is unnecessary complexity.

Should I have a joint account with my partner and separate individual accounts?

The right joint versus individual account structure depends on how you and your partner have decided to manage shared versus individual finances. Common configurations include fully joint (all income and expenses managed from shared accounts), fully separate (each partner manages independently and transfers to cover shared expenses), and hybrid (joint accounts for shared bills and savings, individual spending accounts). The automation principles in this cluster apply to any of these configurations — the account count just reflects the structure you have agreed on together.

Disclaimer: This content is for educational purposes only and does not constitute financial advice. The right account structure varies by individual financial situation. Always verify current account terms, fees, and features with your bank or credit union before opening new accounts.