January 24, 2026

January 24, 2026

Home › Banking Systems › The 3-Account System Explained

About the Author

Don Briscoe is a financial systems coach with more than 12 years of experience helping Millennials and Gen Z escape the paycheck-to-paycheck cycle. His framework-first approach focuses on building financial infrastructure that works automatically — less willpower, more systems. He founded PersonalOne.org to make structured, honest financial education free and accessible.

TL;DR — The 3-Account System Explained

— The 3-account system separates money into bills, spending, and savings accounts — each with one job, no overlap.

— This method prevents overspending, automates savings, and eliminates bill-paying stress without requiring constant tracking.

— Setup takes 2–3 hours initially but eliminates hours of financial mental load every month going forward.

— Works best with direct deposit splits and automatic transfers scheduled on payday.

— Start with the 50/30/20 rule as a baseline, then adjust percentages based on your actual spending patterns.

Picture this: it is three days before payday, you check your account balance, and your stomach drops. You thought you had enough money to last the week, but you forgot about an automatic bill coming out tomorrow. Now you are scrambling to move money around, hoping nothing bounces.

If this feels familiar, you are not alone. Millions of Americans deal with this exact problem — not because they do not earn enough, but because everything is mixed together in one account with no structure. The balance looks fine until it suddenly is not.

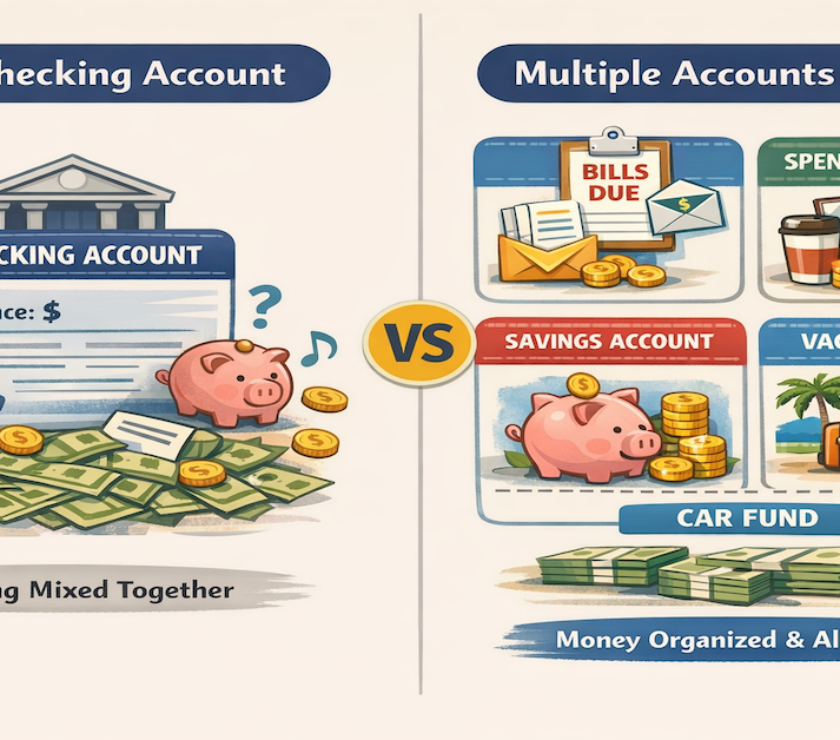

The 3-account system solves this by creating clear boundaries for your money. Instead of one checking account doing everything, you split funds into three dedicated accounts: one for bills, one for spending, and one for savings. Each account has one job. No overlap, no confusion.

This is not about restriction. It is about clarity. When you know exactly what money is for what purpose, financial decisions become straightforward — and most of them stop requiring decisions at all.

What Is the 3-Account System?

The 3-account system is a money management framework that divides income into three separate bank accounts, each with a specific purpose. Think of it as creating lanes on a highway — instead of all your money merging into one chaotic stream, each dollar knows exactly where it is supposed to go.

Account 1 — Bills

Fixed expenses live here. Rent, utilities, insurance, subscriptions, loan payments — anything automatic or on a predictable schedule. This account should be boring and stable.

Account 2 — Spending

Daily life money. Groceries, gas, restaurants, entertainment, clothing — anything you actively decide to spend on. This is where your debit card lives. The balance here is your actual available money.

Account 3 — Savings

Your financial future. Emergency fund, goals, down payments — off-limits for daily spending. It grows quietly in the background while you live your life.

Unlike budgeting methods that require tracking every transaction, the 3-account system creates automatic boundaries. You are not constantly deciding whether you can afford something — the answer is already built into which account the money lives in.

Why the 3-Account System Works

Traditional single-account banking creates a problem psychologists call mental accounting errors. When all money lives in one place, your brain constantly calculates: can I afford this? Will I have enough for rent? Did I forget about any bills? That mental load is exhausting, and it leads to two predictable mistakes.

Overspending from a seemingly large balance. Your account shows $2,000, so dinner out feels fine — except $1,400 of that is already spoken for by bills you have not paid yet.

Artificial scarcity mindset. You deny yourself reasonable purchases because you are worried about unknown future expenses — even when the money is genuinely available.

The 3-account system eliminates both problems by making your financial reality visible and concrete. When you look at your spending account balance, that number is accurate. No mental math required.

The Psychology Behind Separation

Behavioral economics research consistently shows that people manage money better when it is physically or digitally separated. It is the same reason envelope budgeting works — when you can see that your grocery envelope only has $80 left, you naturally adjust your behavior. Digital account separation creates the same psychological boundaries without dealing with cash.

Setting Up Your 3-Account System

Setup takes about 2–3 hours of focused work upfront. That initial investment eliminates financial stress month after month. Here is exactly how to do it.

Step 1 — Choose Your Banking Setup

Option A — All accounts at one bank. The simplest approach. Most banks allow multiple checking and savings accounts under one login, making transfers instant and management easy. The psychological separation of having distinct accounts is what matters, not whether they are at different institutions.

Option B — Strategic multi-bank setup. More sophisticated: bills at a local credit union for easy bill pay, spending at a bank with the best ATM network or debit rewards, and savings at an online bank earning the highest available APY. More setup involved, but maximizes benefits across all three accounts.

Either way, prioritize zero monthly maintenance fees and no minimum balance requirements. The account structure should not cost you money.

Step 2 — Calculate Your Numbers

Bills account total: List every fixed expense — rent, utilities, insurance, car payment, student loans, credit card minimums, subscriptions, phone bill, childcare. Add them up, then add 5–10% as a buffer for variable utilities or annual charges divided monthly.

Savings target: Aim for 20% of gross income, but 10% is a perfectly valid starting point. Consistency matters more than the percentage. Divide by pay period — if paid biweekly, divide monthly target by 2.

Spending account: Everything remaining after bills and savings. This covers groceries, gas, restaurants, entertainment, personal care, and all variable daily expenses.

Sample Calculation — $4,000 Monthly Income

Bills Account: $2,000 (50%)

Savings Account: $600 (15%)

Spending Account: $1,400 (35%)

Step 3 — Automate the Flow

Automation is what converts this system from a good idea into infrastructure that runs without you. If your employer offers direct deposit splitting, contact HR and request your paycheck split directly — a fixed amount or percentage to bills, a fixed amount to savings, and the remainder to spending. This is the gold standard.

If direct deposit splitting is not available, have your full paycheck deposit into spending, then set automatic transfers to bills and savings on the same day the paycheck hits. Most banks support recurring transfers with specific dates. Timing these for the morning after payday ensures funds have cleared.

Step 4 — Connect Bills to Autopay

Once the bills account is funded, connect every recurring bill to autopay from that account — either through each biller's website or your bank's bill pay service. Schedule payment dates that give yourself a buffer after payday: if paid on the 1st and 15th, schedule bill payments for the 5th and 20th. Keep a running list of each bill, its amount, and payment date. Review it quarterly to catch changes or forgotten subscriptions.

Step 5 — Link Spending Account to Daily Life

Your spending account becomes your primary interface with money. Connect your debit card here. Link Apple Pay, Google Pay, Venmo, Cash App, and PayPal to this account. Use this account number for online shopping. Your bills account should be nearly invisible in daily life — no debit card, no daily logins. It just quietly handles obligations in the background.

How to Allocate Money Across the Three Accounts

The 50/30/20 rule is a proven starting point — 50% to bills, 30% to spending, 20% to savings. It translates directly to the three-account structure and works well for middle-income households in moderate cost-of-living areas. But your actual allocation should reflect your real expenses, not an ideal ratio.

| Account | Starting % | What It Covers |

|---|---|---|

| Bills Account | 50% | Fixed expenses and necessities |

| Spending Account | 30% | Variable expenses and daily life |

| Savings Account | 20% | Emergency fund and financial goals |

High cost-of-living adjustments: If bills consume 60–70% of income, adjust to 65% bills / 25% spending / 10% savings. That is not failure — that is reality.

Debt payoff mode: Treat extra debt payments as part of bills — 55–60% bills (including accelerated payments) / 20–25% spending / 15–20% savings. Never reduce savings to zero.

Building emergency fund: Temporarily boost savings to 25% until you hit $1,000–2,000, then ease back to a sustainable rate.

Review and rebalance allocations quarterly or after any significant life change — raise, job change, paid-off loan, rent increase. The goal is a system that reflects current financial reality, not an ideal scenario that creates stress.

Common Mistakes and How to Avoid Them

Underfunding the bills account. The most common error. Add 10% buffer to your bills calculation to cover variable utilities, annual subscriptions divided monthly, and quarterly charges. Review the bills account every three months to catch shortfalls early.

Raiding savings for non-emergencies. Every withdrawal for discretionary spending teaches yourself the boundaries do not matter. If you consistently cannot leave savings alone, create a fourth sinking fund account for planned non-essential purchases — or adjust spending upward and savings down to a rate you can actually maintain. An 18% savings rate you stick to beats a 20% rate you constantly undermine.

Making the spending account too small. Aggressive savers sometimes allocate 10% to spending. When the spending account runs dry mid-month and you still need groceries, the system breaks. Be honest about actual spending patterns before finalizing allocations.

Over-complicating with too many accounts. More accounts do not equal better management — they equal more cognitive load and more points of failure. Stick with three core accounts. Use budgeting apps for granular category tracking within the spending account if needed.

Not accounting for irregular expenses. Birthdays, holidays, car registration, medical copays — these feel like surprises but are entirely predictable. Calculate annual irregular expenses, divide by 12, and add that amount to your monthly bills allocation. When December arrives, the money is already there.

Quitting after one bad month. The first month is always messy — expenses you forgot about, allocations that need adjusting. This is normal. Commit to three full months: month one to discover problems, month two to adjust, month three to experience the system working smoothly.

The 3-Account System Is the Foundation. The Full Architecture Goes Further.

The three-account structure solves the most common banking problems. For the complete banking framework — income routing, paycheck flow design, and multi-account infrastructure for every income type — see the PersonalOne guide on how to structure your bank accounts. Free, no signup required.

Framework-first. Less willpower. More infrastructure.

Frequently Asked Questions

Do I need three separate banks or can I use one?

One bank works fine. Most banks allow multiple checking and savings accounts under one login, making transfers instant. The psychological separation of having distinct accounts is what matters — not whether they are at different institutions. Using different banks can have advantages (higher APY on savings at online banks, better ATM access elsewhere), but the system works either way. Choose whatever reduces friction for you.

What if I get paid weekly or biweekly instead of monthly?

The system works with any pay frequency. Divide monthly allocations by pay periods: weekly divide by 4 (or 4.33 for precision), biweekly divide by 2. For biweekly pay, the two extra paychecks per year (26 periods vs 24) can go entirely to savings or debt payoff since monthly bills are already covered by the standard 24.

Should credit card payments come from bills or spending?

Depends on the card's purpose. Minimum payments and balances you are actively paying down belong in bills — they are fixed obligations. If you use a credit card for daily spending and pay it off monthly, pay the statement balance from spending, since the card was just a payment method for spending you already tracked. Many people pay their rewards card from spending weekly to maintain accurate awareness of what they have actually spent.

How much buffer should each account carry?

Bills account: one month of bills beyond current obligations — this covers early-hitting charges or payroll delays. Spending account: keep it lean, just enough to cover one week between paychecks. A large balance here is money better deployed in savings. Savings account: no upper limit — build toward 3–6 months of expenses for an emergency fund, then save for specific goals.

What do I do with windfalls like tax refunds or bonuses?

Direct windfalls to savings first, then follow your financial priorities. High-interest debt: 80% toward payoff, 20% discretionary. Incomplete emergency fund: all of it there. Financially stable: 50% to savings goals, 30% to guilt-free spending, 20% to bills buffer. The key is being intentional — a $3,000 tax refund should not just dissolve into routine spending.

Can I use this system while paying off debt?

Yes — the 3-account system makes debt payoff more reliable because extra payments happen automatically rather than requiring willpower at month-end. Treat accelerated debt payments as part of your bills allocation (60% bills including extra payments / 25% spending / 15% savings is a workable debt-payoff configuration). Never reduce savings to zero while paying debt — a small emergency fund prevents you from going deeper into debt when unexpected expenses hit.

What if my income varies significantly month to month?

Calculate your average monthly income over the past 6–12 months and use that as your allocation baseline. In high-earning months, surplus flows to savings. In low months, draw from savings to maintain standard bills and spending allocations. Keep a larger bills buffer — 2–3 months of fixed expenses — to protect against extended slow periods. This smooths income volatility and prevents the feast-or-famine cycle.

Resources

CFPB — Bank Account Consumer Tools and Resources — Federal guidance on checking, savings, and consumer protections.

FDIC — Consumer Protection and Deposit Insurance — Deposit coverage and consumer rights across account types.

FDIC BankFind — Verify Institution Insurance Status — Confirm FDIC coverage for any bank before opening an account.

Disclaimer: The content on PersonalOne.org is for informational and educational purposes only and does not constitute financial advice. Banking products, interest rates, and account features change over time. Always review current account agreements and fee schedules before opening new accounts or making banking changes. FDIC insurance covers up to $250,000 per depositor per institution — verify coverage directly with the FDIC before opening any account.