June, 2026

Home › Banking Systems › Account Separation for Different Life Stages › How Families Should Structure Bank Accounts to Protect Every Dollar

Part of Account Separation for Different Life Stages — how to structure your banking as your income, responsibilities, and financial goals evolve.

What You Need to Know

— When a family forms, the two-account couple structure that worked before is no longer enough. Children introduce new expense categories, new savings goals, and new financial risks that need their own accounts.

— The most common family banking mistake is letting the emergency fund carry the weight of children's savings, irregular family expenses, and household bills simultaneously. Those are four different pools of money and they need four different accounts.

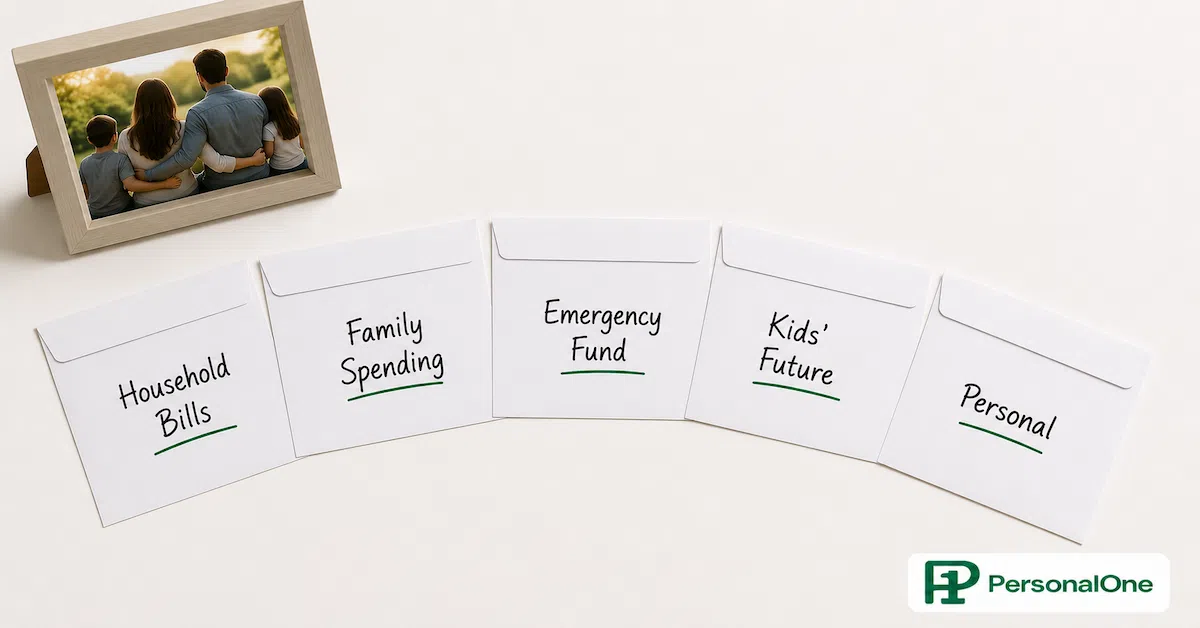

— A family bank account structure that protects every dollar separates money by purpose: household bills, daily spending, emergency reserves, and children's future money each live in their own account.

— Children's savings grow fastest when they are separated from accounts the family accesses for daily decisions. Money that is visible and accessible gets spent. Money in a separate account earns interest and stays protected.

— The family structure is the same three-account system that works at every life stage — expanded by two accounts to protect the new financial responsibilities children bring.

When a family grows, the banking structure that worked before stops being enough. The couple setup — joint bills account, joint savings, individual spending accounts — was designed for two adults with shared and individual financial goals. Adding children adds new expense categories that are non-negotiable, new savings goals with long timelines, and a new level of financial vulnerability that requires more separation, not less.

The families that feel perpetually behind on money are not usually behind on income. They are behind on structure. Everything lives in the same account — or in two accounts that are doing the work of five. The children's savings fund gets raided when a car breaks down. The emergency fund doubles as the vacation savings. The household bills share an account with the family's discretionary spending. Every dollar is technically present but nothing is protected because there is no structural mechanism to protect it.

This guide covers the bank account structure for families that gives every dollar a designated role — how many accounts a family actually needs, what each one holds, and how money flows between them automatically so the structure runs without constant management. The complete framework for how account structure works across every life stage is in the banking systems account structure guide.

If you and your partner already have the couples structure in place, this article shows exactly what to add. If you are building from scratch as a family, it covers the full architecture from the ground up.

Why the Couple Account Structure Is Not Enough for a Family

The couple account structure — joint bills, joint savings, individual spending — is built around two financial lives converging. It handles shared obligations and personal autonomy cleanly. What it does not handle is the financial complexity that children introduce.

Children create new categories of non-negotiable expense: childcare, pediatric healthcare, school supplies, activities, clothing that needs replacing every six months. They create new long-horizon savings goals: education funds, custodial accounts, future financial independence. And they create a new urgency around the emergency fund — a family with children needs three to six months of household expenses protected, not the one to two months that works for a couple without dependents.

None of those new financial responsibilities belong in the existing accounts. Childcare expenses are household bills and belong in the joint bills account — but children's savings are not household bills and should not live in the same place. The emergency fund needs to grow to reflect the family's actual vulnerability — but it should not double as the college savings fund or the children's clothing budget. Each category needs its own account because each serves a different function and operates on a different timeline.

The Family Bank Account Structure: Five Accounts, Five Jobs

The family structure builds directly on the couple structure. Three accounts carry over with expanded roles. Two new accounts are added for family-specific financial needs. Together they give every dollar a designated location and a clear purpose.

Account 1 — The Household Bills Account (Joint Checking)

What it holds: Every fixed recurring household expense — mortgage or rent, utilities, insurance premiums, phone bills, internet, childcare costs, school fees, subscription services, minimum debt payments. Any expense the household owes regardless of month-to-month decisions.

What changes with children: Childcare is often the largest new line item — rivaling or exceeding rent for many families. It belongs here alongside rent, not in a discretionary spending account. School fees, activity registration, and recurring children's healthcare costs also belong here once they become fixed and predictable.

How it runs: Autopay handles everything. Both partners contribute via automatic transfer on payday. No debit card used for personal purchases. The bills system that never overdrafts covers the complete setup for keeping this account funded and running without timing gaps.

Account 2 — The Family Spending Account (Joint Checking)

What it holds: Groceries, family dining, household supplies, children's clothing and incidentals, family entertainment, and any discretionary household spending that varies month to month.

Why it is separate from bills: Family spending is variable — the grocery bill fluctuates, a child needs new shoes, the family takes a day trip. Bills are fixed and protected. Keeping variable spending in its own account means the family can spend freely within that account's balance without risk of accidentally touching bill money.

How it runs: Both partners contribute a fixed monthly amount after bills contributions are made. This is the account the family debit card is attached to. When it runs low, that signals discretionary spending needs to slow down — not that bills are at risk.

Account 3 — The Family Emergency Fund (Joint High-Yield Savings)

What it holds: Three to six months of total household expenses — everything it would cost to run the household and care for the children if one or both incomes were disrupted. This account exists for one purpose: absorbing financial emergencies without debt.

What changes with children: The target grows significantly. A childless couple might need $15,000 in an emergency fund. A family with two children and a mortgage might need $30,000–$45,000. Childcare alone can cost $1,500–$3,000 per month — that expense does not pause during an income disruption.

How it runs: A fixed automatic contribution on payday until the target is reached, then maintained. Earns competitive interest at an online bank paying 4%+ APY. Never used for planned expenses, vacations, or children's savings. The best savings accounts for 2026 covers the top FDIC-insured options with no minimum balance requirements.

Account 4 — The Children's Future Fund (Dedicated Savings)

What it holds: Long-horizon savings for each child — education fund contributions, custodial savings, and any money being set aside for children's future financial independence rather than current household needs.

Why it needs its own account: Money that shares an account with accessible savings gets spent on accessible needs. A college fund in the same account as the family emergency fund will be drawn on during emergencies — that is rational human behavior, not failure. The separation is what makes the protection real.

Account options: A 529 education savings plan for education-specific goals (tax-advantaged, growth tax-free for qualified education expenses). A UGMA/UTMA custodial account for broader goals. A separate high-yield savings account for shorter-term children's savings. The right vehicle depends on timeline and flexibility needs — but the structural principle is the same: it lives apart from the emergency fund and the household spending.

How it runs: A fixed automatic contribution on payday. Even $50–$100 per month per child, started early, compounds significantly over 18 years. The habit matters more than the initial amount.

Account 5 — Individual Personal Accounts (Each Partner)

What they hold: Each partner's personal discretionary spending — clothing, personal care, individual hobbies, gifts to people outside the household, any spending that belongs to one person rather than the family.

Why they survive into the family stage: Financial autonomy matters more, not less, when the household budget is tighter and every dollar feels accounted for. Without a personal spending account, every individual purchase becomes a household financial decision. That dynamic creates resentment and arguments that have nothing to do with the actual money.

What happens to the amount: Personal spending allocations typically shrink when a family forms as more income routes to household needs. That is expected. The account stays regardless of the balance because the structural separation it provides is worth more than the amount inside it.

How Money Flows Through the Family Structure

The power of the structure comes from its automation. On payday, money moves into position before any discretionary spending decision is made. The sequence is fixed and non-negotiable:

The Family Payday Sequence

1. Income lands in each partner's individual checking account.

2. Automatic transfer: each partner's contribution to the household bills account fires immediately.

3. Automatic transfer: emergency fund contribution fires if the fund is not yet at target.

4. Automatic transfer: children's future fund contribution fires.

5. Automatic transfer: family spending account contribution fires.

6. Whatever remains in each individual account is personal spending money. It requires no further decisions because everything else is already funded.

The sequence encodes the family's financial priorities in the infrastructure. Household obligations are funded first. Future security is funded second. Present living expenses are funded third. Personal autonomy receives whatever remains. This is not scarcity management — it is clarity about what matters and in what order, expressed through account structure rather than willpower.

The Most Important Upgrade: Separating the Emergency Fund From Children's Savings

The single most impactful structural decision for most families is putting the emergency fund and children's savings in separate accounts. Most families keep them together — a general savings account that is meant to serve both purposes — and the result is that neither purpose is well-served.

Emergency funds get depleted by planned spending. Children's savings get borrowed against during emergencies and never fully replenished. The balance in a combined savings account is ambiguous — is this money available or protected? That ambiguity is why families with savings still feel financially insecure. They do not know how much of their savings is genuinely unavailable for daily decisions.

Separate accounts remove the ambiguity. The emergency fund balance is always the emergency fund. The children's future fund balance is always the children's future fund. Neither is available for the other's purpose unless an actual decision is made to move money between them — which is a different, deliberate action rather than an accidental drain.

When to Upgrade the Structure as the Family Grows

The five-account family structure is not static. It needs to evolve as the family's financial life changes. The trigger for each upgrade is a new financial responsibility that does not fit cleanly into an existing account.

Second child: Add a separate children's future fund for the second child or expand the existing one with clearly tracked sub-allocations. The household bills account needs recalculating to include the new childcare and healthcare costs.

Home purchase: The household bills account expands to include mortgage, property tax escrow, and homeowner's insurance. A separate sinking fund for home maintenance — typically 1% of home value per year — belongs in its own account rather than in the emergency fund. Home repairs are predictable ongoing expenses, not emergencies.

One partner reduces work for caregiving: The contribution formula needs to shift to proportional or pooled to ensure the caregiving partner retains financial independence within the household. The structure described in the couples bank account structure guide covers how to adjust contribution formulas when incomes diverge significantly.

Children reach earning age: Teaching children to manage their own money using a simplified version of this same structure — spending, saving, giving — is the highest-leverage financial education available. A student checking account and a savings account are enough to introduce the concept before the student version of the full structure makes sense at college age. The student bank account structure guide covers how to set that up when the time comes.

Every Dollar Has a Job. Build the Structure That Assigns It.

The family structure is one configuration of the broader account separation framework. For the complete architecture — how accounts work at every life stage, how income routes correctly, and how the full system runs automatically — see the PersonalOne banking systems account structure guide.

Frequently Asked Questions

Do we need five separate accounts at five different banks?

No. Most of these accounts can live at one or two institutions. The bills account and family spending account are typically at the same bank. The emergency fund and children's future fund work well at a single online bank where both earn competitive interest. Individual personal accounts can stay at whatever institution each partner already uses. The separation that matters is between accounts, not between institutions — though some families find that keeping savings at a different bank from checking creates useful friction that prevents impulse withdrawals.

How much should the emergency fund target be for a family?

Three to six months of total household expenses is the standard guidance. For a family with children, aim for the higher end. Add up everything the household spends in a month — mortgage, childcare, utilities, groceries, insurance, minimum debt payments — and multiply by five or six. For many families this means a target of $25,000–$45,000. That number feels large but is built gradually through fixed automatic contributions. Starting with a $1,000 immediate buffer and building toward the full target is more realistic than waiting until you can fund the full amount at once.

What is the best account for children's savings?

It depends on the goal and timeline. A 529 education savings plan is the most tax-efficient vehicle for college savings — contributions grow tax-free and withdrawals for qualified education expenses are tax-free. The SECURE 2.0 Act now allows unused 529 funds to roll into a Roth IRA for the beneficiary after 15 years, which reduces the risk of over-funding. A UGMA/UTMA custodial account offers more flexibility for goals that are not education-specific. A high-yield savings account works for shorter-term children's goals where flexibility matters more than tax efficiency.

What if we cannot fund all five accounts right away?

Start with the structure, not the amounts. Open the accounts in order of priority — bills account first, emergency fund second, family spending third. Even contributing $25 per month to the children's future fund establishes the account and the habit. The amounts scale as income grows. What does not scale easily is trying to add structure later when the habits of a single-account setup are already entrenched. Build the architecture now at whatever scale is realistic.

How does this structure change when children become financially independent?

When children leave home, the household bills account shrinks significantly as childcare, activity costs, and dependent healthcare expenses end. The children's future fund can be closed or transitioned once the savings goal is complete. The family spending account and emergency fund remain but their targets recalibrate to reflect two adults rather than a household with dependents. This is also the natural moment to reassess the full account structure — the signs your setup has drifted from your actual life are covered in the when to change banks guide.

Official Sources

FDIC — Deposit Insurance Coverage and Bank Verification

More From This Cluster

Return to Account Separation for Different Life Stages for the complete framework on how account structure evolves from student through early career, couples, families, and beyond.

This content is for educational purposes only and does not constitute financial, legal, or tax advice. PersonalOne is not a licensed financial advisor, broker, or investment professional. Account features, fees, and insurance coverage vary by institution and are subject to change. Always verify FDIC insurance status before opening any account. Tax treatment of education savings accounts varies by state and individual situation — consult a qualified tax professional before making decisions about 529 plans or custodial accounts.