June 27, 2026

June, 2026

Home › Credit, Banking & Cash Flow › Banking Structure & Cash Flow Control › The Account Separation Strategy That Prevents Financial Chaos

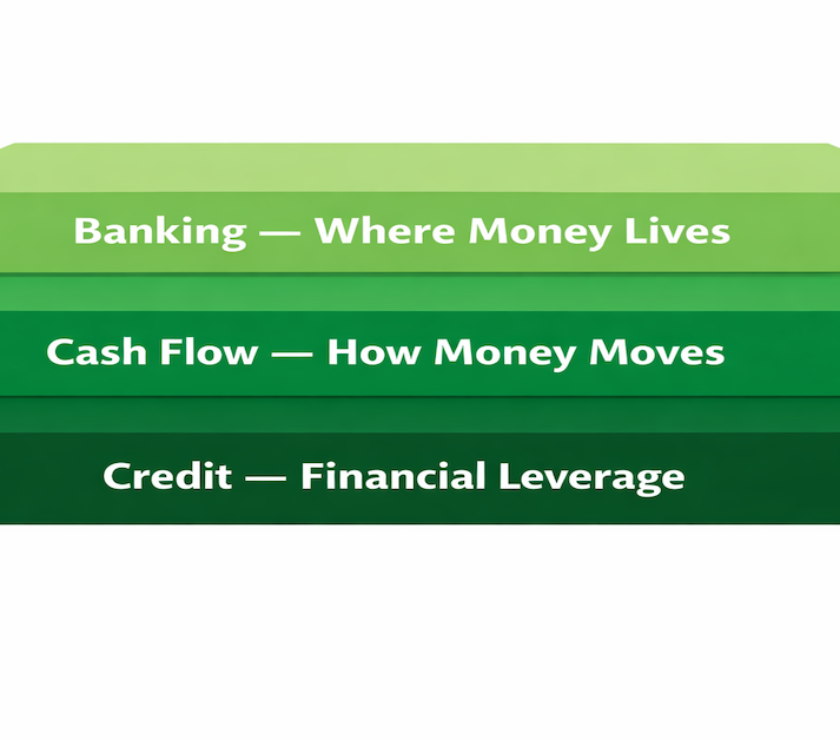

This article is part of the Banking Structure & Cash Flow Control cluster on PersonalOne — the foundation layer of the integrated credit-banking-cash flow system.

Sucy Griffin is a financial strategist with 10+ years of experience designing financial health systems that strengthen credit, stabilize cash flow, and build long-term financial security. She specializes in translating complex financial decisions into practical frameworks that produce real, measurable outcomes. Follow

What You Need to Know

— The account separation strategy routes different categories of money to dedicated accounts so that the balance in each account accurately represents what is available for that purpose.

— The minimum viable structure is three accounts: a bills account, a spending account, and a savings account — with automated transfers routing money to the correct destination on payday.

— Implementation takes one session to set up and runs automatically from that point forward, requiring no ongoing management or mental tracking.

— The result is a financial system where bills are covered by design, spending is bounded by visible account balance, and savings happen before spending decisions are ever made.

— The full banking structure and cash flow control framework is the complete cluster this strategy is part of.

The account separation strategy is the practical implementation of the insight that account structure controls financial outcomes. It takes the problems documented across this cluster — the fungibility failure of a single checking account, the hidden cash flow problem created by mixing committed and discretionary money, and the way invisible category conflicts produce consistent financial instability — and resolves all of them with one structural change to how bank accounts are organized and how money flows between them.

This article is the implementation guide. It covers the specific account structure, the automation rules that make it run without ongoing management, the transition process for moving from a single-account setup, and the variations that address common household scenarios including variable income, irregular expenses, and multiple income earners.

The Core Account Structure

The minimum viable account separation structure for most households uses three accounts, each serving a distinct and non-overlapping purpose.

Account 1: The Bills Account. This account receives all income — direct deposits, transfers, any source of money — and pays all fixed recurring obligations. Rent, mortgage, utilities, insurance premiums, minimum debt payments, and any other fixed monthly expense processes from this account via autopay. The bills account is not a spending account. No discretionary purchases are made from it. Its only purpose is to ensure that every committed obligation is covered reliably, automatically, and without competition from spending money.

Account 2: The Spending Account. This account receives a fixed transfer from the bills account on payday — the discretionary budget for the period. All variable, discretionary spending happens from this account: groceries, dining, clothing, entertainment, transportation beyond fixed costs. The balance in the spending account at any point is the accurate, honest answer to “how much can I spend?” When it reaches zero, spending stops. No mental math, no category tracking, no budgeting app required.

Account 3: The Savings Account. This account receives an automated transfer on payday — processed before any spending money moves to the spending account. The savings transfer happens before the discretionary budget is visible or available, which removes the savings decision from the monthly spending environment entirely. The savings account is not easily accessible for daily spending, which creates natural friction against treating it as overflow spending money.

The Automation Rules That Make It Run

The account separation strategy is only as effective as the automation that routes money to the correct accounts on payday. Manual transfers defeat the purpose because they require a decision each pay period — and decisions are subject to all the cognitive patterns that make financial management inconsistent. Automation removes the decision entirely. Money goes where it is supposed to go before any spending decisions are available to compete with it.

The automation sequence runs in this order on payday: income arrives in the bills account first. An automated transfer moves the savings allocation to the savings account immediately — savings happen before spending. A second automated transfer moves the discretionary budget to the spending account. What remains in the bills account after both transfers is the bills reserve — the money designated for fixed obligations that will process throughout the month.

Most banks allow scheduled recurring transfers to be set up through the online banking interface. Setting up the two transfers takes roughly 15 minutes. From that point, the system runs on every pay cycle without any manual action required. The FDIC’s Money Smart program identifies automated savings and bill payment as the single most effective behavioral intervention for improving household financial stability — because the automation ensures the behavior happens regardless of what else is happening in life that week.

Calculating the Transfer Amounts

Setting the correct transfer amounts is the most important configuration decision in the separation strategy. The calculation is straightforward but requires accurate data about monthly obligations and income.

Bills account reserve calculation: List every fixed monthly obligation with its amount and due date. Sum the total. Add 10% as a buffer for irregular fixed expenses like annual renewals and quarterly charges prorated monthly. This is the minimum balance the bills account must maintain throughout the month to cover all obligations reliably. The remainder after savings transfer and spending transfer remains in the bills account as this reserve.

Savings transfer amount: Start with a specific target — a dollar amount, not a percentage wish. If the goal is a $3,000 emergency fund in 12 months, the required transfer is $250 per month or $125 per biweekly pay period. Set the automation at that specific amount. The CFPB recommends consistent automated savings as the most reliable method for achieving savings goals because it removes the monthly decision about whether to save and how much.

Spending transfer amount: Monthly take-home income minus total monthly obligations minus monthly savings transfer equals the monthly discretionary budget. Divide by pay periods per month for the per-period transfer amount. This number is the honest answer to “how much can I spend?” per pay period. Set the automation at this amount.

Account separation is the foundation. The full integrated system connects it to cash flow timing and credit optimization.

Once the account structure is designed and automated, the next layer — how cash flow timing affects credit utilization — builds directly on top of it. The complete integrated money system is in the hub.

Explore the Full Credit, Banking & Cash Flow System →Implementing the Transition From a Single Account

Moving from a single checking account to a separated structure requires a one-time setup process that should be completed in a single session to avoid a period of parallel confusion between old and new systems.

Step 1: Open the spending account and savings account if they do not exist. Many banks allow this within existing online banking without a branch visit. Accounts at the same institution make the initial automated transfer setup simpler, though the spending account can be at a different institution if additional friction against transferring from savings is desired.

Step 2: Leave direct deposit pointed at the bills account. Do not change the deposit destination — income continues to arrive where it always has. Only the outgoing transfers change.

Step 3: Set up the two automated transfers — savings transfer and spending transfer — timed for the same day as the direct deposit or the following business day. Allow 48 hours of buffer from deposit to transfer to account for any variation in deposit timing.

Step 4: Over the first full month, use only the spending account for all discretionary purchases and observe whether the transfer amount reflects your actual discretionary needs accurately. Adjust the transfer amount based on one month of real data if needed. The initial calculation is an estimate — real-world calibration against actual spending patterns sharpens it.

The transition period also connects directly to the broader cash flow problem and budget-breaking mechanisms covered earlier in this cluster — once the structure is in place, both problems disappear structurally rather than requiring ongoing management.

Variations for Common Household Scenarios

Variable income: Add a fourth account — a holding account that receives all income first. From the holding account, transfer a consistent “salary equivalent” to the bills account on a regular schedule regardless of what income arrived in a given period. The holding account absorbs income variability and smooths it into consistent cash flow that the three-account structure can handle predictably. Build the holding account to a two-month income buffer before switching to this system.

Irregular large expenses: Add a sinking funds account for predictable irregular expenses — car registration, annual insurance renewals, holiday gifts. Calculate the annual total of these expenses, divide by 12, and include that monthly amount in the bills account reserve or set up a separate automated transfer. When the expense arrives, the money is already waiting rather than creating a sudden shortfall.

Two incomes: The structure remains the same. Both incomes route to the bills account. The transfer amounts are calculated against combined income. If one partner manages a subset of expenses independently, a fifth account can be added to route that partner’s discretionary allocation separately — but the bills account remains the single point of income receipt and obligation coverage to maintain visibility over the full household cash flow.

Resources

FDIC — Money Smart Financial Education Program

CFPB — How to Create a Budget and Stick With It

CFPB — Track Your Spending With This Easy Tool

Federal Reserve — Survey of Consumer Finances

This article is part of the Credit, Banking & Cash Flow integration system on PersonalOne — the complete framework for building a personal finance infrastructure that runs reliably by design.

Frequently Asked Questions

What if my spending transfer is not enough some months?

Recalibrate after one full month of real data. The initial transfer amount is calculated against estimates of discretionary spending — real behavior rarely matches estimates exactly on the first attempt. After one month, compare the spending account usage to the transfer amount and adjust upward if genuinely necessary, or use the gap as data to identify which discretionary category is consistently over-allocated. The month of real data is more valuable than any estimate, and one month of calibration typically produces an accurate transfer amount that holds indefinitely.

Should the spending account be at the same bank as the bills account?

There are advantages to both. Same institution: transfers are instant or same-day, which is convenient for topping up the spending account when the monthly transfer is set too low initially. Different institution: transfers take one to two business days, which adds natural friction against impulse transfers from bills or savings into spending. The friction is a feature for some households — it creates a natural pause before any unplanned spending that would require pulling from another account. Choose based on which characteristic is more valuable for your specific behavioral patterns.

How does this affect credit card usage?

Positively, through two mechanisms. First, reliable on-time bill payments from the dedicated bills account improve payment history, which is the most significant factor in credit scoring. Second, paying credit card balances from the spending account — where the balance accurately represents available money — prevents the pattern of carrying balances that feel manageable against a misleading single-account balance but exceed the actual discretionary budget. Many households find that account separation reduces credit card usage significantly simply because the spending account makes the budget boundary visible in real time.

Is this the same as the envelope budgeting method?

It is the digital infrastructure version of the envelope method — same principle, different implementation. The envelope method assigns physical cash to labeled envelopes for each spending category, which makes the category boundary visible and concrete. Account separation does the same thing with bank accounts rather than physical envelopes, which is more practical for electronic payments and eliminates the cash handling requirement. Both methods work because they make the category distinction physical rather than mental — the specific implementation matters less than the structural separation it creates.

Disclaimer: This content is for educational purposes only and does not constitute financial advice. Individual financial situations vary — consult a qualified financial professional for personalized guidance.