August 6, 2025

Updated: May 11, 2026

Home › Financial Stability › Income Volatility Management › Why Inflation Hits Harder When Your Income Is Variable

This article is part of the Income Volatility Management cluster on PersonalOne — how to build financial stability when your income changes month to month.

Don Briscoe is a financial systems strategist with 12+ years of experience helping Millennials and Gen Z build income and financial stability. He founded PersonalOne to provide the financial education he wished existed — structured, honest, and free.

What You Need to Know

— Inflation reduces purchasing power for everyone, but irregular and variable income earners face a compounded version of the problem: their income gaps already create cash flow pressure, and inflation makes every gap more expensive

— The wage-to-inflation gap is structural for entry-level and gig workers — income growth has consistently lagged inflation during high-inflation periods, meaning real purchasing power falls even when nominal income stays the same

— Variable income earners need inflation-specific systems: locking fixed expenses, sizing emergency funds for both income gaps and price increases, and building expense buffers that account for inflation’s effect on irregular spending

— The two failure modes during inflation — panic spending and full paralysis — both make the situation worse; the system response is to review, adjust, and continue

— Inflation is not a reason to delay building stability systems — it is the reason those systems need to be built with more precision than a stable income earner requires

The impact of inflation hits everyone, but not equally. When prices rise faster than income, every dollar covers less ground — and the financial systems built around a previous cost baseline start showing cracks. For people with stable, predictable income, inflation is painful but manageable: the budget needs adjustment, some discretionary spending gets cut, and the system continues.

For people with variable or irregular income, inflation is a compounding problem. The income gaps that already require active management — the slow month, the delayed payment, the dropped client — now cost more to cover. The expense buffer built six months ago may no longer be sized correctly. The emergency fund calculated at last year's cost of living may not cover last year's number of months at this year's prices.

This article is specifically about that compounding dynamic — how inflation interacts with income volatility to create a more complex planning problem, and what adjustments variable income earners need to make to their systems to stay stable when both income and prices are moving at the same time. The full framework for managing this sits inside the income volatility planning system, which covers buffer architecture, account structure, and cash flow allocation for variable earners.

What Inflation Actually Does to a Variable Income System

Inflation is the rate at which the purchasing power of money declines over time. When inflation is at 3%, something that cost $100 last year costs $103 today. When inflation runs at 7–9% — as it did during the 2021–2023 period in the United States — that same item costs $107–$109. Your money buys less. Your fixed dollars cover fewer units of the same things.

For a W-2 employee on a fixed salary, this plays out as a single dimension of pressure: income stays flat, expenses rise, margin shrinks. Frustrating, but structurally simple. One variable is moving.

For a freelancer, gig worker, commission earner, or anyone on variable pay, inflation creates a two-axis problem. Axis one: expenses are rising. Axis two: income is already unpredictable. The income gaps that were already present in a normal cost environment now occur in a more expensive one. A three-week slow period that previously cost $1,800 in living expenses might now cost $2,100 for the same basic needs. The gap didn't change in duration — it changed in cost.

This is why variable income earners need inflation-specific adjustments to their systems — not just the general advice to “cut discretionary spending” that applies equally to everyone. The system adjustments are different because the problem structure is different. Anyone managing money with irregular income needs to account for both dimensions simultaneously — the income variability and the rising cost baseline — rather than treating them as separate problems.

The Wage-to-Inflation Gap and Why It Falls Hardest on Variable Earners

During periods of elevated inflation, wage growth for most workers tends to lag the inflation rate. According to Bureau of Labor Statistics data, real wages — wages adjusted for inflation — declined for a sustained period during 2021–2023 even as nominal wages increased. Workers were earning more dollars but buying less with them.

This lag effect is more acute for entry-level and variable income workers for two reasons. First, entry-level wages have less negotiating leverage — cost-of-living adjustments are more common at senior levels and in unionized environments than at the starting end of the pay scale. Second, variable income doesn't come with automatic cost-of-living adjustments at all. A freelancer's rate from two years ago is still that rate unless they actively renegotiate it. The market may have shifted, but the contract hasn't.

The practical result is that many variable income earners are absorbing inflation on two levels: their income hasn't kept pace with rising prices, and their income is still subject to the gaps and volatility that exist independent of inflation. They're being squeezed from both sides simultaneously.

The system response to the wage-to-inflation gap is not passive. It requires an active review of rates, pricing, and income floor — specifically asking whether the income baseline the current system is built around still reflects actual market rates, or whether it reflects rates set in a lower-cost environment that no longer exists. The same logic applies to workers building financial stability on a low income, where the margin between income and expenses is already thin and inflation compresses it further.

How Inflation Exposes Gaps in Variable Income Systems

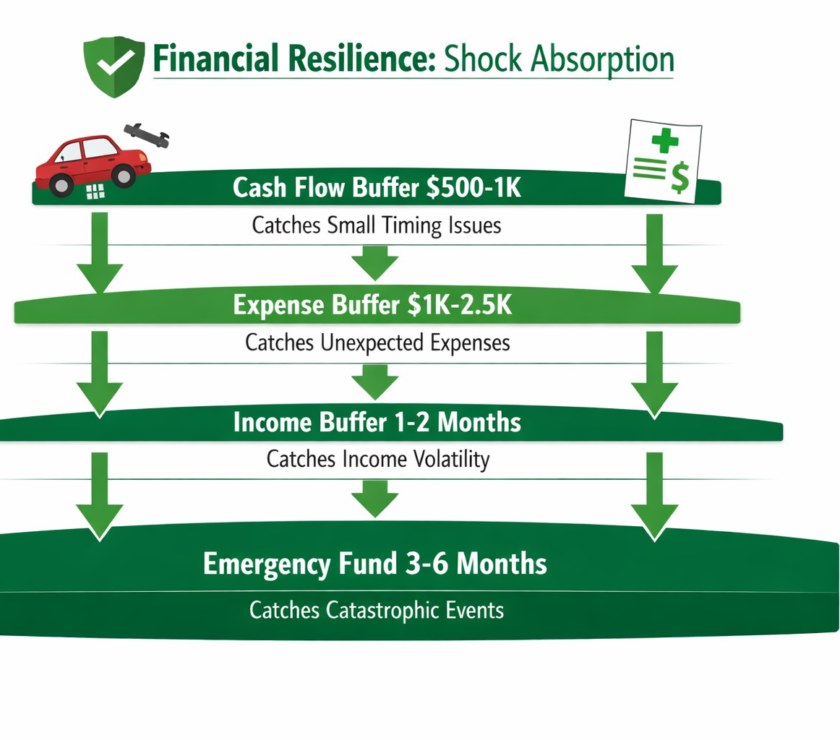

A well-built variable income system has buffers designed to cover income gaps. The income buffer covers the difference between a low-income month and normal expenses. The expense buffer covers unexpected costs. The emergency fund covers extended income disruption. These buffers are all sized against a specific cost baseline — the monthly survival expense number the system was built around.

When inflation runs at 7% annually, a system built on a $3,500 monthly survival number is now underpowered against a $3,745 monthly reality. The income buffer that could cover 1.5 months of expenses at last year's baseline may now cover only 1.2 months at this year's prices. The emergency fund calculated to provide 6 months of runway may now provide closer to 5. The buffers haven't shrunk in dollar terms — they've shrunk in coverage terms.

This is a recalibration problem, not a failure of the original system. The system was correctly built — it just needs to be updated to reflect the new cost environment. The adjustment is mechanical: recalculate the current monthly survival expense number, compare it to the number the system was built on, and determine which buffers need to be resized to restore the original coverage targets.

For most variable income earners during a sustained inflation period, this recalibration should happen annually at minimum — and more frequently during periods of rapid price change. Knowing how to build an emergency fund that protects your purchasing power is part of this: the target isn't a fixed dollar amount but a coverage number that must be adjusted as the cost environment changes.

The Two Inflation Failure Modes — and Why Both Make It Worse

When prices rise and income pressure increases simultaneously, most people shift into one of two behavioral modes. Both are understandable responses to financial stress. Both make the underlying situation worse.

Failure Mode 1 — Reactive spending: The reasoning here is that money is losing value anyway, so delaying purchases makes them more expensive later. This logic has some truth at the macro level but it's almost never the correct individual response. Accelerating discretionary spending during a period when income is already variable and buffers are underpowered depletes the cash reserves needed to cover income gaps. The inflation hedge that buying now provides is almost always smaller than the cost of being cash-poor when a slow month hits.

Failure Mode 2 — Full paralysis: The reasoning here is that everything is too expensive and uncertain to act on, so the best move is to do nothing. The problem is that doing nothing means not building or maintaining the buffers that the situation requires. An income volatility system that isn't being maintained — contributions paused, recalibration skipped, rate review delayed — degrades in real terms during an inflation period even without any active decisions to dismantle it.

The system response to inflation is neither reactive spending nor paralysis. It is a deliberate review and adjustment: recalculate the survival expense number, resize the buffers that need resizing, review income rates against current market conditions, and continue operating the system at its updated parameters. That review may be uncomfortable — it will likely surface a gap between what the system was built for and what the current environment requires — but it is the only response that actually closes the gap.

System Adjustments for Variable Income Earners During Inflation

The following adjustments are specific to variable income earners managing through a sustained inflation period. They are not a complete income volatility system — that framework lives in the income volatility planning guide — but they are the inflation-specific interventions that general personal finance advice typically doesn't address for this income type.

Recalculate your survival expense number. This is the monthly cost of your non-negotiable fixed expenses — housing, utilities, basic food, minimum debt payments, essential insurance. Inflation hits different expense categories at different rates. Recalculate this number from actual recent spending, not from a budget built in a lower-cost environment. The new number becomes the updated foundation for all buffer sizing.

Resize your income buffer against the new baseline. Your income buffer should cover 1–2 months of survival expenses during a low-income period. If inflation has raised your survival expense number, the dollar amount in your income buffer needs to increase proportionally to maintain the same coverage. A buffer that previously covered 6 weeks of expenses may now cover only 5. Rebuild to the target coverage, not the target dollar amount.

Lock fixed expenses wherever possible. Variable expenses inflate faster than locked ones. A multi-year lease at a fixed rate, a fixed-rate utility plan where available, annual subscriptions renewed before a price increase — these all protect a portion of your cost base from further inflation pressure. The goal is to reduce the percentage of your survival expenses subject to ongoing price increases. Anyone already working through a structured approach to budgeting with a variable paycheck will recognize this as the fixed expense baseline step — inflation makes getting that baseline right even more critical.

Review your income rates against the current market. If you are freelancing, consulting, or earning on a commission or variable structure, the rates you set in a previous cost environment may not reflect the current market or your current cost of living. An annual rate review — comparing your effective hourly rate to current market data and your own inflation-adjusted cost baseline — is the income-side equivalent of the expense recalibration. Both need to happen.

Maintain investing through inflation, not despite it. Pausing investment contributions during inflation because it feels financially unsafe is one of the most expensive responses available. Long-term investments in diversified index funds have historically outpaced inflation over extended periods. Stopping contributions to preserve cash that then loses purchasing power in a low-yield checking account is a net negative in most scenarios. The exception is when buffers are genuinely depleted and rebuilding them must take priority — but the goal is to restore contributions as quickly as possible once buffers are restored.

Size your emergency fund for the new cost environment. A 6-month emergency fund sized against last year's survival expense number may now represent only 5 months of real coverage. The dollar target needs periodic adjustment — not because the fund was built wrong, but because the environment it was built for has changed.

Why Inflation Is a Reason to Build Systems Sooner, Not Later

A common response to financial pressure — inflation, income volatility, or both — is to defer system-building until conditions improve. The reasoning is that there isn't enough margin right now to build buffers, so it makes sense to wait until income is higher or prices are lower before starting.

The problem with this logic is that income volatility and inflation are the conditions that buffers are built to handle. Waiting for stable conditions to build stability systems is structurally backwards. The smaller and more constrained the margin, the more important it is to deploy what exists into a system that protects it — even if the initial buffer amounts are small.

A $500 expense buffer built during a tight month provides more protection than a $0 expense buffer deferred until a better month that may not arrive on schedule. The system exists to handle conditions like the current ones — not to be built after those conditions pass.

Inflation raises the cost of not having a system in place. Every unexpected expense that goes to a credit card at 22% APR during an inflation period is doubly expensive: it costs more in nominal terms because prices are higher, and it costs more in interest terms because the debt compounds. The variable income earner who has an expense buffer absorbs that cost at zero interest. The one who doesn't absorbs it at 22%. The inflation period makes that difference larger, not smaller. The broader financial stability strategy at PersonalOne is built around exactly this principle — systems built before pressure arrives cost far less than systems built in response to it.

Build the System That Handles Variable Income and Rising Costs Together

Inflation adjustments are one layer of the variable income stability problem. For the complete framework — including how to build an income buffer, size your emergency fund for irregular pay, and create cash flow systems that hold through both income gaps and rising costs — see the full Income Volatility Management system.

Income Volatility Management →Official Sources

BLS: Consumer Price Index Data — Bureau of Labor Statistics tracking of price changes across consumer goods and services categories.

BLS: Consumer Expenditure Survey — Bureau of Labor Statistics data on how American households allocate spending across categories.

Federal Reserve: What Is Inflation and How Does the Fed Address It? — Official Federal Reserve explanation of inflation mechanics and monetary policy responses.

CFPB: Save and Invest — Consumer Tools and Guidance — Consumer Financial Protection Bureau resources on saving and investing fundamentals.

Continue Learning About Financial Stability

Managing inflation as a variable income earner is one layer of the broader stability problem. The complete framework for building systems that hold through income gaps, rising costs, and financial pressure is in the Financial Stability guide.

Frequently Asked Questions

What causes inflation and why does it keep rising?

Inflation is driven by the relationship between money supply, demand, and the availability of goods and services. Common contributors include supply chain disruptions, rising input costs (labor, materials, energy), increased consumer demand relative to supply, and monetary policy that expands the money supply faster than economic output grows. The Federal Reserve responds to inflation by raising interest rates, which increases the cost of borrowing and slows spending — but also increases the cost of variable-rate debt like credit cards and adjustable-rate loans.

How do I adjust my budget when my income is already unpredictable and prices keep rising?

Start by recalculating your actual current survival expense number from recent spending — not from a budget built months ago. Identify which expenses are fixed and which are variable. Lock fixed expenses wherever you can. For variable expenses, set category limits based on the new cost reality rather than the previous one. The goal isn't to spend less on everything — it's to know exactly what you need to cover each month at current prices, so your income buffer is sized correctly for the actual environment.

Should I still invest if my income is variable and inflation is high?

Yes, with one structural prerequisite: your income buffer and starter expense buffer should be in place before you direct surplus income to investments. This isn't about investing being wrong during inflation — it's about sequencing. If your buffers are depleted and you face an income gap, you'll liquidate investments to cover it, often at a loss. Once buffers are funded, investing during inflation is correct — diversified long-term holdings have historically outpaced inflation over extended periods, and stopping contributions to hold cash that loses purchasing power is a worse outcome for most people.

How does inflation affect my emergency fund target?

Your emergency fund target is calculated as a number of months of survival expenses. If inflation has increased your monthly survival expenses, the dollar amount needed to cover the same number of months has also increased. Review your emergency fund target annually — or more frequently during periods of rapid price change — by recalculating your current survival expense number and multiplying by your target months of coverage. The fund may need to grow even if you haven't used any of it.

When should a freelancer or gig worker raise their rates to keep up with inflation?

An annual rate review is the baseline — comparing your effective hourly or project rate to current market data for your skill set and experience level. If your rate was set during a lower-cost environment and hasn't been reviewed since, it may be below both market rate and your own inflation-adjusted income needs. The review doesn't require raising rates immediately, but it should result in a clear picture of whether your current rate covers your current cost baseline with adequate margin — or whether a conversation with clients about rate adjustments is warranted.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. PersonalOne is not a licensed financial advisor, broker, or investment professional. Individual financial situations vary — consult a qualified financial professional for personalized guidance.