March 23, 2026

Updated: May 14, 2026

Home › Banking Systems & Account Structure › Paycheck Money Flow Design › Should Your Paycheck Go to Checking or a Bills Account?

This article is part of the Paycheck Money Flow Design cluster on PersonalOne.

Don Briscoe is a financial systems strategist with 12+ years of experience helping Millennials and Gen Z build income and financial stability. He founded PersonalOne to provide the financial education he wished existed — structured, honest, and free. Follow

What You Need to Know

— Where your paycheck lands first determines your default behavior with money. Landing in checking makes spending the path of least resistance. Landing in a bills account makes obligations the path of least resistance.

— Neither approach is inherently right. The question is which one matches the account structure and money flow system you're trying to build.

— A third option — splitting direct deposit at the source — eliminates the landing decision entirely by routing money to its final destination before it ever sits anywhere as a lump sum.

— This decision can and should evolve as your system matures. Most people start with checking and migrate toward splitting or bills-first as their account structure becomes more deliberate.

— Where your paycheck lands matters far less than what happens in the 48 hours after it lands. The system that distributes money to the right places automatically is more important than the landing zone itself.

Most people never consciously decide where their paycheck lands. They filled out a direct deposit form when they started their job, selected their checking account, and haven't thought about it since. That default choice — paycheck to checking — works fine as a starting point. But as a permanent structure it has a specific behavioral consequence that most people don't recognize until they start actively managing their money: when your paycheck lands in your spending account, spending is always the path of least resistance.

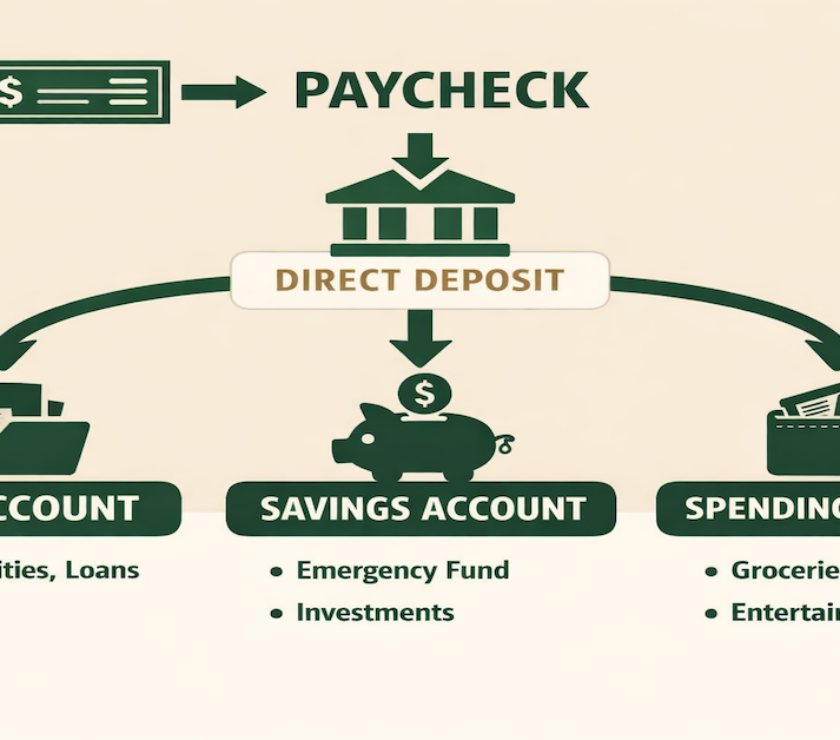

The question of whether your paycheck should go to checking or a bills account is really a question about what the default behavior of your money system should be. Whether the answer is paycheck to checking or bills account depends entirely on which account structure you're operating — and what outcome you're trying to produce. This article covers the three approaches, the specific scenarios where each one works best, and the decision framework for choosing the right landing zone for your current system.

The Core Distinction: What Your Landing Zone Does to Default Behavior

The landing account — the account that receives your direct deposit — doesn't just hold your money temporarily. It sets the default path for everything that happens next. This behavioral reality is the most important concept in the entire landing zone decision and the one that never appears in standard banking advice.

When Checking Is the Landing Zone

When your paycheck lands in your primary checking account, spending is immediately available. Your balance reflects the full paycheck — which looks like spendable money, because it's sitting in the account you use to spend. Bills still need to be paid from that pool, which means bills and discretionary spending compete for the same dollars. If you transfer to a bills account after landing, you're relying on the discipline of remembering to do it — and doing it before spending depletes the balance. The system works when the discipline is consistent. It creates friction when the discipline lapses.

When a Bills Account Is the Landing Zone

When your paycheck lands in a dedicated bills account, obligations are protected the moment income arrives. Bills pay automatically from the account that just received the paycheck. What remains after bills is genuinely discretionary — not dollars that look available but actually belong to an upcoming payment. The system creates structural protection for obligations without requiring active discipline. The trade-off is that spending requires an intentional transfer rather than being immediately available. For people who benefit from that friction — whose financial history includes spending bill money before bills were paid — the structure is the solution.

When Direct Deposit Splitting Is the System

Direct deposit splitting eliminates the landing zone question entirely. Your employer splits the deposit at source — a fixed amount to the bills account, a fixed amount to savings, and whatever remains to spending. Money arrives pre-allocated and never exists as one lump sum waiting for distribution. This is the most structurally complete approach because it removes the behavioral variable altogether — there is no pool of money to make decisions about because the decision was already made at payroll. The full system for designing paycheck flow from source allocation through final distribution is covered in the guide on how to design your paycheck money flow.

What I've Seen

The most consistent pattern I see with people who are frustrated that their money "disappears" each month is that their paycheck lands in the same account they use for daily spending. The money looks available — because it is available — and it gets spent. Bills get paid, but only because they happen to be in the queue before the balance runs low. There's no structural protection for obligations, just a race between bills and spending that the person usually wins by a narrow margin. When the same person switches to landing their paycheck in a bills account and transfers spending money out after bills are funded, the "disappearing money" problem resolves in the first cycle. Nothing else changed — not the income, not the bills, not the spending habits. The structure changed. That's the entire difference.

Approach 1 — Paycheck to Checking: When It Works and When It Doesn't

Checking account landing is the default for most people — and the right choice in several specific situations. The key is understanding which situations those are and recognizing when you've outgrown the approach.

When Checking Landing Works Best

Your checking account is your spending account. If you're operating a simple one or two-account system where checking handles both income and daily expenses, landing in checking is correct. You're not trying to separate spending from income — they're the same pool by design. The approach only creates problems when you're trying to protect obligations from spending but the money is all in the same place.

You have variable income. Freelancers, contractors, and commission earners whose income varies significantly each cycle often benefit from seeing the full deposit in one place before making allocation decisions. When income is unpredictable, automated distribution to fixed amounts doesn't account for low-income months. Seeing the full amount in checking first — then manually deciding how much goes to bills, savings, and spending based on what actually arrived — gives the flexibility that variable income requires. The specific system for routing variable income across multiple accounts without creating cash flow problems is covered in the article on how to route variable income into multiple accounts.

You're in a transitional phase. When you're first building a multi-account system — figuring out the right allocation amounts, testing whether the bills account covers everything, calibrating the buffer — landing in checking while you fine-tune the system is reasonable. The checking landing keeps everything visible and flexible while you establish stable allocation amounts. Once the system stabilizes, the landing zone decision becomes clearer.

The Disadvantages of Checking Landing

Bills and discretionary spending compete for the same pool of money — and spending is immediately available in a way that feels natural. Transferring to a bills account after landing requires consistent discipline to execute before spending depletes the balance. The balance always looks "spendable" even when a portion of it belongs to an upcoming payment. For people whose financial history includes tight months where bills got paid but only just, or where savings transfers consistently got skipped because the balance looked low, checking landing perpetuates the conditions that create that pattern.

Approach 2 — Paycheck to Bills Account: When It Works and When It Doesn't

Bills account landing is the more structurally deliberate approach — and the one that produces the most consistent bill payment outcomes for people who have previously struggled with money arriving in one place and bills competing with spending for it.

When Bills Account Landing Works Best

You've experienced bill payment anxiety or late payments. If your financial history includes months where bills were paid late because spending happened first, bills account landing resolves the structural cause of that pattern. Bills are funded the moment income arrives — before any spending is possible — because the money is in the account the bills pull from. The anxiety of watching a checking balance and wondering whether bills will clear disappears when the bills account is funded independently of spending decisions. A well-designed bills account system — including what belongs in it, how much buffer to maintain, and how to prevent overdrafts — is covered in the article on the bills system that helps prevent overdrafts.

Your bills total is stable and predictable. Bills account landing works best when you know exactly how much your monthly obligations total. A stable bills number — rent or mortgage, utilities within a known range, fixed subscriptions, minimum debt payments — means you can calculate precisely how much the bills account needs to cover and verify that the incoming paycheck covers it. When the bills total is stable, the landing zone protects a known amount automatically each cycle.

You want obligations protected before discretionary spending. The philosophical position that obligations come before discretionary spending — rent before restaurants, utilities before entertainment — is only enforceable through structure if the landing zone reflects that priority. Landing in bills makes it physically impossible to spend before obligations are covered. Landing in checking makes that priority aspirational rather than structural.

The Disadvantages of Bills Account Landing

Bills account landing requires a dedicated bills account to exist and be set up correctly before the landing zone switch makes sense. Changing your direct deposit to a bills account that isn't yet calibrated — that doesn't cover all your bills, lacks a buffer, or has autopay timing issues — creates the opposite of the intended outcome. The bills account needs to be operational and tested before it becomes the income landing zone. If you don't have a functioning bills account yet, starting there is the prerequisite step before any landing zone decision.

Approach 3 — Direct Deposit Splitting: The Structural Automation Solution

Direct deposit splitting is available from most employers and eliminates the landing zone question by routing money to its final destination before it arrives anywhere as a combined sum. Your payroll department splits the deposit at source — a specific dollar amount or percentage to each account — and the money arrives pre-allocated.

How to Set It Up

Contact your employer's payroll or HR department and request a split direct deposit form. Most employers support splitting across two or three accounts. You specify either a fixed dollar amount or a percentage for each account. A typical setup: bills account receives the monthly bills total, savings account receives the fixed savings amount, and checking receives whatever remains as spending money. The split takes effect within one to two pay cycles. Adjusting allocation amounts — when bills change, when savings goals change — requires updating the form with payroll.

When Splitting Works Best

Direct deposit splitting works best for W-2 employees with stable, predictable income and a clear understanding of their monthly bills total and savings target. When those two numbers are known and stable, splitting automates the entire distribution decision — there's no transfer to remember, no balance to evaluate, no discipline required. The money simply arrives where it belongs. Building a dedicated buffer in each account is part of making the splitting system resilient — the concept and mechanics of a financial buffer that absorbs income timing variation without disrupting bill payments is covered in the article on how to build a buffer account.

The Decision Framework: Which Approach Matches Your Situation

The right landing zone is the one that matches your current account structure and produces consistent outcomes for bills, savings, and spending. Here is the decision framework based on your situation.

Choose Checking Landing If:

You don't have a separate bills account yet. Your checking account handles both income and daily expenses and you haven't separated them. You have variable income that requires manual monthly allocation decisions. You're in the early stages of building a multi-account system and are still calibrating allocation amounts. Any of these conditions makes checking the appropriate landing zone — not because it's the best long-term structure but because it's the right match for your current system stage.

Choose Bills Account Landing If:

You have a dedicated bills account that is operational and correctly calibrated. Your bills total is stable and predictable. You have a history of late payments or bill payment anxiety that the current structure hasn't resolved. You operate a "obligations first" financial philosophy and want the structure to enforce it automatically. This approach requires that the bills account exists and is working before the landing zone switches — if the bills account isn't ready, set it up first.

Choose Direct Deposit Splitting If:

You have stable W-2 income, a fully operational bills account, an active savings account, and stable allocation amounts for both. You want to eliminate manual transfers and distribution decisions entirely. You've been operating a multi-account system long enough to know the right amounts for each destination. Splitting is the terminal state of a maturing money system — the stage where automation replaces all active management. The complete account structure that makes splitting work — the three-account framework that separates bills, spending, and savings into distinct functions — is covered in the article on the 3-account money flow system.

How to Transition as Your System Matures

Your landing zone should evolve as your financial system matures. Most people follow a natural progression from simpler to more structured approaches — and that progression is healthy, not a sign that the earlier approach was wrong.

The Natural Progression

Phase 1 — Checking landing, manual transfers. Everything lands in checking. You manually move money to bills and savings after the paycheck arrives. This is the starting point for most people. It works when the discipline is consistent and creates problems when it isn't.

Phase 2 — Checking landing, automated transfers. Everything still lands in checking, but scheduled automatic transfers move money to the bills account and savings account within 24 to 48 hours of each paycheck. The discipline requirement drops because the transfers happen without active management. This is a meaningful upgrade from Phase 1 and works well for many people indefinitely. Setting up automated bill payments from a dedicated bills account — removing the manual execution from every payment — is the automation step that makes Phase 2 reliable and is covered in the article on how to automate your bill payments.

Phase 3 — Bills account landing or direct deposit splitting. The landing zone itself becomes the distribution mechanism. Either your paycheck arrives in the bills account first and spending money transfers out after bills are funded, or your paycheck splits at source and arrives pre-allocated. Both approaches eliminate the transfer discipline requirement entirely because the structure handles distribution without any active management.

How to Know When to Progress

You're ready to move to the next phase when the current phase is working reliably and the remaining friction is structural rather than behavioral. If bills consistently get paid, savings transfers consistently happen, and you're not manually moving money between accounts more than once per pay cycle, the system is working. If bills are occasionally late, savings transfers get skipped, or you're constantly checking balances to see what can be spent, the structure needs adjustment — not the discipline. The full multi-account budgeting system — how to design an account structure that removes financial decisions from daily life — is covered in the article on the multi-account budgeting system.

What Actually Matters Most

Where your paycheck lands is less important than what happens in the 48 hours after it lands. A checking landing zone with reliable automated transfers to bills and savings produces the same outcome as a bills account landing zone with manual transfers — if both execute consistently. The structural question is not "which account receives the deposit?" It's "how do I ensure money reaches the right places automatically, regardless of which account receives the deposit first?"

The answer to that question is a fully functioning account infrastructure — dedicated accounts for distinct purposes, automated transfers or split deposits connecting them, and buffer balances in each account that absorb timing variation without disrupting any of the flows. Building that infrastructure is a process that takes most people three to six months to calibrate. The landing zone decision is one component of that process, not the whole of it. Protecting the emergency fund and cash reserves that make the entire system resilient to income gaps or unexpected expenses is covered in the article on emergency fund and cash reserves.

Design Your Complete Money Flow System

The landing zone is one decision in a complete income routing system. The Paycheck Money Flow Design cluster covers the full architecture — account structure, allocation amounts, automation setup, and how to build a system that runs without constant manual management.

Explore the Full SystemGovernment Resources

CFPB — Bank Accounts — Official guidance on checking accounts, savings accounts, and how direct deposit works across account types.

FDIC — Money Smart Financial Education — Federal financial education resources on account management, budgeting, and building a stable banking system.

FTC — Understanding Your Paycheck — How to read your pay stub, understand direct deposit, and manage paycheck distribution.

Return to the full banking systems and account structure guide for the complete framework for organizing accounts, automating money flow, and building financial infrastructure.

Frequently Asked Questions

Should my paycheck go to checking or a bills account?

It depends on your account structure and financial goals. If you don't have a dedicated bills account yet, checking is the right landing zone. If you have a functioning bills account with a stable bills total, landing in the bills account protects your obligations automatically before any spending is possible. If your employer supports it and your income is stable, direct deposit splitting to multiple accounts eliminates the landing zone decision entirely by routing money to its final destination at source.

Can I change where my paycheck deposits after I've already set it up?

Yes — contact your employer's payroll or HR department and request a new direct deposit authorization form. Changes typically take one to two pay cycles to take effect. You can change this as many times as needed as your system evolves. Keep your previous account active during the transition to ensure no deposits are missed during the processing window.

What if I want to land in a bills account but don't have one yet?

Set up the bills account first and operate it manually for two to three months before switching your direct deposit. During that period, manually transfer the bills amount to the new account each pay cycle and verify that all bills pay successfully from it. Once you've confirmed the account covers everything and the buffer is adequate, switch the direct deposit. Changing your landing zone before the destination account is calibrated creates the opposite of the intended outcome.

Does it matter which account has more activity?

No — activity level is irrelevant to the landing zone decision. What matters is whether the landing zone supports your intended money flow. A bills account can have high activity from automatic bill payments and still be the right landing zone. A checking account can be low-activity and still be the wrong landing zone if it doesn't support the separation you're trying to create. Choose based on which account the money should flow through first, not which account is more or less active.

What about side hustle or freelance income — where should that land?

Route irregular income differently from your primary paycheck. Side hustle income should land in a separate account designated first for tax reserves — typically 25 to 30% set aside for self-employment taxes if you're not withholding — with the remainder distributed to bills and spending after the tax reserve is funded. Mixing variable irregular income with your primary paycheck flow creates complexity that makes the system harder to track. Keep the income streams separate until each one is stable and predictable enough to incorporate into the main allocation system.

How do I know if my current landing zone is working or needs to change?

Your landing zone is working if bills consistently pay on time without active management, savings transfers happen reliably, and you're not moving money between accounts more than once per pay cycle. It needs to change if bills are occasionally late because spending depleted the balance first, savings transfers get skipped, or you regularly feel uncertain about whether bills will clear. The failure mode in every case is structural — the landing zone and distribution system aren't aligned with your priorities — not behavioral. Changing the structure resolves structural problems. Changing behavior resolves behavioral ones.

This article is for educational purposes only and does not constitute financial advice. Your optimal income landing zone depends on your account structure, income consistency, spending patterns, and financial goals. PersonalOne is a free financial education platform and does not offer personalized financial planning services.