June, 2026

Home › Credit, Banking & Cash Flow › The Financial Infrastructure System › The Financial Infrastructure Most People Never Build

What You Need to Know

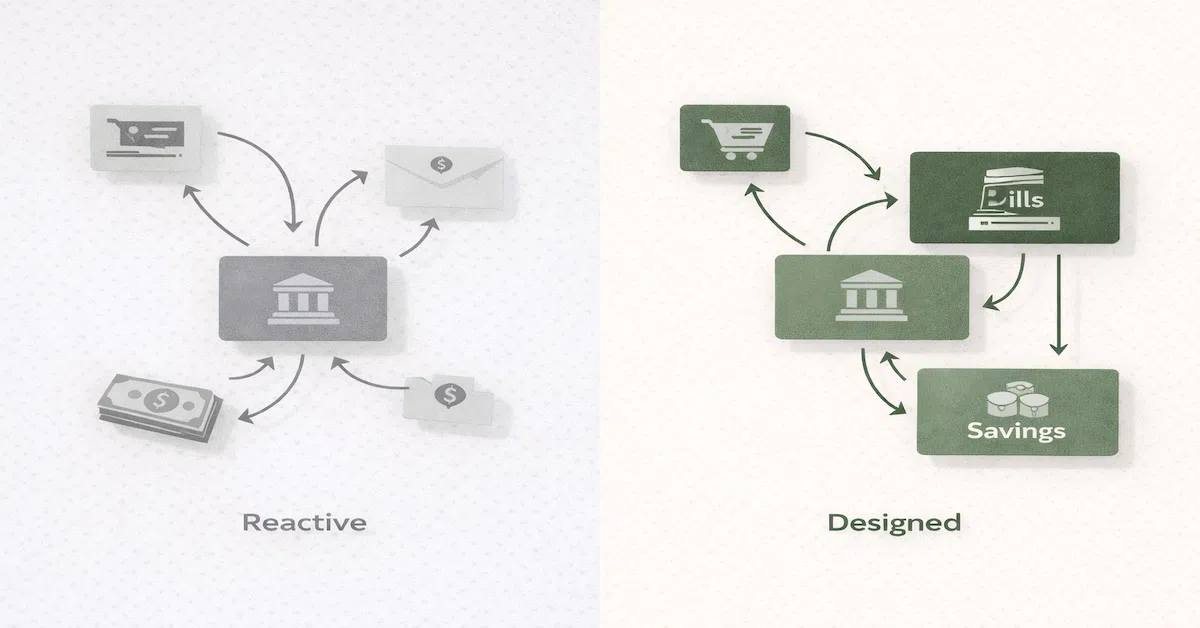

— Most people manage money reactively — responding to what happened rather than operating from a designed system that produces the right outcomes by default.

— The integrated money management system that produces lasting financial stability is built once and then runs — it does not require ongoing active management to maintain its results.

— The reason most people never build it is not a lack of knowledge or willpower. It is a lack of a clear model showing what the complete system looks like and how to assemble it.

— The system has three layers that must be built in the right order: account infrastructure first, cash flow routing second, credit optimization third.

— Each layer of the integrated money management system is covered in detail across this cluster.

The integrated money management system that produces consistent financial stability — reliable bill coverage, growing savings, improving credit, predictable cash flow — is not a complicated system. It is a designed system. The distinction matters because the failure mode for most household finances is not complexity. It is the absence of design. Money arrives, gets spent against an undifferentiated account balance, and the outcomes are reactive rather than intentional.

The financial infrastructure most people never build is the set of account structures, automation rules, and routing decisions that make the right financial behaviors happen by default rather than by ongoing effort. It is not a strategy for getting rich quickly. It is the plumbing that makes every other financial goal achievable — and most people never build it because nobody has ever shown them what it looks like as a complete system.

Why Most People Manage Money Reactively

Reactive money management is the default state for households that have not deliberately designed their financial infrastructure. It looks like this: income arrives, current obligations get paid, the remaining balance gets spent across categories without a clear allocation system, and the month ends either with a small surplus or a small deficit depending on whether any unexpected expense appeared. Next month, the same sequence repeats.

This approach is not irrational. It is the natural behavior that emerges when there is no designed system to follow. People respond to visible information — the account balance, the due date, the bill that just arrived — rather than operating from a forward-designed framework that allocates money before any of those events requires a response.

The Federal Reserve’s consumer financial research consistently documents the outcomes of reactive versus designed money management. Households that automate savings and bill payments — the two most basic elements of a designed system — accumulate significantly more wealth and maintain better credit profiles than households with equivalent incomes that manage money manually and reactively. The difference is not income. It is the presence or absence of a system.

What the Infrastructure Actually Consists Of

The personal finance infrastructure that most people never build has three layers, each of which must be assembled in order because each layer provides the foundation for the next.

Layer 1: Account infrastructure. The account design that separates committed money from discretionary money, routes savings before spending, and makes the available balance in every account an accurate representation of what that account is for. This is the foundation layer. Without it, the cash flow routing layer has no stable architecture to run through, and the credit optimization layer has no reliable payment timing to work with. The banking structure and cash flow control cluster covers this layer in full.

Layer 2: Cash flow routing. The automation rules and transfer schedules that move money through the account infrastructure at the right times — savings on payday, bill reserves protected, spending account funded with the accurate discretionary amount, credit card pre-statement payments timed before statement close. This layer converts the account structure from a static design into a dynamic system that runs each pay cycle without manual intervention.

Layer 3: Credit optimization. The payment timing strategy that uses the cash flow layer to manage what utilization gets reported to the credit bureaus each month. Pre-statement payments funded from the bills account, timed relative to each card’s statement close date, producing consistently low utilization without reducing spending capacity. This layer is built on top of Layers 1 and 2 — it cannot be reliably maintained without them.

The Reason It Never Gets Built

The reason most people never build this infrastructure is not discipline failure or lack of financial knowledge. It is the absence of a clear, complete model of what the system looks like when it is assembled correctly. Financial education covers individual topics — credit scores, budgeting methods, savings accounts — without showing how they connect into a single designed system. People understand the pieces but not the architecture.

The result is partial implementation. Someone opens a savings account but does not automate transfers to it, so saving remains inconsistent. Someone learns about credit utilization but does not build the cash flow routing that makes pre-statement payments sustainable, so utilization management requires active monthly attention that eventually lapses. Someone builds a budget but does not build the account separation that makes it enforceable, so the budget works until a busy or stressful month breaks the mental accounting it depends on.

Partial implementation produces partial results that feel like confirmation that better financial management is not possible for their situation — when the actual cause is that the system was never fully assembled. The complete personal finance infrastructure model provides the architectural view that makes full assembly possible.

The system exists. It is buildable. The framework shows you exactly how.

The financial infrastructure system cluster is the complete model — from account design through cash flow routing to credit optimization — with every layer documented in the order it needs to be built.

Explore the Financial Infrastructure System →What Changes When the Infrastructure Is in Place

The most immediate change when the account infrastructure is properly built is a reduction in financial stress — not because the income increased, but because the uncertainty about whether obligations are covered disappears. When bills are routed to a dedicated account that is not accessible for spending, and that account balance represents exactly the money reserved for obligations, the question “will I be able to cover everything this month?” has a clear and visible answer at all times. That clarity reduces the cognitive load of financial management significantly.

The medium-term changes are in credit profile and savings accumulation. Automated savings that happen on payday before discretionary money is visible accumulate consistently regardless of what else is happening in the household. Pre-statement payments that run automatically each month produce steadily lower reported utilization and a credit score trajectory that improves gradually without requiring ongoing attention. Both improvements compound over time in ways that reactive money management cannot replicate.

Understanding why budgeting fails without banking structure is the entry point for households that have tried budgeting approaches without the underlying account infrastructure and experienced the predictable pattern of temporary improvement followed by reversion. The infrastructure is what makes the budget permanent rather than temporary.

Resources

Federal Reserve — Survey of Consumer Finances

CFPB — How to Create a Budget and Stick With It

FDIC — Money Smart Financial Education Program

This article is part of the Credit, Banking & Cash Flow integration system on PersonalOne — the complete framework for building a personal finance infrastructure that runs reliably by design.

Frequently Asked Questions

How long does it take to build the complete infrastructure?

The account structure layer takes one session to set up — opening the additional accounts and configuring the automated transfers is typically a 30 to 60 minute task. The cash flow routing layer is configured at the same time. The credit optimization layer requires knowing your statement close dates and setting up pre-statement payment automation, which takes another session once the bills account is established. The full system can be assembled in two to three hours spread across two sessions. After that, it runs automatically without requiring significant ongoing time investment.

Do I need to be debt-free before building this system?

No — and waiting until debt is cleared before building the infrastructure delays the system that would most help with debt payoff. Debt payoff is more effective when it is built into the infrastructure as a dedicated allocation — an automated minimum-plus-extra payment from the bills account that runs every cycle without requiring a monthly decision about whether to make the extra payment. The infrastructure supports debt elimination rather than competing with it.

What income level does this system require?

The system design scales to any income level. The principle — separating committed money from discretionary money, automating savings before spending, managing credit payment timing relative to statement dates — applies at $35,000 per year and at $135,000 per year. The dollar amounts in each account are different, but the architecture is identical. Lower income levels benefit from the structure as much or more than higher income levels, because the margin for error is smaller and the cost of unmanaged cash flow is proportionally higher.

Disclaimer: This content is for educational purposes only and does not constitute financial advice. Individual financial situations vary — consult a qualified financial professional for personalized guidance.