April 27, 2026

Home › Financial Stability › Expense Compression Strategy & Cost Control › Compress Expenses Fast

What You Need to Know

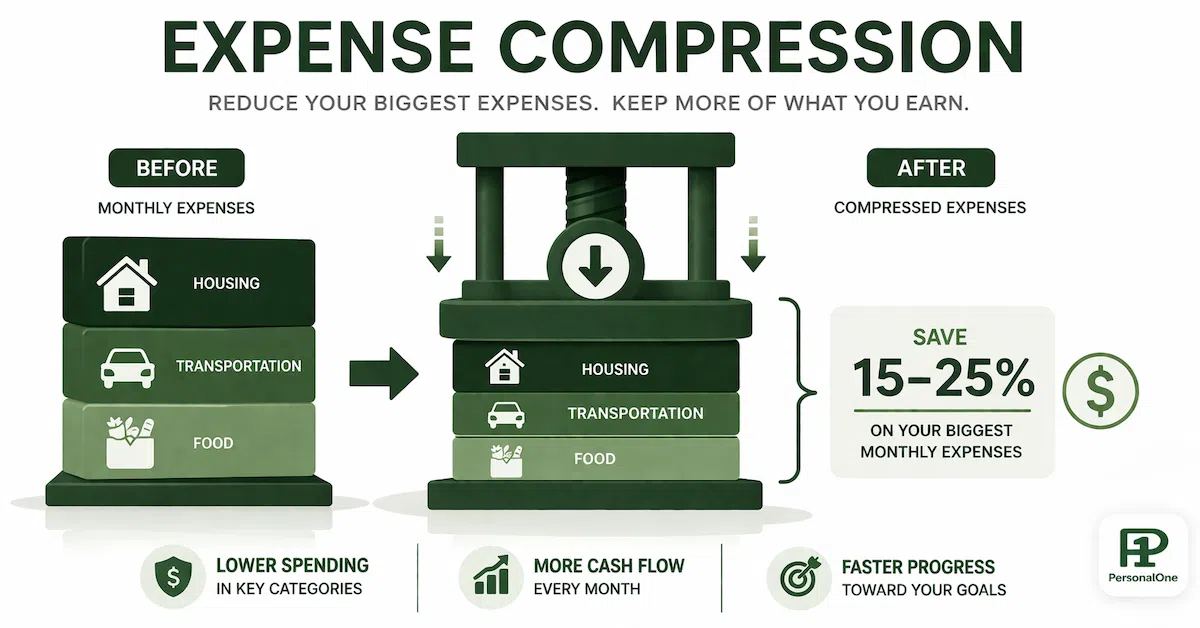

— Expense compression focuses on reducing spending in high-impact categories (housing, transportation, food) where small percentage cuts create large absolute savings

— Effective compression preserves quality of life by targeting waste, inefficiency, and low-value spending rather than eliminating categories entirely

— The average household can reduce expenses 15-25% within 30-90 days by addressing subscription bloat, housing inefficiency, and transportation costs without lifestyle disruption

— Compression works best as temporary intervention during financial emergencies or debt payoff rather than permanent extreme frugality

— Sustainable expense reduction requires distinguishing between value-aligned spending and habitual spending that provides minimal satisfaction

Expense compression is systematic reduction of spending through eliminating waste and inefficiency while preserving quality of life. This distinguishes compression from generic cost cutting, which often reduces expenses by eliminating value indiscriminately. Someone cutting $500 monthly by canceling gym membership, meal prepping exclusively, and eliminating social spending has reduced expenses but potentially damaged health, convenience, and relationships. Someone cutting $500 monthly by negotiating insurance rates, eliminating unused subscriptions, and optimizing grocery spending has compressed expenses without lifestyle deterioration.

The compression framework targets three categories of spending: waste (paying for unused or underutilized services), inefficiency (paying premium prices for commodity services), and low-value spending (expenses providing minimal satisfaction relative to cost). A $120 monthly gym membership used twice equals $60 per visit—waste. Paying $150 monthly for cable television when streaming costs $30 monthly for equivalent content—inefficiency. Spending $200 monthly on convenience foods when meal prep provides equal satisfaction at $80 monthly—potentially low-value depending on time constraints and cooking enjoyment.

Understanding expense compression strategy and cost control provides the systematic framework for identifying compression opportunities across all spending categories.

High-Impact Expense Categories for Compression

Housing costs and occupancy efficiency. Housing typically consumes 25-35% of income according to Bureau of Labor Statistics data, making it highest-impact compression target. Households paying $2,000 monthly for housing cutting 10% through compression save $200 monthly—same absolute savings as eliminating $200 in miscellaneous spending but requiring single decision rather than dozens of small cuts.

Compression approaches for housing include: negotiating rent renewal (landlords often reduce rent 5-10% when presented with comparable lower-priced units rather than face vacancy costs), adding roommate to split costs (cutting $1,800 rent to $900 per person), relocating to lower-cost unit during lease renewal (downgrading from $1,800 to $1,400 saves $400 monthly with minimal lifestyle impact if space reduction is modest), or refinancing mortgage to lower rate (reducing $2,200 monthly payment to $1,950 through rate reduction from 6% to 4.5%).

Housing compression timeline varies significantly. Adding roommate can reduce costs within 30-60 days. Relocating requires lease expiration or breaking lease with penalties. Mortgage refinancing requires 30-60 days for closing. Rent negotiation attempts during renewal or when presenting market data showing overpricing.

Transportation and vehicle costs. Transportation averages 15-20% of household spending, making it second highest-impact category. Households with $600 monthly car payment plus $200 insurance plus $150 gas spend $950 monthly on single vehicle. Compression creates $200-400 monthly savings through strategic changes rather than eliminating transportation entirely.

Compression approaches include: selling financed vehicle and buying used car with cash (eliminates $600 payment, potentially reduces insurance $50-100 monthly through lower coverage requirements on older vehicle), refinancing auto loan to lower rate (reducing payment $50-100 monthly), shopping insurance annually (most drivers overpay $200-500 annually by never comparing rates), carpooling or transit for commute (cutting gas costs 50-75%), and reducing comprehensive coverage on vehicles worth under $5,000 (saves $30-80 monthly when emergency fund covers replacement cost).

Transportation compression requires evaluating total cost of ownership rather than focusing exclusively on payment amount. A $400 monthly payment on reliable newer vehicle costing $150 monthly maintenance may be cheaper than $0 payment on paid-off older vehicle requiring $300 monthly repairs. The compression opportunity is strategic vehicle selection at appropriate price point, not necessarily eliminating payments entirely.

Food spending and grocery optimization. Food spending (groceries plus dining) averages 10-15% of household budgets but shows highest variance in efficiency. Households spending $1,200 monthly on food can often compress to $700-800 monthly through eliminating waste and optimizing purchasing without reducing food quality or variety.

Compression approaches include: eliminating food waste (average household wastes 30-40% of purchased food according to USDA data, representing $200-400 monthly for household spending $1,000 on food), meal planning to reduce impulse purchases (reduces grocery costs 15-25% by eliminating duplicate purchases and forgotten ingredients), buying store brands for commodity items (saves 20-40% on functionally identical products), reducing restaurant frequency (cutting dining from 12 times monthly at $40 per meal to 6 times monthly saves $240 without eliminating dining entirely), and strategic use of wholesale clubs for high-consumption staples.

Food compression preserves satisfaction by maintaining food quality and variety while eliminating inefficiency. Switching from brand-name pasta to store-brand pasta at 40% lower cost creates identical meal at lower price. Reducing restaurant meals from 12 to 6 monthly maintains dining experience while cutting costs 50%. Meal planning prevents waste without requiring extreme couponing or bargain hunting.

Expense compression in housing, transportation, and food creates $500-1,000 monthly savings for most households.

These high-impact categories are part of comprehensive financial stability framework covering income, expenses, and emergency reserves.

Build Financial Stability →Subscription and Recurring Charge Compression

Identifying subscription bloat. Average household maintains 8-12 recurring subscriptions according to consumer spending data, many unused or underutilized. Subscription bloat accumulates gradually—individual $10-15 monthly charges feel insignificant during signup but compound to $200-400 monthly total. Annual review of all recurring charges typically reveals 3-5 subscriptions providing minimal value relative to cost.

Compression process: export 90 days of bank and credit card transactions, filter for recurring charges, categorize by value (essential, valuable, occasional, unused), cancel unused and occasional subscriptions, evaluate whether valuable subscriptions can be replaced with free alternatives or shared among household members. A household paying for Netflix ($15), Hulu ($12), Disney+ ($11), HBO Max ($15), Apple TV ($10), and Paramount+ ($10) spends $73 monthly on streaming—compressing to two services saves $40-50 monthly with minimal content reduction.

Insurance optimization without coverage reduction. Insurance premiums show significant price variance for identical coverage due to insurer pricing models favoring new customers over existing customers. Shopping homeowners, auto, and other insurance annually typically reduces premiums 10-20% without changing coverage levels.

Compression approach: request quotes from 3-5 insurers annually, compare coverage details line-by-line to ensure equivalence, negotiate with current insurer using competing quotes as leverage, switch if savings exceed $200 annually to offset minor inconvenience of policy transfer. A household paying $1,800 annually for auto insurance can often reduce to $1,400-1,500 through shopping while maintaining identical liability limits, deductibles, and coverage features.

Utility costs and usage optimization. Utility spending (electricity, gas, water, internet, mobile) is partially fixed but shows 15-30% compression potential through provider shopping and usage optimization. Internet service particularly shows high compression potential—households paying $80-100 monthly for gigabit internet when 100-200 Mbps service at $40-50 monthly provides equivalent performance for typical usage patterns.

Compression tactics include: calling providers annually to negotiate retention pricing (often saves $10-30 monthly), switching to lower-tier service plans matching actual usage (most households use 20-40% of purchased internet bandwidth), bundling services strategically when bundle pricing beats a la carte (but avoiding bundles including unnecessary services), and implementing basic energy efficiency (programmable thermostats, LED bulbs) reducing electricity costs 10-15% with minimal behavior change.

What Not to Cut During Expense Compression

Health and preventive care spending. Delaying preventive medical care, dental checkups, or prescription medications to reduce short-term expenses typically creates larger long-term costs. A $150 dental cleaning preventing $2,000 root canal saves $1,850 net. A $30 monthly prescription managing chronic condition prevents $50,000 emergency room visit. Health spending should be evaluated for efficiency (generic medications vs brand names, in-network vs out-of-network providers) but not eliminated.

Emergency fund contributions. Stopping emergency fund contributions during expense compression creates vulnerability to financial shocks that destroy compression progress. Someone compressing expenses $400 monthly to pay debt but maintaining $0 emergency fund faces high risk that unexpected $1,500 car repair forces credit card usage, adding debt and interest costs exceeding compression savings. Minimum emergency fund contribution ($50-100 monthly) should continue during compression period.

Professional development and income-generating expenses. Expenses directly supporting income generation or career advancement rarely should be cut during compression. A $40 monthly professional association membership providing industry networking and job opportunities has positive expected return. A $200 certification exam increasing earning potential $5,000 annually returns 25x first-year value. Cut expenses enabling consumption, preserve expenses enabling income growth.

Relationship and social connection spending. Completely eliminating social spending and relationship maintenance costs during compression period often damages relationships and creates social isolation. Compression should target expensive low-value social spending (expensive dinners providing minimal enjoyment over cheaper alternatives) while preserving meaningful social connection. Suggesting potluck dinner instead of restaurant meal with friends maintains relationship at 80% lower cost.

Compression Timeline and Expectations

Immediate compression opportunities (1-7 days). Subscription cancellations, service plan downgrades, and unnecessary purchase elimination create savings within first week. Canceling $150 in unused subscriptions, downgrading internet plan saving $30 monthly, and eliminating impulse purchases saves $200+ monthly with decisions requiring under 2 hours total time investment. This immediate compression category provides quick wins building momentum for larger compression decisions.

Short-term compression (30-90 days). Insurance shopping, negotiating bills, and changing purchasing habits create savings within 30-90 days but require more effort than immediate compression. Shopping auto and home insurance requires obtaining 3-5 quotes and comparing coverage details. Negotiating rent or mortgage refinancing requires market research and applications. Changing food purchasing patterns requires establishing new shopping routines. This category typically produces largest absolute savings ($300-600 monthly) but requires sustained effort over 1-3 months.

Long-term compression (6-12 months). Housing relocation, vehicle changes, and lifestyle restructuring create largest percentage savings but require 6-12 months to implement. Relocating to lower-cost housing requires lease expiration or strategic lease breaking. Selling financed vehicle and buying used replacement requires time to find appropriate vehicle and execute sale. These decisions should be evaluated during early compression phase but often execute months later when timing aligns with existing commitments.

Compression as temporary strategy vs permanent lifestyle. Aggressive expense compression works best as temporary intervention during financial crisis, debt payoff sprint, or savings accumulation for specific goal rather than permanent extreme frugality. Compressing expenses 25% for 12 months to eliminate $10,000 debt provides clear purpose and endpoint. Compressing expenses 25% permanently often creates deprivation mindset and eventual spending rebound when willpower depletes. Sustainable expense management balances compression during high-need periods with moderate spending during stable periods.

Measuring Compression Effectiveness

Tracking absolute savings and percentage reduction. Effective compression tracking measures both absolute monthly savings (total dollars reduced) and percentage reduction by category. A household reducing food spending from $1,200 to $900 monthly achieved $300 absolute savings and 25% category reduction. Tracking both metrics prevents false wins where small percentage reductions in small categories create minimal absolute impact while large categories remain unaddressed.

Evaluating lifestyle impact and sustainability. Compression succeeds when it reduces expenses without proportional reduction in life satisfaction. Monthly review should evaluate whether compression tactics are sustainable or creating deprivation requiring course correction. Someone reducing food spending 30% but reporting constant hunger and food dissatisfaction has compressed too aggressively. Someone reducing food spending 20% while maintaining meal satisfaction has found sustainable compression level.

Calculating compression ROI for time-intensive tactics. Some compression opportunities require substantial time investment with minimal savings. Driving 20 miles to save $5 on groceries costs more in time and vehicle expenses than savings generated. Spending 10 hours monthly extreme couponing to save $80 earns $8 hourly—less than working additional part-time hours. Focus compression effort on high-impact decisions (negotiating $200 monthly rent reduction in 2-hour conversation) rather than time-intensive tactics producing minimal savings.

Common Compression Mistakes to Avoid

Cutting value to reduce spending. Eliminating expenses providing high value relative to cost reduces quality of life more than finances improve. Canceling $50 monthly gym membership when gym usage provides health benefits, stress reduction, and social connection worth $200+ monthly in alternative costs eliminates $50 expense while destroying $200 value. Preserve high-value spending, eliminate low-value spending.

Focusing on small expenses while ignoring large categories. Someone meticulously tracking coffee purchases ($40 monthly) while paying $500 above-market rent wastes effort on low-impact optimization. The 80/20 rule applies strongly to expense compression—80% of compression opportunity exists in 20% of expense categories (housing, transportation, food). Address large categories first, optimize small expenses only after major compression opportunities are exhausted.

Confusing cheap with frugal. Cheap means spending less regardless of value received. Frugal means maximizing value per dollar spent. Buying $20 shoes requiring replacement every 3 months costs more annually than buying $80 shoes lasting 18 months. Cheap focuses on minimizing individual transaction costs. Frugal focuses on minimizing total cost of ownership while maintaining quality. Compression should target frugality, not cheapness.

Creating new expenses while compressing old expenses. Someone canceling $120 gym membership but spending $150 monthly on home workout equipment has increased expenses while appearing to compress. Track net change in expenses rather than focusing exclusively on successful cuts while ignoring new spending. Effective compression reduces total spending, not just reallocates spending across categories.

Resources

Official Sources

BLS: Consumer Expenditure Surveys — Bureau of Labor Statistics data on average household spending by category, providing benchmarks for evaluating expense levels and compression opportunities.

CFPB: Budget and Saving Tools — Consumer Financial Protection Bureau resources for creating budgets, tracking spending, and identifying areas for expense reduction.

FTC: Consumer Information — Federal Trade Commission guidance on consumer rights, avoiding scams, and making informed financial decisions.

Continue Building Financial Stability

Expense compression is one component of comprehensive financial stability. The complete framework for building emergency funds, managing income volatility, and creating financial resilience is in the Financial Stability guide.

Frequently Asked Questions

How much can I realistically cut from my expenses?

Most households can compress expenses 15-25% within 90 days by addressing subscription bloat, insurance inefficiency, and food waste without significant lifestyle changes. Households with above-average housing or transportation costs relative to income may achieve 30-40% compression through strategic housing or vehicle decisions requiring 6-12 months to implement. Compression beyond 25% typically requires lifestyle changes affecting quality of life.

Should I cut expenses or increase income?

Both strategies work synergistically rather than as alternatives. Expense compression creates immediate cash flow improvement within days to weeks. Income increase typically requires months to implement through career advancement or side business development. Compress expenses first for quick wins and immediate financial relief, then focus on income growth for long-term improvement. A $500 monthly expense reduction plus $500 monthly income increase creates $1,000 monthly improvement—same absolute impact as either strategy alone at double magnitude.

What expenses should I cut first?

Start with unused subscriptions and services (immediate savings, zero lifestyle impact), then insurance shopping and bill negotiation (moderate effort, large savings), then food optimization (behavioral change, sustainable savings), finally housing and transportation (largest impact, longest implementation timeline). This sequence builds momentum through quick wins while researching larger compression decisions requiring more time to execute.

How long should I maintain aggressive expense compression?

Treat aggressive compression as temporary intervention with defined endpoint rather than permanent lifestyle. Compress expenses aggressively while paying off debt, building emergency fund, or saving for specific goal, then relax to moderate sustainable spending level after goal achievement. Attempting permanent extreme compression typically creates deprivation leading to eventual spending rebound. Typical compression period: 6-18 months depending on specific financial goal.

Will cutting expenses make me miserable?

No, if compression targets waste and inefficiency rather than value. Canceling unused gym membership creates zero life satisfaction reduction. Negotiating lower insurance rates maintains identical coverage at lower cost. Buying store-brand groceries provides equivalent food quality at lower price. Compression creates misery when it eliminates high-value spending—canceling used gym membership, eliminating all social spending, refusing preventive medical care. Focus on low-value cuts preserving life satisfaction.

What if I have already cut everything I can?

Review spending across 3-6 months identifying every recurring charge and discretionary expense. Most people claiming maximum compression maintain unused subscriptions, pay above-market rates for commodity services, or have optimization opportunities in large categories. If housing, transportation, and food combined equal 60%+ of income, compression opportunity exists through strategic downsizing, relocation, or vehicle change even if small expenses are already optimized. If truly no compression opportunity exists, focus shifts from expense reduction to income increase.

PersonalOne Money System

This content is researched, written, and owned by PersonalOne — a free financial education platform built to help Millennials and Gen Z build real financial systems.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Expense compression strategies should be tailored to individual financial situations, goals, and values. Some compression tactics may not be appropriate for all households. Cutting certain expenses (health care, insurance, emergency fund contributions) can create long-term financial harm despite short-term savings. Consult qualified financial professionals before making major housing, transportation, or financial decisions. PersonalOne is not responsible for decisions made based on this content.