April, 2026

Home › Financial Stability › Financial Shock Absorption › Handle a Financial Emergency Without Debt

What You Need to Know

— The default response to a financial emergency — putting it on a credit card — converts a one-time expense into a recurring debt cost that can persist for months or years

— Most financial emergencies have non-debt funding options that most people do not explore before reaching for a credit card

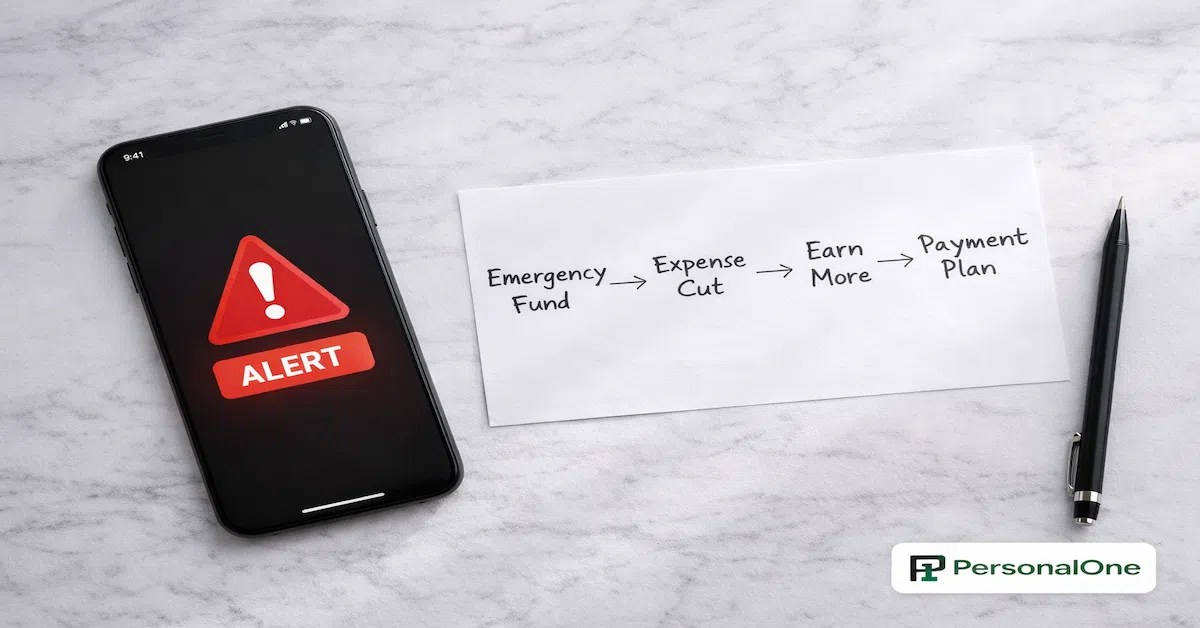

— The financial emergency response sequence is: emergency fund first, expense reduction second, income acceleration third, payment plans fourth, credit as last resort

— Negotiating a payment plan directly with a provider almost always produces better terms than financing through a credit card at 20–30% APR

— The goal is to survive the emergency without creating a new financial burden that compounds the recovery timeline

Knowing how to handle a financial emergency without going into debt requires understanding the specific sequence of funding options available before a credit card becomes the answer. Most people skip directly to credit because it is the fastest and most familiar option — but it is also the most expensive over time. The financial emergency response plan works through four non-debt options before credit is considered. This is the core of the financial shock absorption strategy — and the complete framework is in the Financial Shock Absorption guide.

Surviving a financial crisis without debt is not about having more money — it is about having a system that responds in the right order. The difference between a financial emergency that resolves in 30 days and one that creates 18 months of credit card debt is almost always whether the right response sequence was followed. The broader financial stability system that prevents financial emergencies from becoming financial crises is in the financial stability guide.

Option 1: Emergency Fund

If you have an emergency fund, a financial emergency is exactly what it exists for. Use it. Deploy it without guilt or hesitation for the purpose it was built for. A $600 car repair covered by your emergency fund costs $600. The same repair on a credit card at 24% APR paid over 12 months costs approximately $670 — an additional $70 in interest on a repair that was already expensive. The cost difference compounds significantly for larger emergency expenses.

After the emergency is resolved, replenish the emergency fund before any other financial priority. The emergency fund is not fully functional at a depleted balance — restore it to its target as quickly as possible by temporarily redirecting discretionary spending to replenishment.

Option 2: Immediate Expense Reduction to Free Cash

For a one-time emergency expense that can wait 2–4 weeks, a rapid expense reduction campaign can generate the needed cash from your existing income without debt. Cancel subscriptions, eliminate discretionary spending entirely for one pay cycle, and redirect the freed cash to cover the expense. This is slower than a credit card but costs nothing in interest and does not impact your credit utilization.

The specific amount you can generate through rapid expense reduction depends on your current discretionary spending level. For households spending $300–$600/month on dining out and entertainment, a 30-day spending freeze can generate significant cash toward a moderate emergency expense.

Option 3: Income Acceleration

For emergencies that allow 1–3 weeks of lead time, a short income sprint — selling unused items, taking on extra work hours, completing a quick freelance project — can generate the funds needed without debt. Online selling platforms allow you to list and sell items within days. Gig work can produce additional income within a week in most markets. Overtime hours, if available, generate additional pay within the current pay cycle.

Income acceleration is most effective for mid-size emergencies ($300–$1,500) where the timeline allows for collection before the expense must be paid. Combine it with expense reduction for faster results.

Option 4: Payment Plans Directly With the Provider

Before using a credit card for a large emergency expense, contact the provider directly and ask about payment plans. Medical providers, auto repair shops, dental practices, and home repair contractors routinely offer zero-interest or low-interest payment plans to customers who ask. A hospital bill of $2,000 on a payment plan at 0% over 12 months costs $167/month and $0 in interest. The same bill on a credit card at 24% APR paid over 12 months costs approximately $190/month and $280 in interest.

Hospital and medical billing departments have financial assistance and charity care programs for patients experiencing hardship — these are available regardless of insurance status and can significantly reduce or eliminate large medical bills for eligible patients. Ask specifically about financial assistance programs at the billing department, not the front desk.

When Credit Is the Right Answer

Credit is appropriate for financial emergencies when: the emergency cannot wait, the amount exceeds what the other three options can cover in the available time, and you have a specific repayment plan in place before you charge. Using a 0% APR introductory credit card for an emergency expense with a plan to pay it off before the promotional period ends is a legitimate tool. Using a high-interest card with no repayment plan converts the emergency into a long-term debt problem.

The right sequence makes the difference between a resolved emergency and a debt spiral.

The complete framework for managing financial shocks of all sizes is in the Financial Shock Absorption guide.

Explore Financial Shock Absorption →Resources

Official Sources

CFPB — Savings Tools and Resources — Consumer Financial Protection Bureau guidance on building and deploying emergency savings, how to structure cash reserves for maximum protection, and how to recover after using emergency funds.

FDIC — Consumer Resource Center — FDIC guidance on FDIC-insured savings products appropriate for emergency funds, how to structure savings across accounts for full coverage, and deposit insurance limits.

Return to the financial stability guide for the complete system this cluster is part of.

Frequently Asked Questions

What counts as a financial emergency versus a regular expense I forgot to plan for?

A financial emergency is an unexpected, necessary expense that could not have been reasonably anticipated and budgeted for in advance. Car breakdown: emergency. Annual car registration: not an emergency — it is a predictable expense that should be in a sinking fund. Medical emergency: emergency. Routine dental cleaning: predictable, should be in a sinking fund. The distinction matters because using your emergency fund for predictable expenses depletes the protection you need for genuine emergencies.

Should I take a 401(k) loan to cover a financial emergency?

A 401(k) loan should be considered before high-interest credit card debt but after all other options are exhausted. The risks: if you leave your employer while the loan is outstanding, the full balance is due immediately or becomes a taxable distribution subject to penalties. The loan also removes the borrowed amount from tax-advantaged compounding during the repayment period. Use it only for large emergencies where no other option exists.

Is it ever worth using a payday loan for a financial emergency?

No. Payday loans carry annual percentage rates of 300–600% in many states and create a debt trap that is extremely difficult to escape. The Consumer Financial Protection Bureau and Federal Trade Commission both provide detailed guidance on the risks of payday loans. Before using a payday loan, exhaust every option listed in this article, contact the expense provider about a payment plan, and explore local emergency assistance programs through 211.org.

Disclaimer: This article is for informational and educational purposes only. Financial product terms, assistance program eligibility, and creditor policies vary. Verify current details with each provider.