July 6, 2026

July 2026

Home › Credit, Banking & Cash Flow › The Financial Infrastructure System › How Credit, Banking & Cash Flow Actually Work Together Explained

This article is part of the Financial Infrastructure System cluster on PersonalOne — the integrated model that connects banking structure, cash flow design, and credit behavior into one personal finance system.

Sucy Griffin is a financial strategist with 10+ years of experience designing financial health systems that strengthen credit, stabilize cash flow, and build long-term financial security. She specializes in translating complex financial decisions into practical frameworks that produce real, measurable outcomes. Follow

What You Need to Know

— Credit, banking, and cash flow are not three separate topics — they are three layers of one financial infrastructure system, and each layer directly affects the others.

— Your account structure controls how money moves. How money moves controls whether obligations are met reliably. Whether obligations are met reliably controls what your credit profile looks like.

— The connection runs in both directions: credit behavior affects borrowing costs, which affects cash flow, which affects what banking structure is needed to manage it.

— Most financial problems that feel like isolated issues — a low credit score, a cash flow squeeze, a budget that never holds — are system problems with system solutions.

— The financial infrastructure system is the framework that connects all three layers into a single integrated design.

The financial infrastructure system that governs most household financial outcomes is made up of three interdependent layers: banking structure, cash flow management, and credit behavior. These three areas are almost always taught and discussed as separate subjects — credit scores in one article, budgeting in another, account types in a third. But in practice they operate as one connected system, and the most important financial improvements come from understanding how changes in one layer ripple through the others.

This article maps the actual relationships between the three layers — not as theory, but as a practical framework for diagnosing why financial problems recur and what structural changes resolve them at the root rather than at the symptom.

Layer One: Banking Structure Sets the Foundation

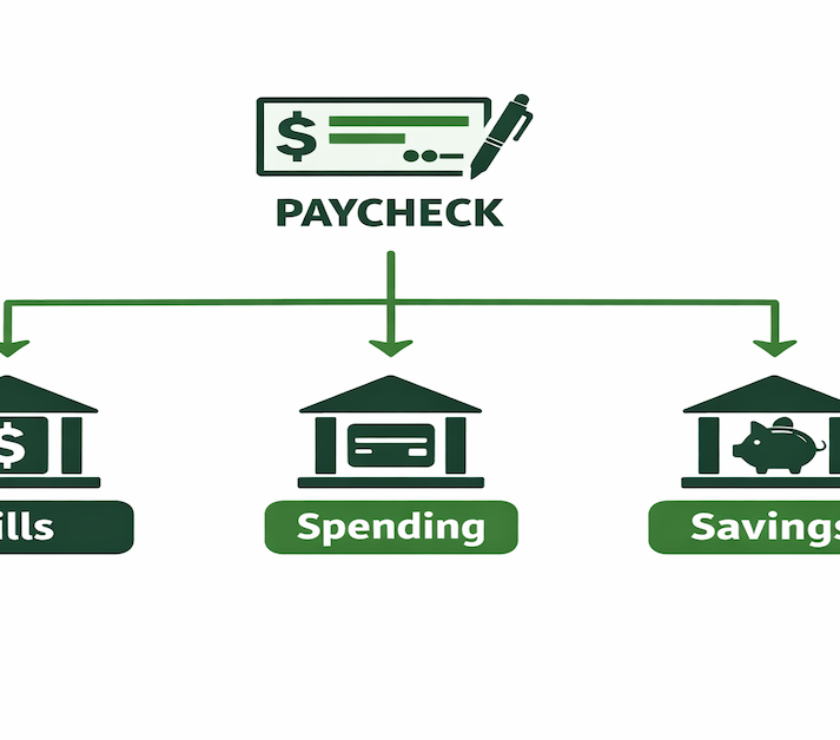

Banking structure is the account design that determines how money flows through a household. It includes how many accounts are maintained, which types of money route to which accounts, how transfers between accounts are automated, and what financial behaviors happen by default before any conscious spending decision is made.

The account structure layer is foundational because it determines the information available to every other financial decision. A single checking account that mixes committed bill money with discretionary spending money produces misleading balance information that leads to overspending against committed funds. A properly separated structure routes each category of money to its dedicated account, making the available-to-spend balance accurate at any point in the month without requiring mental tracking.

As covered in the banking structure and cash flow control cluster, the account design layer is the highest-leverage infrastructure change most households can make — because every other financial behavior runs on top of it. Getting it wrong makes everything else harder. Getting it right makes many other improvements happen automatically.

Layer Two: Cash Flow Management Controls Money Movement

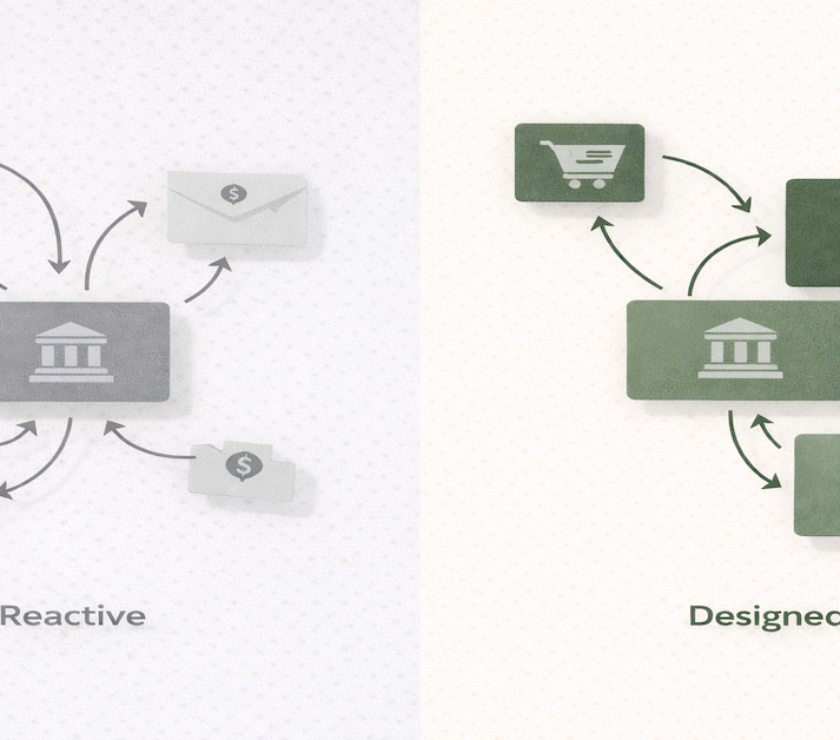

Cash flow management is the system that governs how money moves between income arrival and obligation coverage — the timing, sequencing, and routing of funds through the banking structure. It is not just about budgeting categories. It is about the specific mechanics of when money moves, where it moves to, and what financial events happen as a result.

Cash flow problems are almost always timing and visibility problems rather than income problems. The household that runs short the week before payday despite technically adequate income is not experiencing an income problem — it is experiencing a cash flow design problem. The money exists, but the account structure and routing decisions create conditions where committed funds and spending funds are invisible from each other, producing consistent shortfall at predictable points in the pay cycle.

The connection between cash flow management and credit behavior is direct: cash flow timing determines when credit card payments are made, which determines what balance is reported at statement close, which determines utilization, which affects the credit score. A household with excellent cash flow design — bills covered automatically, pre-statement payments funded reliably, no timing gaps between income and obligations — will produce a consistently better credit profile than a household with identical spending habits and a poorly designed cash flow system.

Layer Three: Credit Behavior Creates the Long-Term Financial Profile

Credit behavior — payment history, utilization, account age, and credit mix — produces the credit profile that governs borrowing costs for every major financial decision over the next decade. The interest rate on a mortgage, the terms of an auto loan, the credit limits offered on new accounts, and the cost of any financing product are all functions of the credit profile established through years of credit behavior.

The connection from credit behavior back to cash flow is equally direct. A credit profile that produces a low interest rate on a mortgage reduces the monthly payment on that mortgage, which frees cash flow capacity for savings, investment, or debt payoff. A credit profile that produces a high interest rate does the opposite — it increases the fixed obligation load, which tightens cash flow, which creates more pressure on the banking structure to manage obligations reliably. Credit behavior affects borrowing cost. Borrowing cost affects cash flow. Cash flow affects what banking structure is needed. The system is circular.

Three layers. One system. The framework that connects them is the starting point.

The financial infrastructure system cluster covers the complete integrated model — how to design all three layers to work together and what the full architecture looks like when it is functioning correctly.

Explore the Financial Infrastructure System →Why Fixing One Layer in Isolation Produces Limited Results

Most financial advice addresses one layer at a time. Credit repair advice focuses on payment history and utilization without addressing the banking structure and cash flow design that would make those behaviors automatic rather than effortful. Budgeting advice focuses on spending categories without addressing the account architecture that determines whether the budget can be maintained in practice. Banking advice focuses on account types and fees without connecting account design to credit behavior and cash flow outcomes.

The result is partial improvements that do not hold. A credit score that improves temporarily when attention is paid to utilization but reverts when attention moves elsewhere. A budget that works for two months and then breaks down when the structure supporting it was never actually built. An account consolidation that feels simpler but removes the separation that was preventing bill money from competing with spending money.

The financial infrastructure most people never build is the integrated design that treats all three layers as one system. That integration is what produces financial improvements that compound rather than reverting — because each layer reinforces the others rather than operating in isolation.

Resources

CFPB — How to Create a Budget and Stick With It

CFPB — Credit Reports and Scores

Federal Reserve — Survey of Consumer Finances

FDIC — Money Smart Financial Education Program

This article is part of the Credit, Banking & Cash Flow integration system on PersonalOne — the complete framework for building a personal finance infrastructure that runs reliably by design.

Frequently Asked Questions

Why does my credit score keep fluctuating even when I am not doing anything differently?

Fluctuation in the absence of deliberate changes usually means the cash flow layer is producing inconsistent utilization reporting. If spending patterns vary month to month, the balance at statement close varies, which varies the utilization reported, which varies the score. The fix is not credit-focused — it is cash flow design. A pre-statement payment that runs automatically each month produces consistent low utilization at statement close regardless of how spending varied during the period.

Can I improve my credit score just by changing my banking structure?

Indirectly, yes — and sometimes significantly. A banking structure that separates bill money from spending money makes on-time bill and credit card payments automatic rather than effortful. On-time payment history is the largest factor in credit scoring. A structure that includes a pre-statement payment automation reduces reported utilization, the second largest factor. Together these two structural changes produce the two most important credit behaviors without requiring ongoing willpower or attention — which means they sustain over time rather than improving temporarily when focus is applied and reverting when it moves elsewhere.

What should I fix first: my credit, my banking structure, or my cash flow?

Banking structure first, in almost every case. It is the foundation that makes the other two improvements durable. A credit repair effort without the supporting banking structure requires ongoing effort to maintain. A cash flow improvement without the account separation that makes it visible produces improvements that erode as the mental accounting that is trying to track categories inevitably fails. Fix the account structure first, automate the basic cash flow routing, and the credit improvements will follow as a downstream consequence of better bill payment reliability and lower statement-date utilization.

Disclaimer: This content is for educational purposes only and does not constitute financial advice. Individual financial situations vary — consult a qualified financial professional for personalized guidance.