Published: March 4, 2026

Home › Banking Systems › Multiple Account Budgeting System › Why You Need a Separate Account for Bills

About the Author

Don Briscoe is a financial systems coach with 12+ years helping Millennials and Gen Z escape paycheck-to-paycheck cycles. He has worked with hundreds of people to build emergency funds, eliminate debt, and start investing using framework-first strategies that require less willpower and more infrastructure. He founded PersonalOne to provide the financial education he wished existed -- structured, honest, and free.

TL;DR -- What You Will Learn

A separate bills account is the single most important account separation in personal finance. When bills share space with spending money, you are forced to do mental math before every purchase -- can I afford this, or do I have bills coming?

The solution: Dedicate one checking account exclusively to fixed monthly bills. Fund it automatically on payday. Set all bills to autopay from it. Never touch it for spending.

- Why bill and spending separation matters more than any other account split

- The psychology of why this simple change eliminates money stress

- Exactly how to calculate your bills account funding amount

- Step-by-step setup process from opening to automation

- What happens when bills and spending live in the same account

Picture this: it is Thursday. Your checking account shows $1,200. You are at the coffee shop debating whether to buy the $7 latte.

But wait -- is rent due tomorrow or next week? When does car insurance hit? The phone bill already came out, right? Or was that last month?

You pull out your phone, check your bank app, scroll through pending transactions, try to remember what bills are scheduled for autopay, and ultimately decide you are not sure if that $7 is really safe to spend.

This is bill anxiety. And a separate bills account eliminates it completely.

The Core Principle of Multi-Account Systems

Bills account separation is the foundation of the multiple account budgeting system that eliminates financial stress. While you can add more accounts for specific purposes, this single separation -- bills versus spending -- creates more clarity than any other financial strategy.

Once bills are isolated, your spending account balance becomes perfectly accurate. What you see is what you can actually spend.

What Happens When Bills and Spending Share an Account

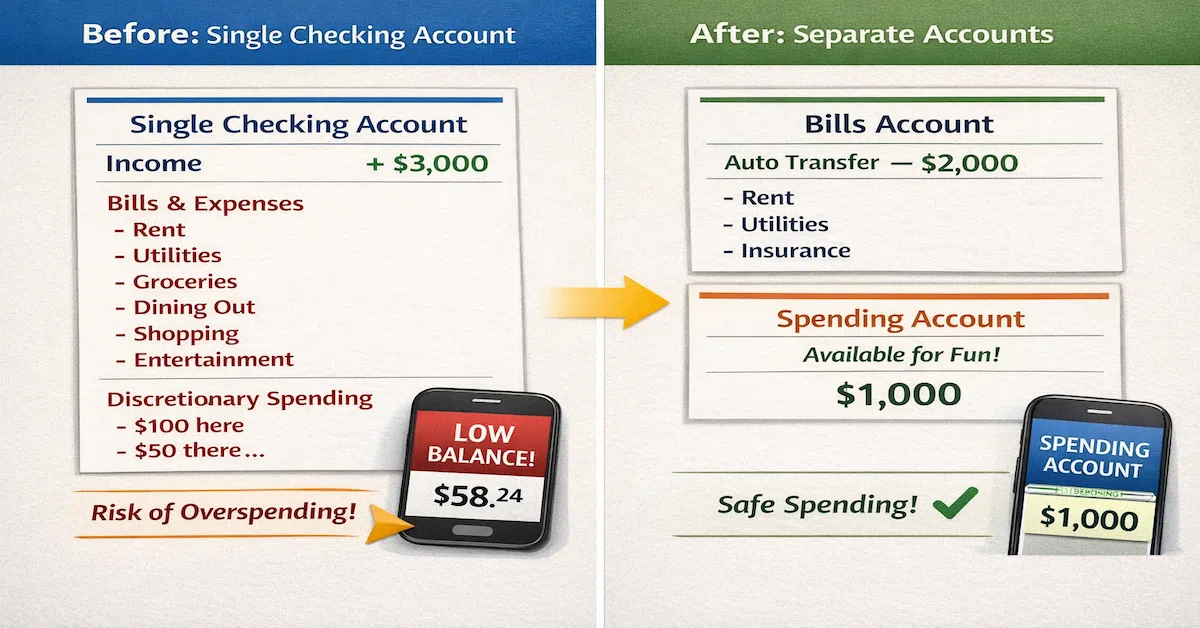

Most people operate with a single checking account. Income lands there. Bills pay from there. Spending happens from there. And chaos lives there.

You get paid $2,500 on Friday. Your account shows $2,500. Your brain registers that you have $2,500. But actually $1,200 is allocated to rent due in 10 days, $150 is for car insurance autopaying in 5 days, $80 is for utilities already scheduled, $60 is for subscriptions scattered throughout the month, and $200 is for minimum debt payments. The available money is actually $810 -- but your account shows $2,500, and every time you look at that balance your brain has to run that calculation manually.

Failure Mode 1: Decision Paralysis

Every purchase requires mental math. You are never quite sure if money is truly available or if you are about to spend bill money. This creates what psychologists call decision fatigue -- by the end of the day you are exhausted from constantly evaluating whether purchases are safe.

Failure Mode 2: Accidental Overspending

You see $1,500 in your account. You grab groceries ($80), fill up gas ($50), buy dinner ($40). Three reasonable purchases. But rent is due tomorrow and now you are $170 short. You did not consciously decide to spend bill money -- your brain just saw the available balance and treated it as spendable.

Failure Mode 3: Bill Payment Anxiety

Even when you successfully avoid overspending, you never feel confident about bills. You check your balance before every bill due date. You worry about whether autopay will clear. The stress is not about not having enough money -- it is about not knowing if the money sitting there is actually available.

Why Physical Separation Works

A separate bills account solves all three failure modes by creating structural clarity instead of relying on mental discipline.

Your Spending Account Balance Becomes Truth

When bills are separated, the number you see in your spending account is genuinely available. If it shows $600, you have $600 to spend. No calculations required. No wondering if bills are pending. The question of whether you can afford something has a simple answer: check the spending account balance.

Bills Cannot Be Accidentally Spent

Bill money lives in a different account. You do not have access to it when making purchases. This is not about willpower or discipline -- it is about making the wrong behavior structurally impossible.

Bill Payment Becomes Automatic

Once your bills account is funded properly, bills pay themselves with zero mental involvement. You never check if the money is there -- you know it is there because the funding happens automatically on payday. The anxiety disappears because the uncertainty disappears.

How to Calculate Your Bills Account Amount

Before opening a bills account, you need to know how much to fund it. This calculation is simpler than it looks.

Step 1: List All Fixed Monthly Expenses

Write down every bill that hits your account predictably each month: rent or mortgage, car payment, insurance (auto, renters, health, life), utilities (use a 3-month average), phone, internet, streaming and subscription services, minimum debt payments, and childcare or tuition if applicable.

Step 2: Add Up Your Monthly Bill Total

Example: Rent $1,200 + Car payment $320 + Car insurance $140 + Utilities $110 + Phone $60 + Internet $70 + Subscriptions $45 + Minimum credit card payment $80 = $2,025 per month.

Step 3: Add a 10-15% Buffer

Bills are not perfectly predictable. Utilities spike. You forget a subscription. A bill increases without warning. Add 10-15% cushion: $2,025 x 1.12 = $2,268. Round to $2,300 for simplicity.

Step 4: Divide by Number of Paychecks

Biweekly (26 paychecks/year): $2,300 ÷ 2 = $1,150 per paycheck. Twice monthly: $2,300 ÷ 2 = $1,150. Monthly: $2,300 once. Weekly: $2,300 ÷ 4 = $575 per week. This is your automatic transfer amount every payday.

Step-by-Step Bills Account Setup

Step 1: Open a Dedicated Bills Checking Account

Most banks allow you to open a second checking account at no cost. Requirements: free account with no monthly fees, no minimum balance, online bill pay capability. Name it something obvious -- Bills Account or Fixed Expenses -- so there is no confusion with your spending account. Do not order a debit card for this account.

Step 2: Set Up Automatic Transfers

Schedule automatic transfers from your main checking account to your bills account to execute 1-2 days after each payday. If you are paid on the 1st and 15th, schedule transfers on the 2nd and 16th. Most banks call this recurring transfers or scheduled transfers in online banking settings.

Step 3: Move All Bills to the Bills Account

For each biller: log in, update your payment method to the new bills account, enable autopay if not already active, confirm the change went through. Time estimate: 45-60 minutes to update 8-12 billers. This only needs to be done once.

Step 4: Seed the Account

The first month requires manual funding since bills hit before your automatic transfers establish a balance. Transfer your full monthly bill total to the bills account immediately after opening it to ensure bills due in the next 30 days are covered.

Step 5: Monitor for 2-3 Months

Check the bills account weekly for the first few months. Balance too low -- increase your transfer by $50-100. Balance growing steadily -- you are overfunding, decrease slightly. Balance stable around $200-300 -- your buffer is working. After 3 months you rarely need to check it. The system runs itself.

What This Looks Like After Setup

Maria earns $3,200 per month, paid biweekly ($1,600 per paycheck). Her monthly bills total $1,900. Every payday: $1,600 deposits into her main checking, an automatic transfer of $950 moves to the bills account, and $650 remains in checking for spending. Rent autopays on the 1st, car payment on the 10th, insurance on the 15th, utilities when due.

When Maria checks her spending account and sees $200, she has $200 to spend -- no calculations, no second-guessing. She has not checked her bills account in two months. Zero bill payment anxiety. This is what financial clarity feels like.

Common Concerns Answered

Is This Just Complicating Things?

The initial setup takes 1-2 hours. It eliminates hundreds of hours of mental calculation, balance checking, and financial stress over the following year. You are trading 2 hours of setup for permanent peace of mind.

What If I Need to Pull From the Bills Account?

You can. But the physical separation creates a pause -- is this really an emergency worth risking bill coverage? Ninety percent of the time the answer is no. The friction saves you from impulsive decisions.

My Bank Charges Fees for Multiple Accounts

Switch banks. Most online banks and credit unions offer free checking with no minimums. Account structure only works if it is cost-free. If your bank charges fees for this, you are subsidizing outdated infrastructure instead of building your own.

What About Irregular Bills?

Calculate annual irregular bills -- car registration, holiday spending, annual insurance renewals -- and divide by 12. Add that monthly amount to your bills account funding. Example: $600 car registration + $800 holiday spending = $1,400 annually ÷ 12 = $117 extra per month to the bills account.

Master the Complete Banking System

Bills account separation is the foundation. The Banking Systems authority hub covers the full account architecture -- how to layer spending accounts, savings automation, and a complete money flow system that runs on autopilot.

Explore the Banking Systems Hub →Frequently Asked Questions

Should my bills account be at the same bank as my spending account?

Start with the same bank for simplicity. Transfers between accounts at the same institution are instant, and you can manage everything in one app. Once the system is stable you can move the bills account elsewhere if desired, but there is no advantage to doing so initially.

What if a bill amount changes unexpectedly?

This is why you build a 10-15% buffer. If your electric bill spikes $40 one month, the buffer absorbs it. If bills consistently exceed your funding, increase your transfer amount by $50-100 and monitor for another month.

Can I use this system with irregular income?

Yes, but modify the approach. Instead of splitting your bills across paychecks, transfer your full monthly bill total as soon as income arrives, then allocate the remaining money to spending and savings. The structure stays the same -- only the timing adjusts.

Should I get a debit card for my bills account?

No. The bills account should have exactly two access points: automatic transfers in and scheduled autopay out. A debit card creates temptation to spend from it. If you need to make a manual payment, log into online banking and pay directly from there.

How much buffer should I keep in the bills account?

Aim for $200-300 beyond what is needed for the current month. This handles unexpected increases without manual intervention. If your buffer consistently grows beyond $500, reduce your transfer amount slightly.

What if my bills decrease after paying off a loan?

Reduce your bills account funding and redirect the freed-up amount to spending or savings. If your bills drop $150 per month, decrease your transfer by $75 per paycheck. Every dollar freed from bills is a dollar you can deploy deliberately.

Can I use credit cards with this system?

Yes. If you pay your credit card in full monthly, treat the payment as a bill -- add it to your monthly bill total and set it to autopay from your bills account. The purchases come from your spending budget, but the payment is treated as a fixed expense.

Resources

- How to Set Up a 3-Account Money Flow System That Actually Works -- Step-by-step implementation including bills, spending, and savings

- Where Your Paycheck Should Go First: Designing Your Money Flow -- How to route income to fund your bills account automatically

- Financial Automation: How to Run Your Money on Autopilot -- Next step after your account structure is built

- CFPB -- Bank Accounts and Money Management

- FDIC -- Consumer Resources and Banking Guidance

Disclaimer: This guide provides general educational information about bills account separation and personal finance strategies. It is not personalized financial advice. Your optimal account structure depends on your income consistency, expense patterns, bill amounts, and personal preferences. Before making significant changes to your banking setup, consider your complete financial situation and consult with a qualified financial professional if needed. PersonalOne provides educational content and does not offer personalized financial planning services.