Published: February 27, 2026

Home › Banking Systems › The 3-Account System › How Many Bank Accounts Should You Really Have?

About the Author

Don Briscoe is a financial systems coach with more than 12 years of experience helping Millennials and Gen Z escape the paycheck-to-paycheck cycle. His framework-first approach focuses on building financial infrastructure that works automatically — less willpower, more systems. He founded PersonalOne.org to make structured, honest financial education free and accessible.

TL;DR — The Answer Depends on You

There is no universal right number of bank accounts. The answer depends on your income complexity, financial goals, spending patterns, and how much structure you need.

The baseline for most people: Three accounts — bills checking, spending checking, high-yield savings.

This guide covers:

— The 3-account foundation that works for 80% of people

— When to add a 4th, 5th, or 6th account

— Life stage considerations: single, married, family, retirement

— Signs you have too many accounts

— A decision framework for your specific situation

Search "how many bank accounts should I have" and you will find answers ranging from one to fifteen.

Personal finance content creators show off their 8-account systems. Your parents insist one checking account is plenty. Your financially sharp friend swears by seven specialized accounts.

They are all right — for their specific situation.

The number of accounts you need depends on factors most articles ignore: your income consistency, whether you are married or single, if you have kids, whether you own a home, your comfort level with complexity, and what financial problems you are actually trying to solve. This guide gives you a decision framework, not a one-size-fits-all answer.

Account Structure That Actually Works

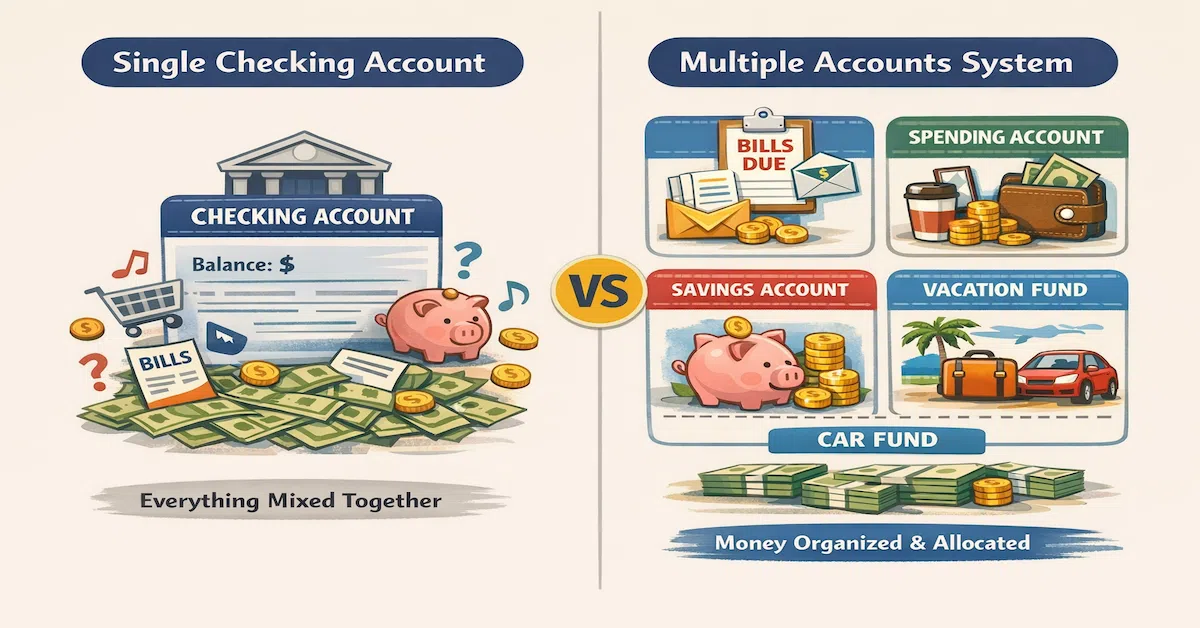

Deciding how many accounts you need starts with understanding what each account is supposed to do. The 3-account banking system is the foundation most people should build from — a clean separation of bills, spending, and savings that runs on autopilot. More accounts are only added when they solve a specific problem this foundation cannot.

The 3-Account Baseline (Works for 80% of People)

If you are asking how many accounts you need, start here. Three accounts create enough separation to eliminate financial stress without adding management overhead.

Account #1: Bills Checking

Purpose: Fixed monthly expenses only.

This account handles rent or mortgage, utilities, insurance, car payments, subscriptions, and any other predictable recurring bills. Money flows in automatically on payday. Bills autopay out throughout the month. You rarely touch it.

Why it matters: Separating bills from spending means your spending account balance is always accurate. No mental math required.

Account #2: Spending Checking

Purpose: Daily variable expenses.

Groceries, gas, restaurants, entertainment, clothing, personal care — anything that is not a fixed bill or designated savings goes here. When the balance gets low, you know to cut back. When money is there, you spend without guilt.

Why it matters: Physical separation eliminates the "can I afford this?" paralysis. If money is in spending, yes. If not, no.

Account #3: High-Yield Savings

Purpose: Emergency fund and short-term goals.

This should be at an online bank earning meaningful interest — not your regular bank's near-zero savings rate. Money transfers here automatically on payday and is rarely withdrawn except for actual emergencies or planned goal spending.

Why it matters: Out of sight, out of mind. Money you do not see in checking stays saved. The interest you earn compounds over time in a way a brick-and-mortar savings account never will.

Is the 3-Account System Enough for You?

Answer YES if:

— Your bills are consistent month to month

— You do not have large irregular expenses like annual insurance or property taxes

— You are not saving for multiple specific goals simultaneously

— You prefer simplicity over optimization

— Your income is predictable (W-2 employee)

If you answered yes to 3 or more of these, stop at 3 accounts. Do not add complexity you do not need.

When to Add a 4th Account: Irregular Expenses

The 3-account system works well until December arrives and you realize you need $1,500 for car insurance, holiday gifts, and annual subscriptions you forgot about.

Add a 4th account if you have: annual or semi-annual bills (car registration, property taxes, insurance premiums), predictable irregular expenses (holiday spending, birthday gifts, back-to-school costs), or quarterly bills that do not fit monthly budgeting.

Account #4: Irregular Expenses Account

Calculate your total annual irregular expenses. As an example: car insurance at $720 per year, car registration at $200, a streaming or membership renewal at $140, holiday spending at $800, and birthday gifts at $300 comes to roughly $2,160 annually — or $180 per month. Transfer that amount monthly to this account. When the irregular expense hits, the money is already there. No scrambling, no emergency fund raids.

Life Stage: Homeowners

If you own a home, a 4th account becomes essential. Add home maintenance and repair savings to irregular expenses. A common rule of thumb: save 1% of home value annually for maintenance. A $300,000 home means setting aside roughly $250 per month to the irregular expenses account.

When to Add a 5th Account: Multiple Savings Goals

Your emergency fund is built. Now you are saving for a house down payment while also building a car replacement fund. Mixing these in one account creates confusion about what money is allocated where.

Add a 5th account if you are: saving for multiple distinct goals (house, car, vacation, wedding), building wealth beyond your emergency fund, or accumulating a buffer for future business expenses.

Account #5: Goal-Specific Savings

Three approaches work here. One savings account with named mental buckets is simpler but requires tracking. Multiple savings sub-accounts — which many online banks offer free — give each goal its own visible balance. A dedicated account at a separate bank creates the strongest psychological boundary for large, long-horizon goals.

An example structure: Account 3 holds the emergency fund — fully funded, rarely touched. Account 5a holds the house down payment contribution. Account 5b accumulates the car replacement fund. Account 5c holds vacation savings. Each balance reflects exactly where that goal stands.

Life Stage: Planning Major Purchases

If you are two to five years from a major purchase, separate that savings from your emergency fund. The emergency fund stays liquid and untouched. Goal savings grows specifically for the planned purchase. This separation prevents the common mistake of borrowing from emergency funds for non-emergencies.

When to Add a 6th Account: Business or Side Hustle

The moment you earn income outside your W-2 job, separate business and personal finances immediately.

Add a 6th account if you: freelance or do contract work, run a side business, earn 1099 income, or have rental property income.

Account #6: Business Checking

Mixing business and personal income creates tax problems, obscures profit and loss tracking, and makes bookkeeping unreliable. Commingled funds also raise flags in the event of an IRS audit. The structure is straightforward: all business income deposits here, all business expenses pay from here, 25–30% gets set aside in a sub-account for estimated taxes, and you pay yourself a regular transfer to personal checking.

Tax Note: Self-Employment Income

If you earn self-employment income — even $500 per month from a side project — open a dedicated business checking account immediately. Deposit all business income there, set aside 30% for taxes, and transfer the remaining profit to personal checking. This single separation prevents most of the tax and bookkeeping problems freelancers encounter.

When You Have Too Many Accounts

More accounts produce diminishing returns. Past six or seven, you are adding complexity without meaningful benefit.

Signs you have too many: You forget accounts exist and discover them months later. You cannot explain what each account is for. Transfers between accounts happen weekly or daily. You spend more time managing accounts than they save in mental clarity. Multiple accounts serve essentially the same purpose. You are opening accounts just in case without a clear function.

The fix: Consolidate accounts with overlapping purposes. Merge multiple general savings accounts into one with named sub-buckets. Close forgotten accounts. Simplify back to the essentials that actually solve your financial problems.

Life Stage Considerations

Your ideal number of accounts changes as your financial life evolves.

Single, Early Career (Age 22–30)

Recommended: 3 accounts. Bills checking, spending checking, high-yield savings for building the emergency fund. Focus: simplicity and habit building.

Single, Established Career (Age 30–40)

Recommended: 4–5 accounts. Bills checking, spending checking, emergency fund (fully funded), goal savings, and an irregular expenses account if a homeowner. Focus: wealth building and major purchase preparation.

Married, No Kids

Recommended: 4–6 accounts. Joint bills checking, joint spending checking or individual spending accounts, joint emergency fund, joint goal savings, and optionally individual discretionary accounts. Focus: coordination and shared goals.

Married with Kids

Recommended: 5–7 accounts. Joint bills checking, joint spending checking, emergency fund (six months minimum), irregular expenses for childcare and seasonal costs, kids' savings or college fund, home maintenance if a homeowner, and optionally individual spending accounts for each spouse. Focus: stability and future planning.

Retirement

Recommended: 3–4 accounts. Bills checking for fixed expenses, spending checking for discretionary and travel, emergency savings, and optionally a healthcare savings account for Medicare gaps or long-term care costs. Focus: simplification and income distribution.

The Decision Framework

Step 1: Start With the 3-Account Baseline

Bills checking + spending checking + high-yield savings. This foundation works for 80% of people. Only add accounts if they solve a specific problem this structure cannot.

Step 2: Add Account #4 If You Answer YES

"Do I have irregular expenses that surprise me annually or cause me to raid savings?" Examples: annual insurance, property taxes, holiday spending, car registration.

YES = Add an irregular expenses account.

Step 3: Add Account #5 If You Answer YES

"Am I saving for multiple specific goals beyond my emergency fund?" Examples: house down payment, car replacement, wedding, major travel.

YES = Add goal-specific savings account(s).

Step 4: Add Account #6 If You Answer YES

"Do I earn income outside of W-2 employment?" Examples: freelancing, side business, contract work, rental property.

YES = Add a business checking account. Non-negotiable.

Step 5: Stop Adding When

You cannot clearly articulate what each account is for, or you are managing accounts more than they are managing your money.

Aim for clarity, not complexity. The best system is the simplest one that solves your actual problems.

Joint vs. Individual Accounts for Couples

For couples, account quantity also depends on financial philosophy. None of the following structures is right or wrong — match the structure to your relationship dynamic and communication style.

Fully joint (4–5 accounts): joint bills, joint spending, joint savings, joint irregular expenses. Works best when both partners have similar spending styles and want full financial transparency.

Hybrid (6–8 accounts): joint bills, joint household spending, joint savings, individual spending accounts for each partner, joint irregular expenses. Works best when partners want shared responsibility alongside personal autonomy.

Mostly separate (7–10 accounts): joint bills only, with each partner maintaining independent checking, savings, and goal accounts. Works best in second marriages, situations with significant income disparity, or when both partners strongly prefer financial independence.

Build the Complete Banking Architecture

Account quantity is one decision. Structure, automation, and flow are the rest. The PersonalOne guide on how to structure your bank accounts covers the full framework — how each account connects, how money moves between them automatically, and how to build a system that runs without daily management. Free, no signup required.

Framework-first. Less willpower. More infrastructure.

Frequently Asked Questions

Will having multiple bank accounts hurt my credit score?

No. Checking and savings accounts do not appear on credit reports and have zero impact on your credit score. Only credit accounts — credit cards, loans, lines of credit — affect your score. You can open as many bank accounts as you need without any credit consequences.

Should all my accounts be at the same bank?

Not necessarily. Bills and spending checking accounts benefit from being at the same bank for instant internal transfers. Savings, however, should be wherever the interest rate is highest — often an online bank paying significantly more than a traditional branch. Business accounts may need to be at a bank with physical locations if you deposit cash regularly.

How do I manage multiple accounts without it becoming overwhelming?

Automation handles the heavy lifting. Set up automatic transfers on payday so each account funds itself. Use a financial aggregator to view all accounts in a single dashboard. Check balances weekly at first, then monthly once the system is stable. The point of the structure is that the accounts run themselves — if you are actively managing them daily, the system is not set up correctly.

What if my spouse wants fewer accounts than I think we need?

Start with the 3-account baseline you both agree on. Run it for two to three months. If problems emerge — irregular expenses creating surprises, savings goals getting mixed together — propose adding one specific account to solve that one problem. Add accounts incrementally with mutual agreement rather than implementing a complex system all at once.

Can I start with one account and add more later?

Absolutely. Many people start with one checking account, add savings when they begin building an emergency fund, then add a bills account when they realize the separation would reduce stress. There is no requirement to implement a complete system immediately. Evolve your structure as your financial life becomes more complex.

Is there a maximum number of accounts I should never exceed?

There is no hard maximum, but practically speaking most people see no meaningful benefit past eight to ten accounts total. If you are managing more than that, you are almost certainly adding complexity without solving new problems. Consolidate accounts that serve overlapping purposes and simplify.

Should I count investment accounts in this total?

No. This framework covers checking and savings accounts for daily money management. Investment accounts — 401(k), IRA, brokerage — serve a different function and are not part of your operational account structure. Keep them separate from this count.

What if my bank charges fees for multiple accounts?

Switch banks. Free checking and savings accounts are standard at online banks and most credit unions. Your account structure should not cost you money in maintenance fees. If your current bank charges for additional accounts, you are subsidizing outdated infrastructure instead of building a functional financial system.

How do I know if I need another account or if I am overcomplicating things?

Add an account only when you can clearly state what specific problem it solves that your current accounts cannot address. If you cannot articulate the problem, you do not need the account. A useful test: explain to someone else why the account is necessary. If you cannot explain it simply, the case is not strong enough.

Should kids have their own savings accounts?

Yes, if the goal is to teach money management. A savings account in a child's name with you as custodian gives them visibility into saving and how interest works over time. This does not count against your personal account structure — it is an educational tool operating separately. A natural starting point is when children begin receiving allowance or earning money from gifts or chores.

Resources

FDIC: How to Make the Most of Your Bank Accounts — Federal guidance on account types, deposit insurance, and how to evaluate banking options.

CFPB: What Is a Checking Account? — Official explanation of checking account features, fees, and consumer protections.

CFPB: What Is a Savings Account? — How savings accounts work, what to look for in interest rates, and how they differ from checking.

Disclaimer: The content on PersonalOne.org is for informational and educational purposes only and does not constitute financial, legal, or tax advice. Optimal account structure depends on individual income sources, expense patterns, financial goals, and personal preferences. Before making significant changes to your banking setup, consider your complete financial situation. PersonalOne provides educational content and does not offer personalized financial planning services.