April, 2026

Home › Financial Stability › Financial Shock Absorption › How to Cut Expenses Fast

What You Need to Know

— When income drops suddenly, the goal is to reduce monthly spending to survival expenses only — typically 40–60% below normal spending for most households

— There are three tiers of cuts: immediate (cancel or pause today), short-term (reduce within the week), and negotiated (contact providers for hardship rates)

— Most households can cut $400–$800/month within 48 hours by eliminating subscriptions, pausing non-essential services, and switching to home cooking

— Fixed expenses like rent, car payments, and insurance require direct contact with providers to reduce — they do not reduce automatically

— Every dollar of monthly expenses you reduce increases your cash runway — track the cumulative impact of each cut to maintain momentum

Knowing how to cut expenses fast when income drops is not about finding the cheapest option for every purchase — it is about moving systematically through three tiers of expense reduction in order of speed and impact. The financial shock absorption strategy for expense reduction works fastest when you treat spending cuts as a triage operation: address the biggest-impact, fastest-to-execute cuts first rather than spending hours optimizing small variable expenses. The complete framework for absorbing financial shocks is in the Financial Shock Absorption guide.

The goal of emergency budget cuts is to arrive at your bare-bones monthly number — the minimum you need to keep a roof over your head, your car operational, your utilities on, and your minimum debt payments current. Everything above that number is a candidate for immediate reduction. How you structure this reduction in the context of your full financial system is covered in the financial stability guide.

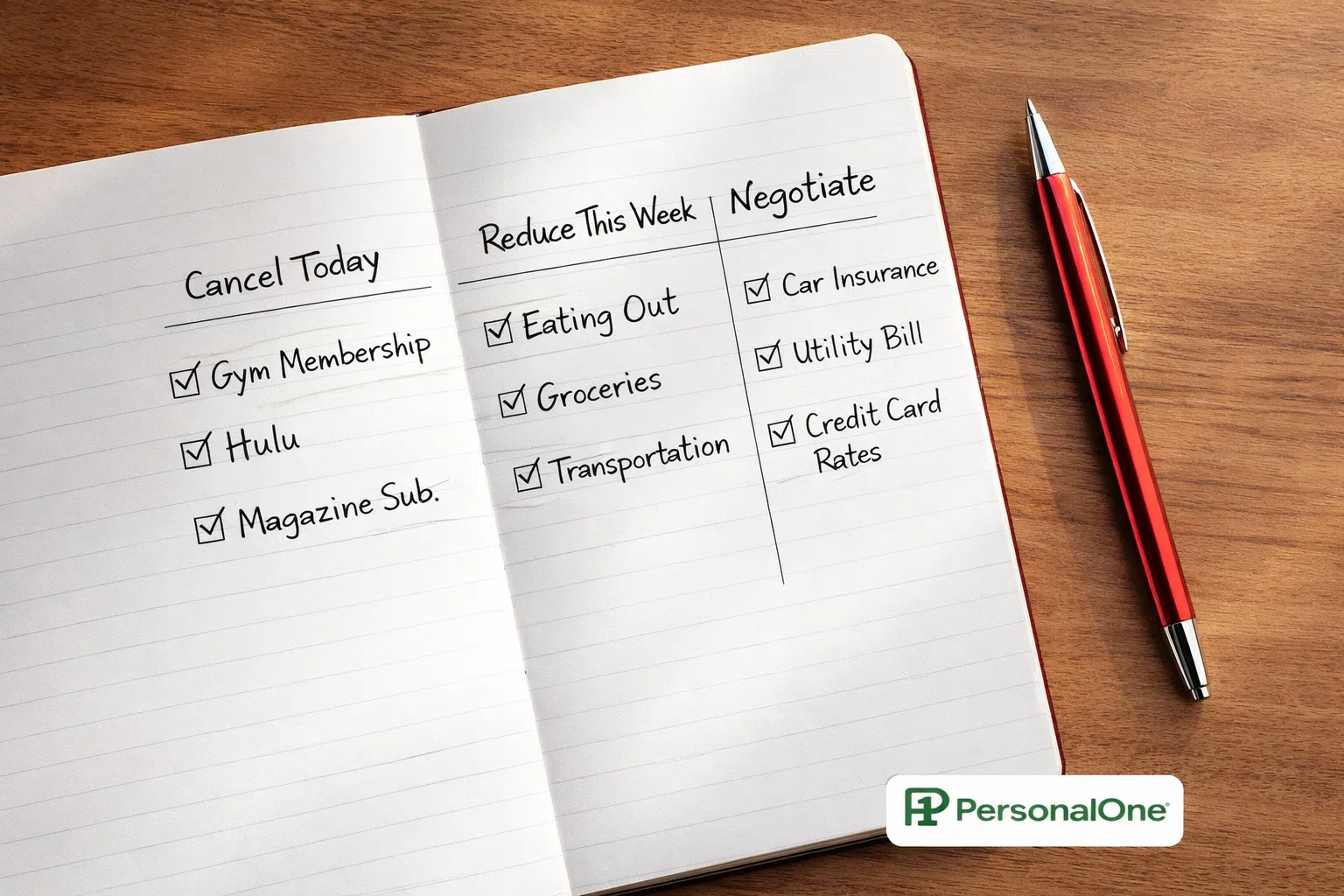

Tier 1: Immediate Cuts — Execute Today

These are expenses you can eliminate within 24 hours with no negotiation and no consequence beyond losing access to the service. Execute every applicable cut on this list before doing anything else.

Streaming and entertainment subscriptions. Netflix, Hulu, Disney+, Spotify, Apple TV+, YouTube Premium — cancel all of them. Most allow you to cancel and restart without losing your account history. Total savings: $50–$150/month depending on how many you carry.

Software subscriptions and app purchases. Adobe Creative Suite, Microsoft 365 personal, gaming subscriptions, cloud storage upgrades above free tiers, premium app subscriptions. Cancel any that are not essential to income-generating work. Total savings: $30–$100/month.

Gym and fitness memberships. Most gym contracts have hardship cancellation clauses or allow freeze rather than full cancellation. Call or cancel online. If a contract requires a cancellation fee, weigh the fee against several months of continued payments. Total savings: $25–$80/month.

Dining out completely. Restaurant meals, coffee shop purchases, takeout, and delivery apps stop immediately. The average household spends $300–$600/month on dining out. Switching to home cooking does not require elaborate meal planning — simple, inexpensive meals (eggs, beans, rice, pasta, seasonal vegetables) cover nutrition at a fraction of the cost.

Tier 2: Short-Term Reductions — Execute This Week

Grocery spending. Reduce by 30–40% by buying store-brand products exclusively, planning meals around what is on sale, and eliminating convenience items. A household of two can eat nutritiously on $200–$300/month with intentional shopping. Total savings from previous baseline: $100–$200/month.

Transportation costs. Combine errands into single trips to reduce fuel consumption. Pause any toll passes or transit cards that cover non-essential commutes. If you have two vehicles, consider temporarily suspending registration and insurance on the less essential one. Total savings: $50–$150/month.

Utilities. Reduce electricity consumption by adjusting the thermostat, unplugging unused devices, and eliminating energy-intensive habits. Switch to the most basic internet plan available — internet providers will often temporarily reduce your rate to avoid cancellation if you call and explain the situation. Total savings: $40–$100/month.

Tier 3: Negotiated Reductions — Contact Providers Directly

Car insurance. Call your insurer and ask about hardship rate reductions, reduced-mileage discounts (if driving less during job search), or increasing deductibles temporarily to reduce premiums. Most insurers have options that are not advertised. Total potential savings: $30–$80/month.

Credit card minimum payments. Credit card issuers have hardship programs that reduce interest rates and minimum payments temporarily during documented financial hardship. Call the number on the back of your card and ask for the hardship department specifically. This does not close the account and does not automatically impact your credit score if the agreement is documented.

Phone plans. Most major carriers have emergency or reduced plans at $25–$40/month that provide sufficient service for job searching. Call and ask to be moved to the lowest available plan. Total savings from standard plans: $40–$80/month.

Every dollar cut extends your runway. Start with Tier 1 today.

The complete framework for absorbing financial shocks — including what to do with the money you save and how to prioritize bills — is in the Financial Shock Absorption guide.

Explore Financial Shock Absorption →Resources

Official Sources

CFPB — Budgeting and Spending Tools — Consumer Financial Protection Bureau tools for building an emergency budget, tracking spending, and identifying categories where reduction is possible during income disruption.

BLS — Consumer Expenditure Survey — Bureau of Labor Statistics data on average household spending by category — useful for benchmarking your own spending and identifying where your household is above average in categories that can be reduced.

Return to the financial stability guide for the complete system this cluster is part of.

Frequently Asked Questions

What is the fastest way to cut $500 from monthly expenses?

Cancel all streaming and entertainment subscriptions ($50–$150), stop all dining out and switch to home cooking ($200–$300), call your phone carrier and downgrade to the cheapest plan ($40–$80), and cancel any gym or fitness membership ($25–$80). These four actions can be executed within 24 hours and typically total $300–$600 in monthly savings without requiring any negotiation or provider contact beyond phone calls.

Should I reduce my 401(k) contributions to free up cash?

Do not reduce 401(k) contributions below the employer match threshold — the match is an immediate return that no expense reduction can replicate. If you need additional cash flow beyond what Tier 1–3 cuts produce, reducing above-match voluntary contributions temporarily is a lower-harm option than carrying credit card debt at high interest. Restore contributions as soon as income stabilizes.

Can I temporarily pause my car payment?

Contact your auto lender directly and ask about payment deferral programs. Most lenders will allow one to three months of deferred payments during documented financial hardship, with the deferred amount added to the end of the loan term. This does not eliminate the payment — it moves it. Confirm any deferral agreement in writing before missing a scheduled payment, as unauthorized missed payments are reported to credit bureaus.

Disclaimer: This article is for informational and educational purposes only. Subscription terms, provider hardship programs, and insurance options vary. Verify current details directly with each provider before making changes.